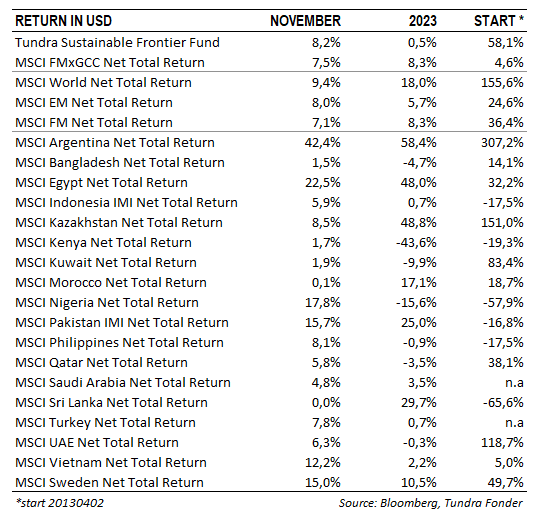

EGYPT AND PAKISTAN LIFTED THE PORTFOLIO DURING NOVEMBER

In USD, the fund rose 8.2% (EUR +5.2%): during November, compared to the MSCI FMxGCC Net TR (USD), which rose 7.5% (EUR: +4.5%), and MSCI EM Net TR (USD), which rose 8.0% (EUR: +5.0%)

The largest absolute contribution during the month (+3.1%) came from Pakistan, where our sub-portfolio rose 17%, primarily driven by a strong performance by the textile company Interloop (+34%) and National Bank of Pakistan (+31%). We note that Interloop has now risen 56% (USD) this year, after being down 34% at the beginning of May. A strong recovery for Pakistan’s star in sustainable textile production which, even at these levels, is valued at a relatively modest P/E of 5x this year’s earnings. The second largest contribution came from Egypt (+2.2%) where our Egyptian sub-portfolio rose 28%, primarily driven by strong performance for the financial and automotive conglomerate GB Corp (+35%) and the education company CIRA (+32%). The largest negative contribution was received from Indonesia (-0.8% portfolio contribution), where our investment in the media company Media Nusantara (-18%) was weak. The company continues to suffer from TV viewers being forced to upgrade their receiver equipment, which has lowered the number of viewers and reduced advertising revenue in the short term. At a valuation of 5x this year’s profit, however, the setbacks are well priced, while the company’s digital assets in the subsidiary MNC Digital are assigned a non-existent value. The only other market that contributed negatively was Sri Lanka (-0.1% portfolio contribution).

During the month, Sri Lanka lowered its policy rate (mid-rate) by a further 100 basis points, to 9.5%. It is still significantly above the country’s inflation, which during November came in at 3.4%. Inflation rose in November from 1.8% on an annual basis, primarily as a result of increases in electricity prices (12-18%). After the strong rise during the first eight months of the year, the stock market has rebounded slightly in the last three months. The first, more drastic, repricing of risk has been completed and investors are now awaiting the finalization of debt restructuring negotiations to ensure that the recovery is sustainable. During the month, Sri Lanka reached an agreement with parts of its creditors (the so-called Paris Club), which is a positive step forward. However, the most difficult negotiations will likely be with the holders of the country’s Eurobonds. Debt restructuring of commercial debts tends to attract some dubious actors who try to take advantage of the situation through almost extortion-like methods. We are also approaching 2024 when the country is supposed to hold presidential elections in the autumn. The market probably prefers current President Wickremasinghe who led the country out of the crisis. However, he is still far behind in opinion polls. It is a long way until the election, which right now looks unusually open.

