STOCK SELECTION IN VIETNAM SUPPORTED DURING A WEAK MONTH

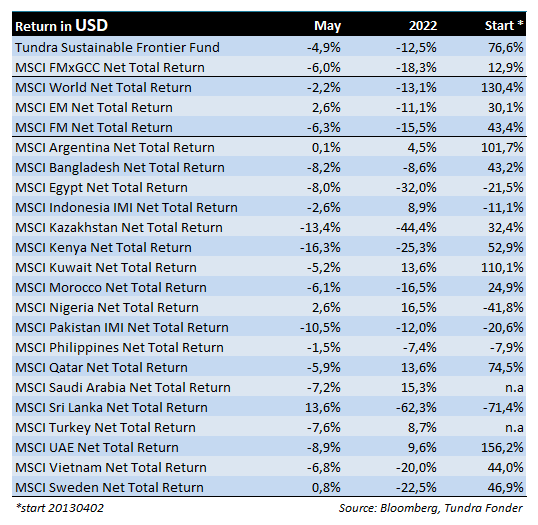

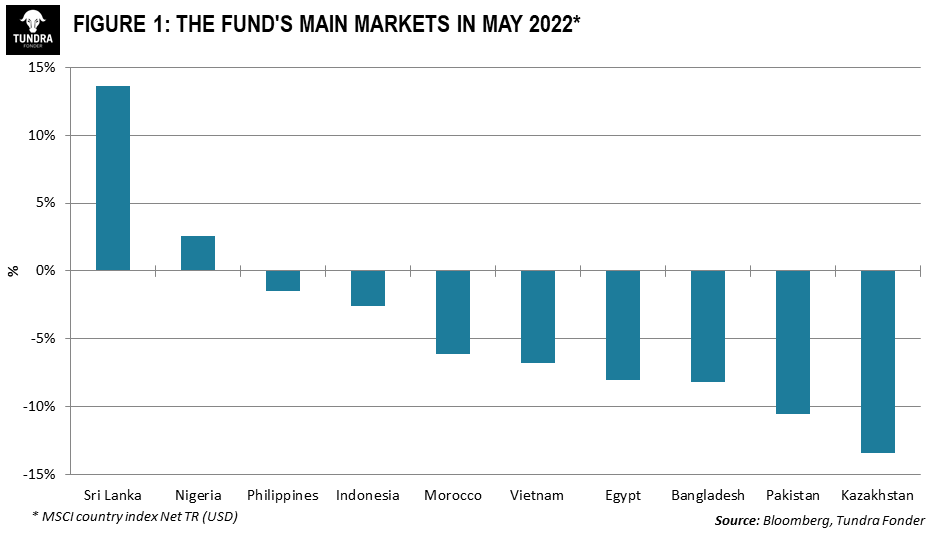

In USD the fund fell 4.9% during the month (EUR: -6.7%), compared to MSCI FMxGCC Net TR (USD) which fell 6.0% (EUR: -7.8%), while MSCI EM Net TR (USD) rose 2.6% (EUR: +0.6%). It was a shaky month. Measured in USD and absolute terms at country-level, a positive contribution was received only from Vietnam (+1.2% portfolio impact), where our sub-portfolio rose 5%. However, this was exclusively due to stock selection, as the market fell 7% during the month. The largest negative contributions came from Pakistan (-3% portfolio contribution), where our sub-portfolio fell 14%, from Egypt (-1.1% portfolio contribution), where the sub-portfolio fell 15%, and from Bangladesh (- 0.8% portfolio contribution), where the sub-portfolio fell 8%.

Despite unfavorable conditions, our stock selection cushioned somewhat, especially in Vietnam. REE Corp (an ambitious renewable energy producer), the fund’s fifth-largest position, rose 30% in a falling market. Rising electricity prices in the competitive generation market (the part of the electricity market where pricing is set by demand and supply) benefit the company. Furthermore, the company’s engineering business (primarily involved in the installation of HVAC, Fire Protection, Electrical, Plumbing & Drainage, etc., at infrastructure, commercial and industrial projects) is set to benefit from the fact that Vietnam has now opened up entirely post-covid.

The fund’s largest position, the Vietnamese IT company FPT Corp, also rose 3% despite the weak local market. Like some Vietnamese companies, the company releases preliminary earnings monthly. In the first four months, profits increased by 35% on an annual basis, which was received positively.

