THE FUND

The Fund fell 3.8% in July, compared to -5.9% for MSCI FMxGCC Net TR (SEK) and +2.4% for MSCI EM Net TR (SEK). The Swedish krona strengthened close to 7% against the US dollar during the month, which negatively affected the absolute return correspondingly. Our overweight and favorable stock selection in Pakistan contributed to the majority of the excess return during the month. Local investors continue to transfer capital from the bond market to the equity market and the broader interest, which now also includes medium-sized and small companies, traditionally benefits our stock-picking-focused investment style. Lack of holdings in Kenya and underweight in Vietnam were the other two largest contributions in July. Negative contributions were received from Sri Lanka, which fell back after a period of strong performance. We also received minor negative contributions from our positions in Indonesia and Morocco. Among individual holdings, our positions in Pakistan and Bangladesh stood out during the month. Pakistan’s leading industrial conglomerate, Lucky Cement, rose nearly 30% in local currency and the leading Islamic bank Meezan Bank rose more than 20%. The Bangladeshi pharmaceutical company Beximco Pharmaceuticals rose just below 20% in an otherwise stagnant market. Among the losers in July was the Vietnamese steel producer Hoa Sen Group, which fell by about 15% in local currency, partly as a result of concerns in regards to a second wave of COVID-19 in Vietnam, and partly as a reaction to a previously strong price development over several months. Our Turkish healthcare company MLP Care also fell back by about 15% in profit-taking after a strong run-up lately. During August, it will be especially interesting to follow the reports for the second quarter. Five of our portfolio companies have reported so far, of which four are Vietnamese. For the reporting group as a whole, sales increased 33% while earnings per share rose 14%. The second quarter, however, struck very differently between companies and sectors. For example, both our Vietnamese steel companies increased profits by more than 50% as margins for the sector rose after the very tough 2019. We also note that the Vietnamese IT company FPT, in line with the sector globally, showed both sales and profit growth even though the increase was marginal. For our Sri Lankan food company Cargills, sales decreased 12% compared to the second quarter of 2019 while net profit fell by 77%. It should be remembered that Sri Lanka was in principle closed during the period and the coming quarters will look better. Before COVID-19, Cargills was in a positive trend with improved demand and rising margins, which was visible in the first-quarter figures. For the first half of 2020, sales increased by 8% and earnings per share by 20%. In August, most of our remaining portfolio companies should report figures for the second quarter and we will then have a better picture of the impact between our various markets.

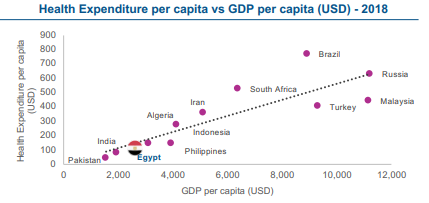

During the month, we sold a smaller remaining position in Pakistani Shifa Hospitals. We also reduced our position in the Turkish health care company MLP Care. Outside adding to some of our existing holdings the proceeds were used to add a new Egyptian company, Ibnsina Pharmaceuticals, which is the country’s fastest-growing pharmaceutical distributor. They are today the second-largest pharmaceutical distributor with just over 20% market share and have increased their market share every year for the past 5 years. During this period, the underlying market has grown by 17%, while Ibnsina Pharma has grown by 31% per year. The health care sector remains our single largest overweight in the Fund given the current very low consumption of medicines and health care, while there is a very strong link between this consumption and a country’s welfare development. It is also a sector where it is possible to build a particularly strong brand, given that the demand for this type of product is very strongly linked to trust. It creates a natural threshold that makes it harder for new competition to emerge. We believe that Ibsina Pharma has crossed this threshold and has a continued interesting growth journey ahead of them.

MARKET

MSCI FMxGCC Net TR (SEK) fell 5.9% in July, compared to MSCI FM Net TR (SEK) which fell 7% and MSCI EM Net TR (SEK) which rose 2.4%. As we wrote under the section for the Fund, the Swedish krona strengthened close to 7% against the US dollar, which means that the market performance in local currency was neutral during the month. Of the markets included in the index, none managed to fully compensate for the weaker dollar. Morocco did best with a decline of 2% in SEK. Sri Lanka (-14%) and Vietnam (-10%) were the underperformers. Both countries have previously been praised for the limited spread of COVID-19 but were negatively affected in July when an increase in registered cases was noted. It is a reminder to be careful about proclaiming “winners” at this stage of the pandemic and to define what “winner” means. As a parenthesis, it can be said that Pakistan and Vietnam had very different trajectories in the pandemic. As of the 2nd of August, Pakistan had 280,000 registered cases and 6,000 deaths, compared to Vietnam which at the same time had 620 cases and 6 deaths. Pakistan has applied more selective shutdowns and has not been able to carry out the systematic infection tracing maintained by Vietnam. Initially, Vietnamese shares performed better, but since the end of March, the Pakistani equity market has performed significantly better and as of the end of July, the two stock markets had an equivalent performance for the full year so far. The lesson is that those countries that are highlighted early on to have effectively controlled the spread of infection are probably more sensitive to signals of increased spread of infection. During August, most companies in our markets will report results for the second quarter. We then get a good yardstick for how hard the companies were hit when it looked the worst in our countries. Most Vietnamese companies have already released their reports. For these, we note that sales have fallen marginally on an annual basis while profits are almost unchanged compared with the second quarter of 2019. However, the country was a bit unique with a fairly short shutdown, followed by a rapid recovery. Our other countries will have been hit harder. Given that equity markets are forward-looking, what the companies say about their outlooks are likely to be more interesting to read. Has COVID-19 created a permanently lower demand level, from where to grow from or do they expect a more significant recovery? The sharply lower interest rates, primarily in Pakistan and Sri Lanka, may have a positive effect on the companies’ prospects in these countries. In Sri Lanka, the results of the parliamentary elections have just been announced. The very strong majority won by the Rajapaksa Brothers’ party SLPP will be interpreted positively by the equity market. We have said it before, but it is worth repeating: the big event of the autumn will be the US presidential election. We believe that an election victory for Joe Biden would be positive for emerging and frontier markets as it probably means less anti-globalization rhetoric. Given the large valuation gap between the US and emerging and frontier markets, this may mean we will see some reallocations to the later markets.

ESG Engagement

One Egyptian company was added to the fund in July.

Ibnsina Pharma (ISP), established in 2001, is an Egyptian-based pharmaceutical distribution company. The company distributes a competitive portfolio of pharmaceutical products from over 350 Egyptian and multinational companies to more than 42,000 customers including pharmacies, hospitals, retail outlets, and wholesalers. Its fleet of around 760 vehicles completes an average of over 460,000 deliveries each month. ISP is compliant with quality, environmental, road safety, and health & safety certifications including ISO 9001:2015, ISO 14001:2015, ISO 39001, and OHSAS 18001:2007. As part of the company’s CSR efforts and to support state efforts in the face of the COVID-19 crisis, ISP has donated EGP 4 million to the Egyptian Authority for Unified Procurement and EGP 5 Million to Welfare Fund.

One Pakistani company, Shifa Hospital, was divested from the fund due to financial considerations.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.