NIGERIA WEIGHS DOWN A POSITIVE MONTH

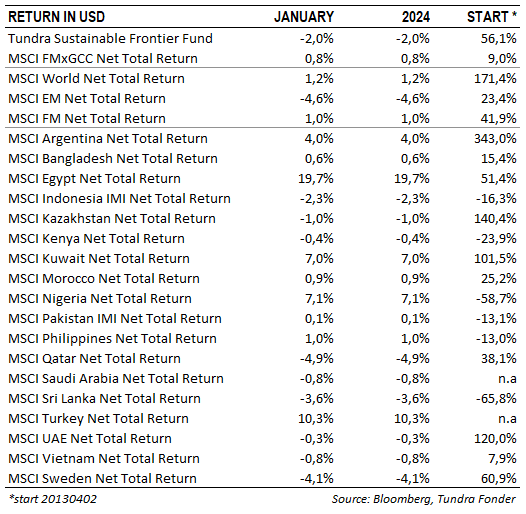

In USD, the fund fell 2% (EUR: -0.3%), compared to the MSCI FMxGCC Net TR Index (USD), which rose 0.8% (EUR: +2.5%). We lost around 2% in the short term in Nigeria, where the Naira was devalued by 40% (read more below). In addition to Nigeria, we lost 90 basis points (bps) in Indonesia, where primarily our healthcare company, Hermina Hospitals, had a weak month. Further we lost 90 bps in Pakistan, where one of our largest holdings, Systems Ltd, lost 6% during the month. Positive contributions were received from Vietnam (60 bps), whereas Turkey, Bangladesh, Philippines, and Egypt combined added approximately 1% in absolute return.

Bangladesh held its election on 8th January. As expected, the election was won by the incumbent Awami League, led by Prime Minister Sheikh Hasina. The election was preceded by extensive protests against the incumbent government party, and the main opposition party, Bangladesh Nationalist Party, chose to boycott the election. From a market perspective, we now have five years until the next election, which increases the possibilities for somewhat tougher decisions. An important one came on 18th January. After 18 months, the stock exchange removed the so-called “floor pricing rule” for most of the listed shares. During this period there were restrictions on the lowest price that individual shares could be traded at on the stock exchange (although buyers and sellers could agree outside the stock exchange). Both of our relevant positions (Square Pharma and Brac Bank) rose in good volume after the decision by 8% and 9%, respectively.

Pakistan is preparing for what will be a truncated election on 8th February. During the month, former Prime Minister Imran Khan was sentenced to ten years in prison for allegedly leaking classified information. Continued severe restrictions on Imran Khan’s party, PTI, suggest that the election will be won by the former ruling coalition, led by the PML-N, which appears to enjoy continued support from the actual governing power – the military.

From a crass market perspective, this would mean a, for the time being, stable political situation, which gives the many talented entrepreneurs in the country the opportunity to focus on their businesses. The current, and likely future, government set-up reflects decently well what Pakistan has looked like for the last 10 years.

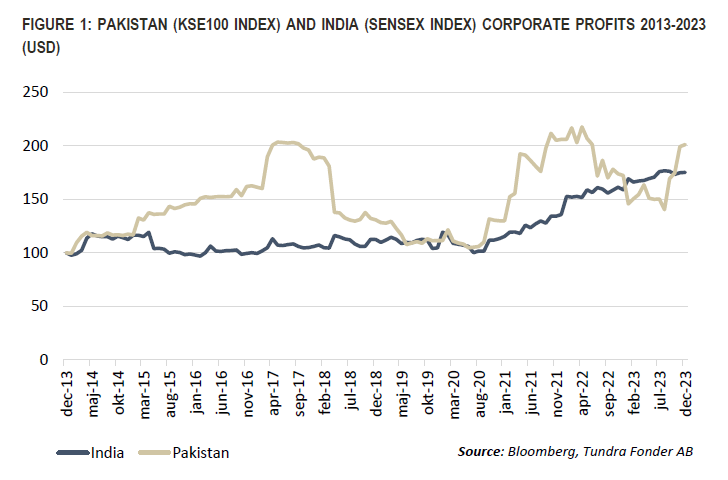

There are two cemented misconceptions among foreign investors regarding investing in small emerging markets. The first is the irrational fear of exchange rate movements (stocks are real assets, meaning over time they compensate for devaluations), and the second is an overconfidence in how the political set-up influences the fundamental performance of companies. Our experience is that if you give companies a somewhat predictable business climate (good or bad), they will learn to navigate this climate. Our positive attitude towards Pakistan has never been about how well the country is managed by its politicians, but about what we see the companies delivering. Given that India (after the USA) has been one of the world’s most popular stock markets in the last decade, it has become a good example country to compare with. In the last ten years, despite political and economic crises, Pakistani companies have actually shown stronger profit growth than Indian companies in US dollar terms (see Figure 1).