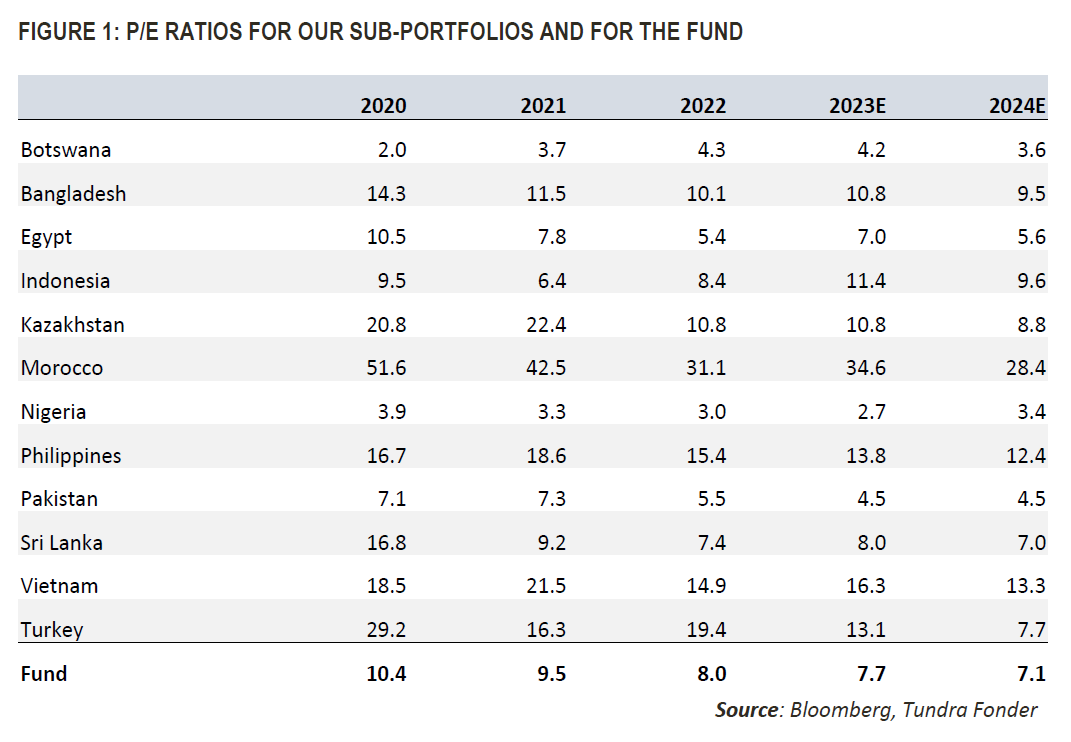

When we look ahead, we note that our thesis of gradually improving news flow from the second half of the year is still intact and looks like it can extend a manageable distance into 2024. It is less about a greatly improved economic climate, and instead more about how several years’ extreme impact (covid, followed by Russia-Ukraine) is gradually being worked through. As we have tried to show in our updates on the profit development in our portfolio companies, the majority of companies have fared decently well but market concerns have meant significant multiple contractions. As the news flow now gradually improves, fear diminishes, and investors “rediscover” markets. Pakistan is a typical example. The stock market has now risen just over 20% in USD this year, from being down 20% as recently as end of June. Those who have followed our monthly newsletters have seen us try to explain that the actual impact on companies’ profits is not in proportion to the price declines. A company’s (and its share’s) value is in the long run decided by its ability to generate profits (positive cash-flows) to its shareholders. Cash generation varies in cycles but is generally decently stable. Equities are real assets. In periods of high inflation, competitive companies also raise their prices. Companies with a high proportion of imported goods or machinery in their production are also forced to raise their prices when their currency is devalued. This means that even more severe crises rarely have more than 1-2 years of impact on companies’ underlying earnings, provided they are competitive. In the short term, however, stock market psychology, or sentiment as we in the industry sometimes call it, plays an important role. Fear and greed cause investors to sell too low and buy too high in all markets. Investors’ expectations of the future tend to fluctuate considerably more than the actual development of the companies they own. Limited knowledge and access to information means that frontier markets are particularly vulnerable to investor mood, and thus speculation. Looking at the portfolio’s valuation, we note that the expected P/E ratio for 2023 is 7.7x. The exact same portfolio was valued at P/E 9.5x in 2021 and 10.4x in 2020, i.e., 23% and 35% higher, respectively. Looking at individual markets, we note that our Pakistani portfolio is valued at P/E 4.5x even after the recent rise. This compares to P/E of 7.3x and 7.1x in 2021 and 2020 earnings, respectively. Provided we do not see any further shocks around the world, it is most likely that the valuation of our holdings will now gradually return to historical valuations. It should be noted that it is not a matter of the outlook miraculously changing for the better, just that the bottomless pessimism is gradually abating, and we are returning to a more neutral climate.

___________________________________

TUNDRA SUSTAINABLE FRONTIER FUND REPLACES THE SWAN WITH THE EU’S REGULATIONS FOR SUSTAINABILITY

In connection with the new EU regulation under the Sustainable Finance Disclosure Regulation (SFDR), new requirements are applied to funds’ sustainability work as of March 2021. Tundra has therefore decided on July 4 not to continue with the Nordic Ecolabelling of the fund. According to the new regulations, sustainability reporting must take place in a uniform manner and funds are divided into different categories. The Tundra Sustainable Frontier Fund is classified as an Article 8 fund (Light green: promotes environmental or social characteristics). The investment philosophy of the fund remains the same; management of the fund and is not affected by the change.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.