THE FUND:

The fund fell 3.2% during November, compared with MSCI FMxGCC Net TR (SEK), rising 1.5% and MSCI EM Net TR (SEK), rising 3.1%. It was a generally weak month for the fund, where we had to yield some of this year’s outperformance. Our stock selection in Vietnam (primarily the absence of the largest Vietnamese index shares) cost about 1% relative yield; the underweight in Argentina cost about 1%; the overweight in Pakistan cost just below 1%; and the overweight in Nigeria about 0.5%. This month we were lacking significant positive contributions. The fund is now down 2.8%, since the start of the year, compared with the fund’s benchmark index, which is down 12.4%.

During the month, we have implemented some major changes to the portfolio for the new year. The biggest change is that Argentina is back in the portfolio (6% of fund assets). We exited Argentina at the end of 2017 and the beginning of 2018 because we felt the valuations were unreasonable and did not account for significant macroeconomic risks. This has been the single biggest reason for the fund’s outperformance in 2018. We now see that the Argentinian peso has fallen enough (-50% in 2018) and the country has taken the necessary steps to restore confidence. We also see that the concerns arising from the adjustments (likely negative growth in the first half of 2019 and possible effects on incumbent President Macri’s chances of winning the presidential election in the fall of 2019) are widely known and should be discounted. Macri will find it difficult to be re-elected, but the only significant political risk for Argentina, a return of Christina Kirchner, seems very unlikely in our eyes.

At the stock level, we have been positively surprised by how a number of companies have handled the crisis both in terms of actual results and in the transparency they have shown. Argentina faces a very tough first half of 2019 and it will be significantly worse before it gets better. However, we believe that 2019 will be a year of recovery for frontier and emerging markets, looking beyond the short-term effects of the crises that characterised 2018. We note that Argentina from current levels has a reasonable risk-reward. We have bought back 3 of our previous investments in the banking sector, now 50-70% lower than when we exited. The purchases in Argentina were primarily funded through sales in Egypt, where we sold the bulk of our positions in the cement sector. We also reduced our positions in the banking sector and continue to shave off from one of our bets in consumer discretionary. That said, we added a position in Egypt during the month, a private education provider CIRA. Educating Egypt’s youth is a priority area for the state, and CIRA will play an important role in achieving the global goal of education for all children. We met the company just over a month ago in Cairo and believe it has good prospects for showing significantly higher growth than the economy as a whole over the next ten years.

We also made some changes in Bangladesh after our most recent trip. We were impressed by the positive conditions for the pharmaceutical sector where we increased during the month. We have not wanted to increase our overall exposure to Bangladesh given that we see a certain risk for the currency in the short term, probably after the election at the end of December. We, therefore, chose to reduce our positions in BRAC Bank and IFAD Autos and increased our exposure to the pharmaceutical sector.

We have also made some changes in Pakistan. We have completely exited our position in Meezan Bank, which has been one of the fund’s most successful holdings since our first investment 4 years ago. Meezan Bank’s focus on islamic financing combined with a high added value to high net worth individuals has been, and will continue to be a recipe for success. However, the valuation is now closer to twice as high as the larger traditional banks, and we do not think the differences in future growth from current levels are large enough to justify the valuation. We have instead bought the third largest bank, United Bank. Higher interest rates will mean higher net interest rate margins for the banking sector in general and with a currency that is now cheap, we believe that nominal growth over the next few years will translate into corresponding growth in foreign currency earnings. According to our estimate, United Bank is trading around 7x next year’s profit. Combined with a yield of 9% and a low downside on the currency, it appears attractive.

THE MARKET:

MSCI FMxGCC Net TR (SEK) increased 1.5% during the month, compared with MSCI EM Net TR (SEK), which rose 3.1%. Among the larger markets, Argentina and Morocco returned 4.5% and 2.9% respectively in SEK. Many were surprised that Sri Lanka, in the midst of what constitutes a constitutional crisis, was one of the winners during the month and rose almost 3%. President Sirisena sacked Prime Minister Wickremesinghe in late October and appointed former President Rajapaksa as the new prime minister. Given the complicated history between Sirisena and Rajapaksa, where the former unexpectedly changed sides in conjunction with the presidential elections in 2015 and supported the opposition to defeat Rajapaksa, this nomination was very unexpected. However, the opposition has argued that the changes are unconstitutional. Two votes of no confidence against Rajapaksa have passed without any action by President Sirisena. Instead Sirisena announced the dissolution of Parliament and new elections in January, more than a year before planned elections. The Supreme Court is currently investigating whether Sirisena is entitled to take these actions. At this point it seems doubtful they will allow it. The situation is further complicated by both sides claiming they represent the people’s will. Earlier this year, local regional elections were held in Sri Lanka, where Rajapaksa progressed very strongly. It is likely that if elections were to be held today, team Sirisena/Rajapaksa would win. However, the accelerated pace at which they have tried to achieve this win has probably reduced support for them. Regarding the market’s reaction, we conclude that local investors have been aggressive buyers since the process began in late October. From a purely cynical market perspective, investors find that Rajapaksa, despite all allegations of corruption and human rights violations during the Civil War, is better suited to leading the country. The current political crisis is, of course, negative for the country’s economy in the short term. Over the last five years, Sri Lanka has faced some criticism in terms of its economic policy, which means that the Sri Lankan stock market is now one of the cheapest frontier markets, from being one of the most expensive in the past. Despite the risk of continuing turbulence in the short term, we conclude that much of it has been discounted by the market. An early election would be clearly positive for the stock market. Among more generally influential factors, the US and China, took one small step away from a wider trade war, something that is likely to have a positive impact on emerging and frontier markets. As an investor focused on fundamentals, we are opposed to embarking on far-reaching theories about what will once again get the “herd” of global investors back into emerging and frontier markets. We prefer to focus on how the companies we own are expected to develop. However, it seems clear that an important element will be the signals from the US central bank (FED). Any signs that the rate increases in this cycle are coming to an end is likely to have a tangible impact on emerging and frontier markets given the FED’s central role in the discussion in the bear market that started in April this year. Four interest rate hikes, of which the last one is expected in the fourth quarter of 2019 is currently expected.