Most of our markets ended in the red during the month. We remain in a climate where further interest rate hikes are expected to curb inflation and mitigate weaker currencies. During the month, five of our countries raised their key interest rates: Pakistan (+1.5pp to 13.75%), Egypt (+2pp to 11.75%), the Philippines (0.25pp to 2.25%), Nigeria (+1.5pp to 13%) and Bangladesh (0.25pp to 5% – repo-rate).

Sri Lanka rebounded by 14% after the country appointed a new coalition government led by former Prime Minister Ranil Wickremasinghe. It was seen as a step toward reducing the unrest in the country. Thus a step toward a successful debt restructuring and a new agreement with the IMF. The rise should be seen in the light of the stock market is still down 62% in USD during 2022.

Nigeria rose 3% during May. Rising commodity prices have trumped the problems of rising inflation. The stock market, which in principle is completely abandoned by foreign investors after a long period of currency restrictions, has so far this year risen 17%.

The Egyptian stock market had a hard time, and Russia’s invasion of Ukraine continues to negatively affect the country’s access to wheat. Egypt is one of the world’s largest importers and Ukraine has historically been an important source of imports. Now, the country is looking for alternative suppliers, including India (which has indicated that it can make exceptions to their export ban). The central bank’s sharp rate hike signals that the country continues to suffer in the current climate.

Pakistan fell 11% due to continued political, and thus economic, uncertainty. The new coalition government, led by PML-N’s Shehbaz Sharif, since its takeover on April 11th appeared indecisive. There have been two camps in the market. One camp has expected that the new government plans to rule until the general elections in 2023 and would take relatively immediately hard economic measures that pave the way for continued economic support from the IMF. The second camp has been expecting that the new government would announce early elections relatively immediately, and the technocratic transitional government would then be able to take the hard economic decisions at no political cost. Former Prime Minister Imran Khan’s sharp rise in popularity after he was ousted has likely made it difficult to decide between these two paths. An early election could mean that Imran Khan’s PTI gains a majority.

At the same time, hard economic decisions, in particular, the abolition of the fuel subsidies that Khan introduced at the end of his term, are politically sensitive and likely to increase support for Khan and PTI even further. In addition, the situation is further complicated by the rather sensitive arrangement of the current coalition, which consists of a right-wing party (PML-N), a left-wing party (PPP), and various defectors – whose reason for changing sides was probably partly the difficult economic situation and how this affected the population. On May 27th, however, the government decided, somewhat unexpectedly, to raise the price of fuel sharply, and on June 2nd, another increase was announced. We welcome the decision, as it lowers the near-term risks of a Sri Lankan-style disaster. The decision indicates that the government will attempt to complete its term. The market’s muted reaction comes against the background of the risks of continued protests from the opposition and probably also some uncertainty as to whether it is possible to pursue a responsible economic policy and at the same time hold together a rather fragile coalition with various ideological backgrounds.

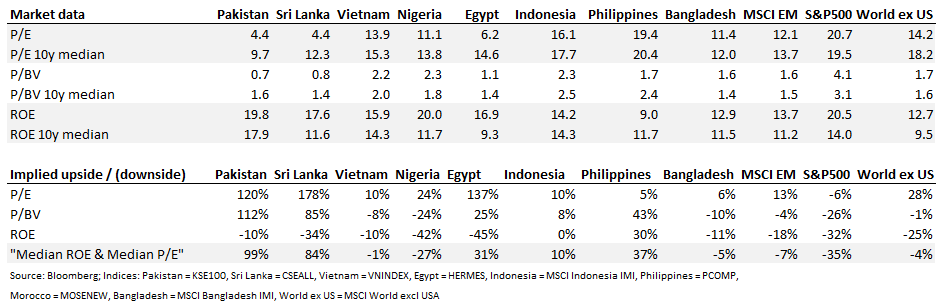

Global stock markets are in a fragile state where we should see falling profit estimates in most markets against the backdrop of rising borrowing costs and higher input costs. The risks to the world economy and individual countries are obvious. How this will be reflected in equity markets from here is less obvious. Equity markets performance will be about exactly how pessimistic investors in each market are, i.e. to what extent they have already acted (sold) per a negative scenario. We have regularly shown a table of current valuations vs. historical valuations in our key markets and comparisons with the US and the rest of the world. It can be a good exercise to refresh current valuations vs historic, as a gauge of sentiment across equity markets.

