THE FUND SHOWED DEFENSIVE CHARACTERISTICS DURING A TURBULENT MONTH

In USD the fund fell 1.5% in February (EUR: -1.8%), compared with MSCI FMxGCC Net TR (USD) which fell 5.4% (EUR: -5.7%) and MSCI EM Net TR (USD) which fell 3.0% (EUR: -3.3%). An important contributing factor was our overweight in Asia and underweight in Eastern Europe. The latter region was particularly hard hit by Russia’s aggression in Ukraine, while our markets in Asia and Africa fared better. As can be seen from the relative return, our stock selection also worked well during the month.

Our biggest positive contributions came from stock selection in Vietnam where all our 5 holdings rose, despite a slightly weaker market. The best performer among our Vietnamese holdings was Airport Corporation of Vietnam, which operates 22 airports around Vietnam. The stock rose 10% during the month. Declining restrictions in Vietnam are positive for the company as air traffic can revert to more normal levels.

Good contributions were also received from our Egyptian position, GB Auto, which came out with a really strong report during the month. The stock rose 20%. Both their vehicle assembly business and the, in our eyes, more exciting financial services business exceeded expectations. Profit rose 61% in 2021, while sales increased 35%. For 2022, we expect lower profit growth, albeit continued double-digit. The company’s valuation of 4.5x 2021 net income remains too low in our opinion.

Our biggest negative contribution during the month came from Pakistan, where one of our favorite positions, the IT company Systems, fell 13%. The stock has fallen close to 20% from the peak in recent months, probably as a result of lower global investor appetite in the sector. In the IT sector, however, a distinction must be made between companies and companies. Systems is a very profitable company that acts as a subcontractor to companies all over the world with programming services and updating of IT systems. It is a cost-effective alternative for basic services that are needed continuously by all major companies, today and tomorrow. Even though the company has had operations abroad for decades, we note a significant breakthrough during the last two years which leads us to believe they have a few years of harvesting ahead of them. The company is valued at around 18x the expected profit for 2022. It should be set against the long-term goal of sustainable top-line growth by 25% per year with maintained profitability. Right now, the company is growing faster than that and we believe the conditions are good that this will continue for at least the next few years. Powerful expansions will from time to time hit the margins of individual quarters, and Systems will also be affected by this at some point. For us as long-term shareholders, this does not matter. The important thing is that the management remains focused and continues its long-term journey to lead Pakistan’s IT sector forward.

The eyes of the whole world are of course currently resting on Ukraine and the invasion initiated by Russia. Equity investors are focusing on assessing the long-term consequences of Putin’s aggression and the economic sanctions that followed. A fairly obvious risk is that we will see another sharp rise in commodity prices. Most of the countries we invest in import most of the raw materials used. Higher prices affect their trade balance, raise inflation and may put further pressure on currencies. Of course, there is also the risk of unknown Russian exposures in the global financial industry that could come to the surface. This remains a risk factor for all stock exchanges in the world. If we were to try to mention something positive from the situation we are currently going through, it is that the very strong and united reaction from the global community is stronger than expected. The strong sanctions that have now been imposed on Russia should give countries in potentially similar situations food for thought. Regardless of what rights you as a country think you have, the storm that hit Russia in the wake of the invasion will need to be taken into account. One potential global conflict that comes to mind is the ever-present risk with China and Taiwan.

Regardless of the despair we as humans might feel about the situation in Ukraine, our task is to manage the capital our unitholders have entrusted to us in the best possible way. External unrest is not good for any market and our markets have also felt their share. The fund has however navigated the turbulent waters well so far. As revealed by our relative returns, our stock selection is the most important reason. Long-term positioning in the best companies in growth markets, rather than jumping between themes or countries, is Tundra’s way of managing. This investment style also enables our long-term work to support and influence our portfolio companies in their sustainability journey. Even adjusting for our excess returns, we conclude that our markets have been more resilient than outside investors would have thought. There are a number of possible reasons for this, some of which we have discussed before:

- Tundra’s exposure in Eastern Europe accounts for just under 2% of the fund and the majority of investments are instead in Asia. The distance to the conflict as well as the limited relations with both Russia and Ukraine have helped.

- While we in the West have almost returned to normal life, the fear of COVID-19 has remained high in most of our countries. Less knowledge and limited healthcare services are partly to blame. During the month, a number of our countries announced a significant easing of restrictions. We in the richer countries of the world sometimes forget that people in many parts of the world do not always have the opportunity to put food on the table at home.

- The foreign participation rate in our markets is historically low (5-20%) and foreigners have sold most of their exposure in the last 7-8 years. The remaining selling is for natural reasons limited. This means that we are less sensitive to the nervousness of foreign investors in situations like this.

- With Vietnam as the only real exception, local investors have gone through a number of tough crises in the last 7-8 years, which means that their concerns and crisis awareness were already at a fairly high level before Ukraine. Without in any way downplaying the seriousness of the situation in Ukraine and Russia, this is for local investors only another cause for concern.

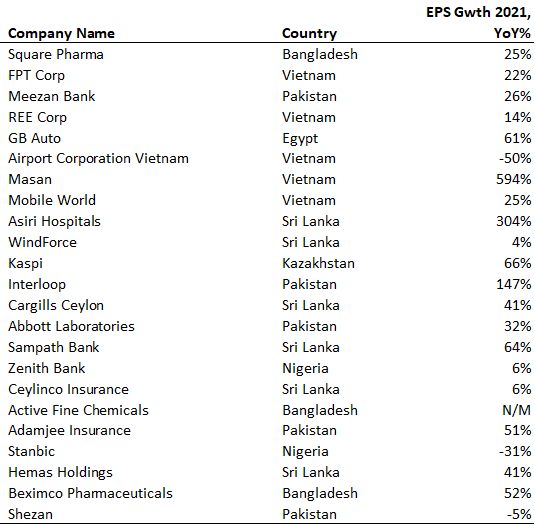

As we have discussed for some time, the valuations in our markets vary between reasonable and low from a historical perspective. To date, 23 (out of 39) portfolio companies (60% of fund assets) have reported their results for the fourth quarter of 2021. 19 of 23 (55% of fund assets) increased profits in 2021. The median increase in profit growth was 29% (see table).

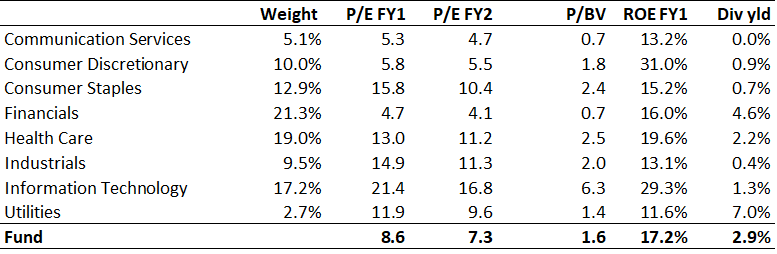

We usually mention the fund’s valuation relative to the current year’s estimated profits and the subsequent year. As more of our companies report results for 2021, the estimates for the current year of those companies are rolled over to 2022. The fund’s valuation at the end of February amounts to 8.6x the current year’s profits and for the coming year 7.3x. The return on equity during the current year is expected to be 17.2%, the dividend yield is estimated at 2.9%. The dividend payout ratio is thus about 25%. In line with Higgins’ model for sustainable profit growth (assuming unchanged Return on Equity and without the addition of new capital or debt), this indicates that the companies in our portfolio with current profitability will be able to grow around 13% per year sustainably. Our markets will not be immune to strong external turmoil, but expectations are low, which indicates reasonable to good market return in the coming years.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.