Learn more about Tundra’s definition of Frontier Markets, how we differ from the pack, and why we believe the fund can offer an exciting long-term upside and be a good diversification in the global equity portfolio in this report. Read about all our fund in the Full Prospectus on the Buy/Sell page.

We publish a monthly letter commenting on market developments and our funds. Read the latest as well as previous editions here.

Subscribe here if you would like to be added to the distribution list.

RISK INFORMATION

Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return.

The Full Prospectus, KIID etc. can be found at Buy/Sell and the Annual and semi-annual reports can be found at Annual Reports. You can also contact us to receive the documents free of charge. Please contact us if you require any further information:+46 8-55 11 45 70.

Frontier markets

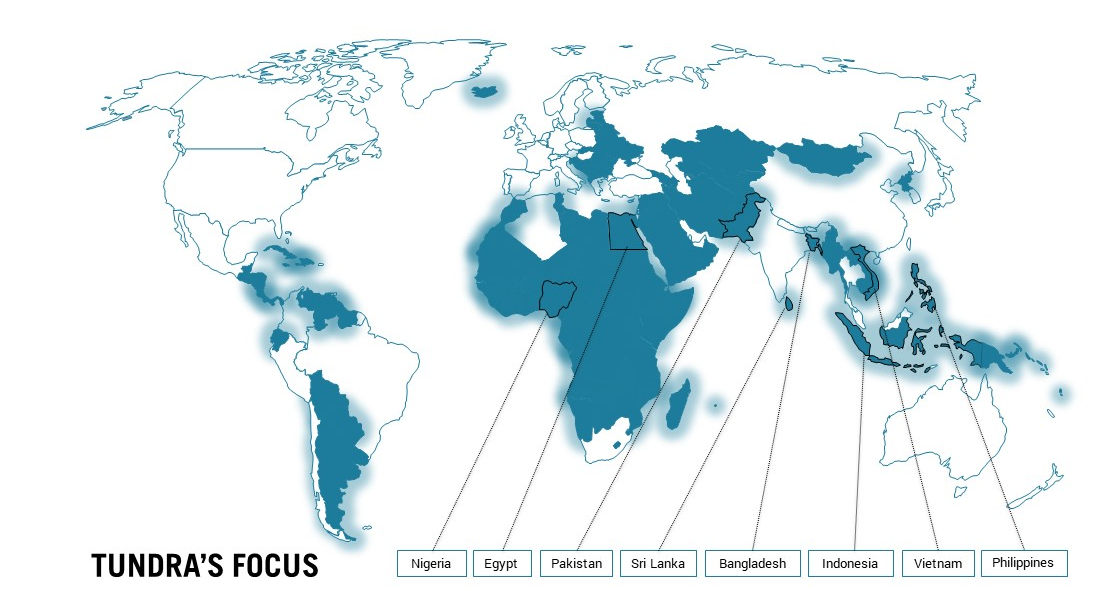

A new generation of growth markets are emerging. Frontier markets are the next generation of emerging markets that include countries such as Vietnam, Bangladesh, Pakistan, Sri Lanka, Nigeria and Egypt. These are countries that come from a low level of economic development but which have undergone a transformation in the last decade and now are among the fastest growing economies in the world. Tundra’s definition of frontier markets are countries defined by the World Bank as low-income or lower-middle-income countries. These countries currently make up 50% of the world’s population, but according to UN estimates, by 2070 they will make up almost 67% of the population. Most of what we read about these countries is about the problems, but the fact is that between 2008-2018, the proportion of people living in extreme poverty in lower-middle-income countries decreased from 27% of the population to 11%. A new generation of workers and consumers are emerging. In the coming decades, a large part of the world’s factories, roads, hospitals, schools and shopping malls will be built in these countries. This suggests that economic activity will be higher than in the rest of the world. Tundra invests in the best companies in these countries that benefit from this development.

Economic growth in frontier markets is driven by:

- Demographics: Frontier markets have young and fast growing populations. Today, frontier markets represent close to 50% of the global population but according to UN:s population estimates, by 2070 their share of the world population will have increased to close to 67%. People in countries such as Pakistan, Egypt and Sri Lanka are also becoming better educated. Education contributes to higher levels of productivity and a more sustainable economic growth.

