THE FUND

The Fund fell 3.2% during the month, compared to our primary benchmark index MSCI FMxGCC Net TR (SEK), which rose 2.0% and MSCI EM Net TR (SEK), which fell 6.7%. About 3% of the underperformance accrued from the lack of Argentinian holdings. Argentina (21% of the benchmark index in May) rose by 15% during its last month in the frontier index. We lost another 1% from our positions in Pakistan (17% of the Fund), where the sub-portfolio fell slightly more than 5%. We also lost about 0.5% each from our positions in Nigeria and Egypt. Positive contributions were obtained from the absence of holdings in Kenya (0.3%) and positive performance in our Turkish position Medical Park (0.2%). No companies were added during the period and one Kazakhstani company, JSC Halyk Bank, was divested due to financial considerations.

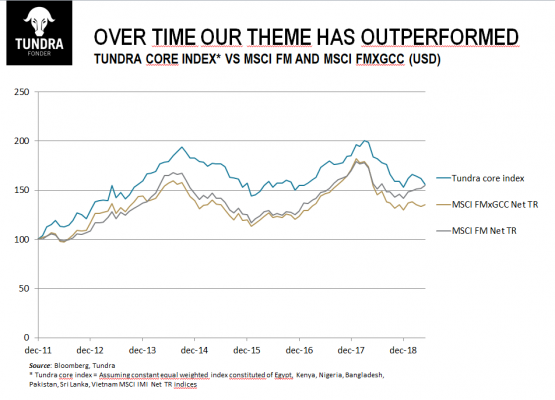

2019 has so far been a tough year for the Fund and the month of May was particularly weak. We note that until the end of May, we had temporarily given back large parts of the excess return we generated in 2018. Our off-benchmark positioning, which helped us during the crash in Argentina in 2018, has so far in 2019 not worked for us. Three out of our seven core markets (Pakistan, Sri Lanka and Nigeria) are at minus returns in USD for the year so far. The perceived risky tail of emerging and frontier markets has so far not been favored in an otherwise strong year, and the risk appetite for mid and small caps has been particularly weak. However, our clear focus on seven core markets (Vietnam, Bangladesh, Pakistan, Sri Lanka, Nigeria, Kenya, and Egypt) has over time outperformed both the broad frontier index and the frontier index excluding the Middle East (see graph). Also, the frontier small-cap index has outperformed the large-cap equivalent historically.

To dare to go against the herd and to focus on the fundamental conditions for our companies is what has generated our excess return since the start, but it also means that during periods we will have to patiently wait for a more rational behavior in the market. The weighted average valuation in the portfolio is currently below 7 times 2019 earnings, the lowest since inception. Three of our seven core markets (Pakistan, Sri Lanka, and Nigeria) are trading near ten-year lows measured as a valuation of book values and at the moment, only Vietnam’s is above its ten-year average P/BV. For the portfolio as a whole, we see the risks of downward versus upward adjustment of profit estimates as well-balanced and we currently have the most well-diversified portfolio based on land risk since the Fund’s inception. Weak periods always mean that we scrutinize the portfolio and our assumptions that form the basis for our investment decisions. Each holding at all times competes with other potential investments. Overall, however, we are very pleased with the portfolio and expect a return significantly above our average return since inception in the coming years.

MARKET

MSCI FMxGCC Net TR (SEK) rose 2.0% during the month, compared to MSCI EM Net TR (SEK), which fell 6.7%. Among the index countries, Argentina excelled with an increase of 14% during its last month as a frontier market (moved to MSCI EM May 31). Among other markets, Romania rose slightly more than 4% and Bangladesh rose just under 1%. The weakest market was Sri Lanka with a decline of just over 6%. Outside the benchmark, but among our core markets, we note that Pakistan fell just over 5% and that Egypt fell close to 6%.

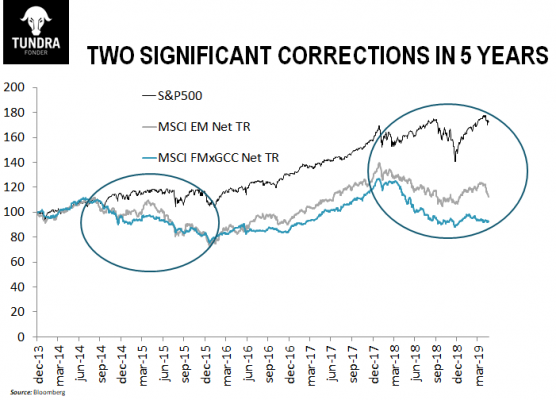

Frontier markets as an asset class have developed strongly in 2019, but so far, it has been a relatively narrow increase, focusing on what investors perceive as less risky markets and with clear preferences for the larger more liquid companies. We interpret it as the caution towards global concerns that characterized 2018 and that continued into 2019, albeit for other reasons. If we dissect the start of the turbulence in 2018, this began with rising US long-term interest rates and expectations of a number of interest rate increases from the US central bank. This has now been transformed into concerns for a global recession. US long-term interest rates are now lower than they were at the beginning of 2018, and the discussion about the policy rate in the US is now centered at when the next rate cut will occur. The infected trade war between the US and China remains a concern and action taken against Chinese telecommunications company Huawei indicates that the conflict may be further aggravated. For example, China has recently flagged to prepare “a package” with similar action against “companies at risk of damaging their national interests”. This list may include a number of global listed companies of importance to the world market index. Although the conflict with China so far focuses on China, Trump’s unpredictability is an ever-present threat to global stock markets, like Turkey, Mexico, and even India recently experienced. We also see some concerns about the situation in the Middle East where it is still tense between Saudi Arabia and Iran. If these concerns start having more severe impacts on global equity markets, emerging and frontier markets have historically been hit even harder. The question that investors have to ask themselves this time, however, is whether this time there is the same room on the downside for emerging and frontier markets in the event of a major decline in developed equity markets. Emerging and frontier markets over the past 5 years have gone through not only one, but two declines. The first 2014-16, due to the falling oil prices, and the other that began in 2018 with weak exchange rate developments and crashes in several markets (see graph 2). One should also note that there are huge discrepancies in performance among the largest index constituents within the broader frontier index. This can be exemplified by the fact that since the end of 2017, the largest index market Kuwait has risen more than 60%, whereas the second largest index market, Argentina, during the same period has fallen by just over 40%. Is it really relevant to talk about the asset class as a unison market at this stage, or have some of the equity markets in the category of early emerging markets and frontier markets already discounted parts of the concerns that global investors today have for the future? The last two years have been about finding pockets among a very heterogeneous asset class, and much indicates that the differences in performance in the coming years will again be substantial. It is far from certain that the “safest” markets in recent years will prove to be the safest in the years to come.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.