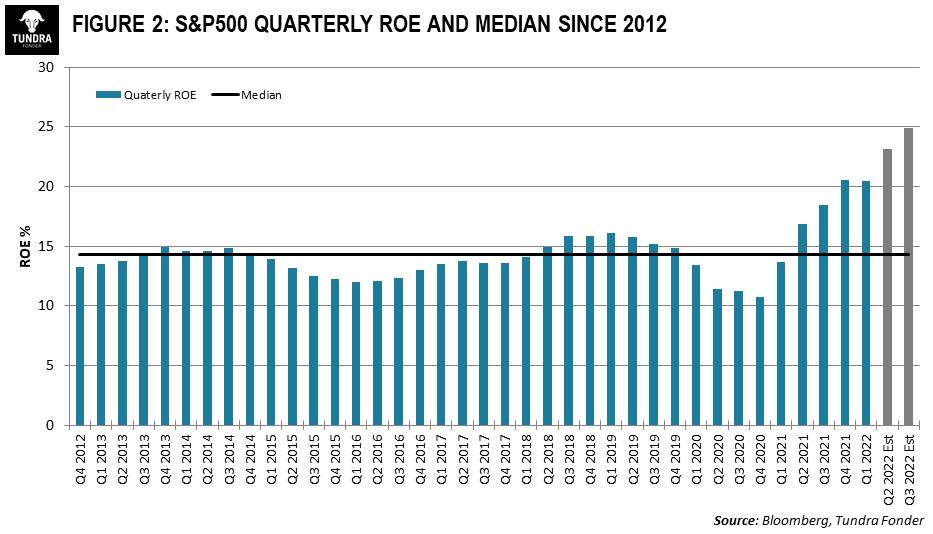

If we start with the world’s largest equity market, the USA, we conclude that the P/E ratio is now not far from the median value of the last ten years. If we move a bit further down the column, however, we note that Return on Equity (ROE) is significantly higher than the median value. The current P/E-ratio is thus low because profitability is unusually high from a historical perspective. In the current global context, it is optimistic not to expect profitability to come down, especially given the fact that the return on equity historically has proven to be quite cyclical (see Figure 2 on the next page).

At the bottom of the table in Table 1, we show a scenario that assumes that profitability (ROE) and the valuation (P/E ratio) return to the 10-year median, i.e. normal profitability and normal valuations. In such a scenario, the US stock market would need to come down another 35%, everything else being equal. Looking at the world index excluding the USA, the picture is different. The current ROE is significantly higher than historical levels, but the low valuations vs. historical levels indicate that investors have partly already taken into account a fall in profits. The same applies to larger emerging markets (MSCI EM).

When we apply the corresponding analysis to our major stock markets, we conclude that our markets, except for Nigeria (-27%), Bangladesh (-5%), and Vietnam (-1%), generally indicate quite a significant upside. The largest upside in a scenario where profitability and valuation are normalized is from Pakistan (+99%), Sri Lanka (+84%), the Philippines (+37%), and Egypt (+31%). These four countries are those of our countries that were immediately hardest hit by rising commodity prices in the wake of the Russia / Ukraine crisis. Also, those countries have already priced in a significantly worse scenario than anything that has hit these markets over the last ten years. This leads us to our main argument as to why we remain quite optimistic. Conditions are bad, but investors have already priced in severe pain. This means that in the next few years these markets should be able to provide acceptable returns even in a very negative outcome. At the same time, there is a powerful recovery potential in the unlikely scenario that the world situation suddenly returns to normal.

This kind of exercise of course has limited predictive capability in terms of short-term market performance. It is however useful support when assessing the likelihood of an investment’s long-term return. We maintain our view that our part of the world is one of the few investment categories where it is rational to expect a normal market return (8-10% per year) in the coming years. Since the fund’s inception, we have delivered an average annual alpha of just over 5% per year after full fees and all costs in the fund. Provided we can maintain our alpha generation we should thus be able to generate 13-15% returns during a normal year. Our strong alpha generation is derived from stock selection with a strong focus on quality and low risk in company selection. The following key criteria must be met:

1) Honest owners and a strong management

2) Production of goods or services that are in structural growth (will constitute a larger part of the economy in the future than today) and

3) Companies who have a positive impact on the society in which they operate.

The last factor is the basis of our sustainability analysis, and it is far from as altruistic as it may sound. Companies that manufacture necessary goods and services with the least possible negative impact on the environment and people, who are growing and respected employers, and who are good taxpayers, run a significantly lower risk of being subject to negative government measures (change in taxations, import tariffs for crucial input goods, etc). After risks associated with corporate governance, state governance risks to companies’ operations are the greatest that is associated with investments in our markets. If you invest in businesses subject to structural growth and are diligent about corporate governance risks as well as state governance risks, you have a fair chance to reap the benefits of the higher forecasted growth across our markets over the coming decades.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.