- Urbanisation: Frontier markets are going through an urbanisation trend – gradually more and more people are moving from rural to urban areas. As this transition takes place, infrastructure investments increase, children and youths get access to modern education, and a growing proportion of consumption takes place through the formal economy in super markets and department stores rather than through local markets. In countries such as Sri Lanka, Pakistan and Bangladesh, approximately 40% of the population is urbanised compared to 80% in Western Europe and the US.

- Infrastructure investments: Infrastructure investments take place continuously in frontier markets. Reliable power supply is ensured, road networks are expanded and a growing section of the population gets access to computers and telecommunication.

- Foreign direct investments: Foreign direct investments in frontier markets have expanded over the past decades. For several years now, Nike produces more shoes in Vietnam than in China and Samsung Electronics, the South Korean electronics giant, produces half of its handsets in Vietnam. We recognise this pattern from history – Japan, South Korea, Taiwan and China have already gone through this phase. Now it is time for countries such as Vietnam, Bangladesh and Pakistan to take their turn.

- Rising political stability: We tend to associate countries in Africa, Asia and other developing parts of the world with political instability. This is only partially true. Never before has e.g. Africa had so many democratic governments as today. In addition, the number of armed conflicts has seen a decline in the past decade.

Frontier Markets

Uncharted territory

Frontier equity markets are still dominated by domestic investors. The number of foreign pension funds, insurance companies and asset managers which are active in frontier markets is limited. To a large extent, these markets are still uncharted territory. The limited number of foreign investors also means that frontier equity markets tend to be less analysed. For long-term investors it creates opportunities to find under-researched and undervalued companies that over time, as the economies grow, will attract more foreign capital.

Limited foreign investor participation also contributes to frontier markets having relatively low correlation with other equity markets and asset classes. Replacing a portion of a global equity portfolio with frontier markets can contribute to reducing the overall risk level of the portfolio while maintaining returns.

Risks

Just as frontier markets offer great return potential over time, the asset class is also associated with risks.

- Market liquidity is still worse than in more developed asset classes

- Despite improvements in terms of political stability, frontier markets are still associated with more political risk than emerging markets and developed markets.

- Frontier market currencies tend to be more volatile than emerging and developed market currencies.

- Poor corporate governance and presence of corruption can be assumed to be more prevalent than in other parts of the world.

Tundra works proactively with these issues as part of our analysis.

Frontier markets have historically struggled with high gearing. This is no longer the case. Write downs combined with high economic growth have resulted in frontier markets today having a lower gearing (measured as external debt as a portion of GDP) than for instance the G7 countries.

Suitable for actively managed funds

Passive investment vehicles such as ETFs and index funds have grown in popularity during the past years. Frontier markets are less suitable for passive vehicles. Transaction costs are typically higher; they tend to lack a functioning futures market; indices rarely fully reflect the structurally most attractive investment opportunities. This is also frequently reflected in the poor relative return of passive vehicles investing in frontier markets and why there are substantial opportunities for outperformance created through active management.

INVESTMENT PHILOSOPHY

Our investment selection is made in accordance with traditional fundamental analysis. Our funds are actively managed.

We have three key criteria that must be met in order for us to invest in a company:

- The company’s owners must be responsible and honest, and the company must have a competent management with a proven track record to navigate different market conditions. Regardless of potential, we as shareholders must first and foremost be sure that the people behind the company run the company for the benefit of all shareholders.

- The products or services the company markets should be in structural growth, i e demand for them should grow faster than the underlying economy. The analysis includes both the product/service itself, as well as how it is produced with regard to impact on the environment and employees.

- The company must have a positive impact on the society in which they operate. This is the core of our sustainability analysis and crucial for financial performance. After risks with corporate governance, the risk of government interference is the highest in our markets. Companies that help society develop have a significantly lower risk of being exposed to government interference.

Tundra Fonder has no restrictions on what proportion of the portfolios may be invested ”off benchmark”. This also means there will be times when we fall behind our competitors. Daring to take the risk of ”being wrong”, not only in individual quarters, but even years, is essential for success in creating good long-term returns, we believe. Tundra Fonder’s products are not for investors seeking short-term stable returns, nor a return in line with an index. Such investors are better off investing in one of the successful hedge funds or in an index fund.