There is a reason why stock markets do not deliver their average return of 8-10% each year. Fear and greed create volatility investors have gotten used to. As someone humorously expressed it: “The equity market is the only market where investors run towards the exit when prices are lowered.” And right now it is ”sale” in most markets. Not only are the valuations low — the portfolio’s P/E for 2018 is currently 8.2x — and we currently expect the valuation to fall to just below 7x for 2019. Many currencies in frontier markets now also appear cheap after sharp depreciations in the past year.

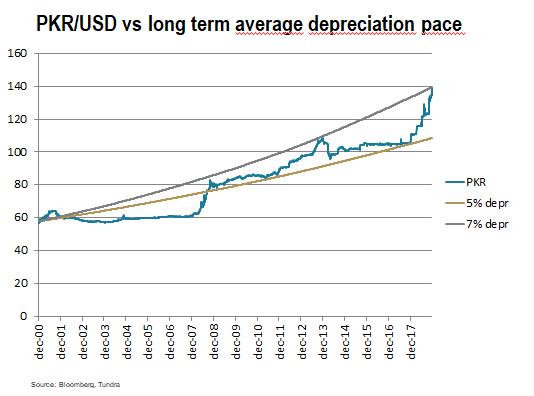

We do not think investors should be overly concerned about currency developments, except in extreme cases where the currencies overshoot too much and stock prices do not take this into account. Argentina at the end of 2017 was one such case. Currencies in our markets tend to drop 3%-5% annually against the US dollar, which can be explained by higher interest rates, which can be explained by higher inflation. Rarely do these adjustments take place evenly over time though but in sharp sudden moves after a couple of years of too strong exchange rates. By nature, it is difficult to predict over-valuations, as they tend to arise in conjunction with positive macroeconomic developments, increasing direct investment, etc. When the trend breaks, it is usually due to shocks in the economy or in the political climate and the currency tends to overshoot, i.e. it weakens more than the fundamental need. The adjustment is then usually followed by a longer period of relatively modest weakening, lower than the long-term trend. Pakistan may be said to be a good example in recent times. As shown by the graph (top right), the average currency weakening since December 2000 (starting point chosen to get some space from the 1997/98 currency crisis) is now 7%, which has historically been followed by several years with significantly more modest currency movements. 2018 has been a challenging year for investors in emerging markets and frontier markets and there is plenty of concern left. For us, however, it is always about the expected average return, which is likely from current levels. After a number of tough years in which currency crises were racked (Kazakhstan, Nigeria, Egypt, Argentina, Pakistan and Sri Lanka), there are good prospects for a period of return over the historical average of 8%-10% in USD on our markets.

ESG ENGAGEMENT:

Three companies were added to the fund this month. Argentinian financial companies, Grupo Financiero Galicia S.A. and Grupo Supervielle, and an Egyptian educational group called Cairo for Investment & Real Estate Development (CIRA).

Grupo Financiero Galicia is a financial service holding company based in Buenos Aires, Argentina. Founded in 1905, the company operates through banking, insurance and related segments. The bank calculates its carbon footprint while its environmental management strategy involves the reasonable consumption of electricity and paper along with awareness campaigns. The bank is also part of a regional platform that collaborates on knowledge exchange including experiences and best practices called the Sustainable Finance Committee of the Argentine Banking Association. Reportedly, the bank aligns its sustainability report with international standards such as the Global Reporting Initiative (GRI); the company also takes the 17 Sustainable Development Goals (SDGs) into consideration.

Grupo Supervielle is also a financial services holding company that provides banking products and services in Argentina. Based in Buenos Aires, the company was founded in 1887. Financial inclusion is an important aspect of sustainability for the bank, where it encourages and develops financial products and services for less developed communities. The company aims to be an agent of change and a creator of social value through its initiatives. Its strategy includes programs aimed at the promotion of social participation, fighting against child poverty and malnutrition, education, and strengthening institutions. The company prepares its annual sustainability reports according to the GRI.

CIRA is one of the largest private integrated educational groups in Egypt, which targets the higher education and K-12 segments. The company owns and operates 19 schools with 24,000 enrolled students under the Futures Schools and Rising Star brand. In addition, the company runs Badr University in Cairo (BUC). According to the company, each school is accredited either by local or international education boards. The company’s reported employment ratio of teachers is 70% female and 30% male. A yearly plan for developing employee skills depending on their specialisation and/or needs is also created. The company has been a participant of the UN Global Compact since 2003.

Two companies – Egyptian Arabian Cement and Pakistani Meezan Bank – were divested from the fund due to financial considerations.

DISCLAIMER:

Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.

Kundgrupp / Investortype:

* Ontario and Quebec