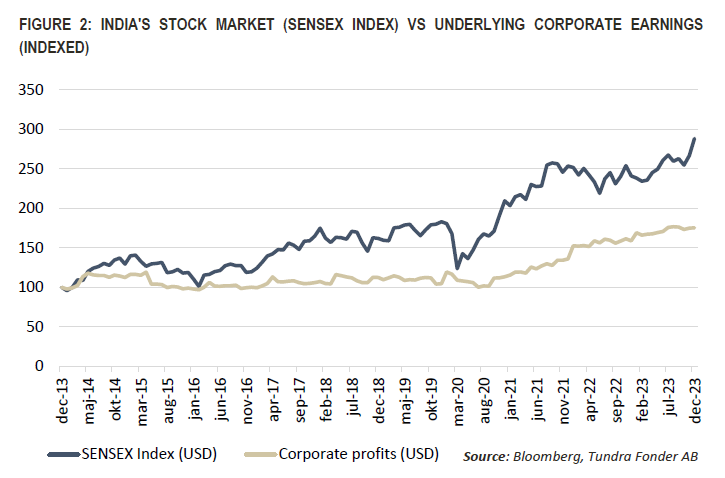

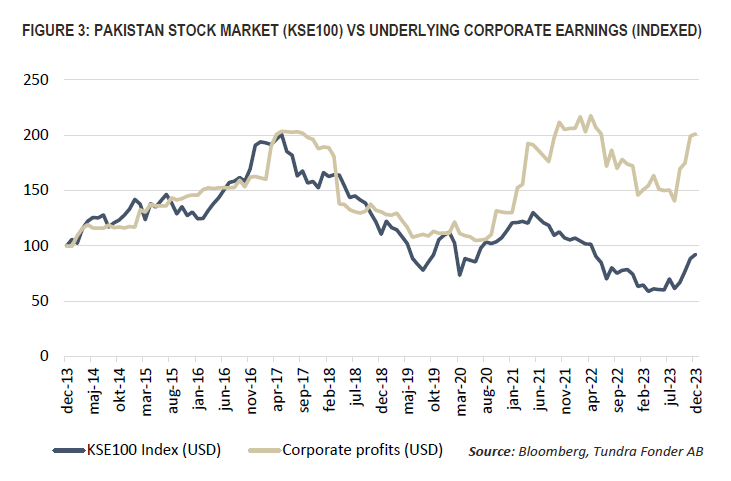

While India has outwardly displayed political and economic stability, the headlines in Pakistan in the same areas have been almost exclusively negative. This means that the equity market has not followed the profit trend at all, which can be seen in Figure 2 & 3 that compare the equity markets in India and Pakistan relative to the respective profit generation for the companies in the respective indexes (USD).

Corporate profits in India have risen 75% over the past ten years and have been rewarded with an equity market return of almost 200%. During the same period, corporate profits in Pakistan have risen 100% while the equity market has given a negative return. It shows how important it is for a country to present a positive image to investors. Countries that, at least outwardly, can demonstrate political and economic stability are rewarded. Countries that exhibit the opposite are weighed down by investors’ pessimism until stability is reinstated. As investors, we must respect that optimism and pessimism will always be an important factor for the short-term performance for equity markets, sometimes even the medium-term performance. More important to remember, however, is that this optimism or pessimism is based on an expected fundamental event (earnings trends), and at some point, investors will evaluate their expectations against the actual outcome. Thus, we remain positive on the equity market in Pakistan, which needs to rise approx. 100% to catch up with the earnings trend and its average valuation over the past ten years (current P/E is 4.6x vs 8.7x in the 10-year average), alternatively having very good protection on the downside in a more pessimistic scenario.

TINUBU TAKES THE NEXT STEP IN NIGERIA

Nigeria’s new president, Tinubu, came to power in the spring of last year, promising to end the country’s failed economic policies of parallel exchange rates and subsidized fuel prices. It started promisingly with an immediate abolition of the fuel subsidies and a devaluation of almost 40%. The former central bank governor was deposed. However, after several years of a non-functioning foreign exchange market, both local and international actors were skeptical. The expected inflows of foreign capital did not materialize, banks continued to build large net positions in US dollars and, perhaps most importantly, inflows of remittances (capital from Nigerians residing abroad) continued to occur through informal channels. In the limited trading that followed, the gap between the “official Naira rate” and the black market widened again due to non-existent supply of foreign currency. Tinubu is now making another attempt which includes forcing forex traders to set rates that reflect the actual supply and demand picture. In doing so, he hopes that all inward remittances, estimated at anywhere between 20-35 billion including informal channels per year (4-8% of GDP), will enter through official channels again.

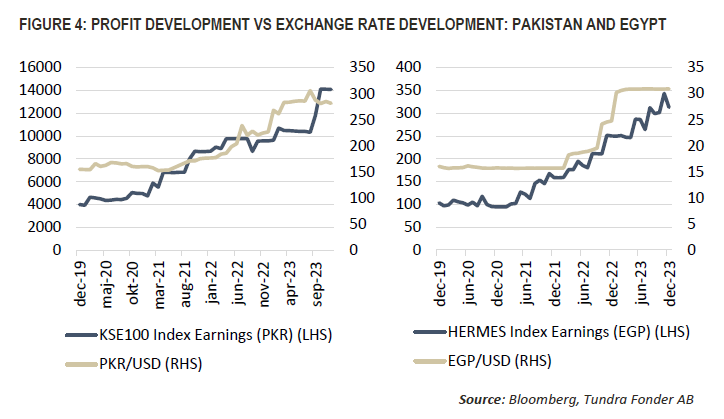

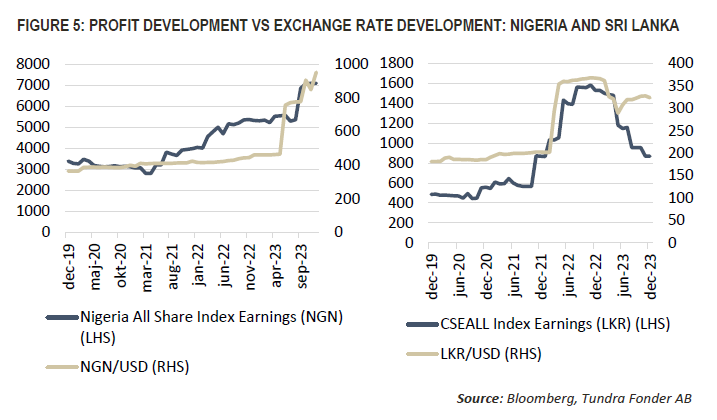

At the same time, restrictions will be imposed on banks’ net exposure to foreign currency. Although it remains to be seen how Tinubu’s new measures will work, we welcome the measures. A functioning currency pricing is based on the premises that all natural flows of currency in the economy go through official channels so that the entire capital balance is reflected in the exchange rate setting. Tinubu’s actions are aimed at restoring this. For the equity market, as we said before: Shares are real assets. Sudden movements in exchange rates can cause a short-term bump in the curve, but of course machinery and information systems purchased abroad do not suddenly become 40% cheaper because the price the local currency is assigned changes overnight. Entrepreneurs must base their calculations on replacement costs for the assets they need in order to run their businesses. This means that they raise their prices, which means that turnover and profits tend to adjust relatively quickly in line with currency movements, something that historical data also shows (see Figure 4 & 5 with examples from Pakistan, Egypt, Nigeria, and Sri Lanka up to end of 2023).

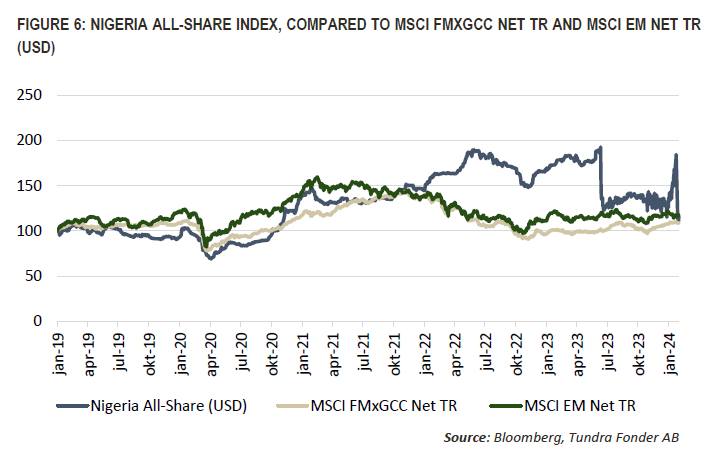

Nigeria has a number of lost years behind it, but as Africa’s largest economy, it also has enormous long-term potential if it starts taking action to rectify the situation. Despite two major devaluations in the last five years, the equity market, in USD, has developed in line with our benchmark index and the MSCI EM index. If Tinubu succeeds in getting the wheels rolling in the economy again, the journey ahead could be interesting.

___________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.