THE FUND ADDED FURTHER ALPHA IN THE LAST MONTH OF THE YEAR

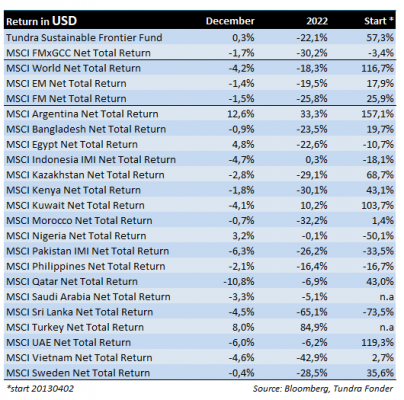

In USD the fund rose 0.3% (EUR: -2.6%) during December, compared to the fund’s benchmark index MSCI FMxGCC Net TR (USD) which fell 1.7% (EUR: -4.5%), and MSCI EM Net TR (USD) which fell 1.4% (EUR: -4.2%). In terms of absolute contributions in USD, it was mainly Egypt (8% of the portfolio) that contributed positively during the month. Our sub-portfolio rose by 13%, which gave an absolute contribution of 1% to the portfolio. In terms of absolute negative contributions, it was mainly Pakistan (19% of the portfolio), where the sub-portfolio fell during the month by 6%, which translated into an absolute negative contribution of 1.2%. Our Indonesian sub-portfolio fell 2% during the month, which contributed negatively by 0.2% to the total return. Measured relative to the index, the fund was helped during the month mainly by good stock selection in Vietnam. Our sub-portfolio (roughly 24% of the fund’s assets vs. 30% for the benchmark) rose 3%, compared to the index which fell 5%. This gave a relative contribution to the index of 2.1% during the month. Relative to the index, it was primarily Pakistan (-1.2% relative portfolio contribution) and Indonesia (-0.2%) that contributed negatively.

Among individual holdings, in USD, our two Egyptian holdings, Juhayna Foods (+47%, +0.6% portfolio contribution) and GB Auto (+15%, +0.5% portfolio contribution) were the main contributors. Juhayna’s performance can probably stem from the fact that there have been some strategic buyers in the share since a couple of months ago which from time to time leads to short-term sharp movements. In the case of GB Auto, we note that one of the largest brokerage firms published a new analysis in which the significant undervaluation of GB Capital (a financial services arm), which we have previously discussed, was spotlighted.

On the laggards’ list, two of our Pakistani holdings, Systems (-4%, -0.4% portfolio contribution) and Meezan Bank (-10%, -0.4% portfolio contribution), were weighed down by negative sentiment given the great uncertainty Pakistan is currently in. Our Indonesian holding Media Nusantara (-6%, -0.3% portfolio contribution) also performed negatively, mainly due to weak general stock market performance in Indonesia.

2022 – WORST POSSIBLE CONDITIONS BUT GOOD STOCK SELECTION ALLEVIATED THE DECLINE

For the year as a whole, in USD, the fund fell 22.1% (EUR: -17.4%), which can be compared with the fund’s benchmark index, which fell 30.2% (EUR: -26.0%), and the MSCI EM Net TR (USD) which fell 19.5% (EUR: -14.6%). 2022 was the fund’s worst year since its inception, but it could have been significantly worse. The fund’s thematic focus on primarily low-income and lower-middle-class countries, where the majority of raw materials are imported, has meant difficult conditions in the wake of the war between Russia and Ukraine. Most of the fund’s markets have had a very tough year. In USD Sri Lanka (-65%) and Vietnam (-43%) performed particularly negatively. Good stock selection, however, eased the decline. In Vietnam in particular, we did well in 2022. Our choice to focus on non-cyclical holdings and avoid the banking and real estate sectors proved to be the right choice. Our sub-portfolio fell marginally during the year (-3%) compared to the market which fell 43%. Our five holdings all performed better than the market. Our second largest Vietnamese holding, renewable energy producer REE Corp, managed to return 16% in USD during the year. Our Vietnamese sub-portfolio overall added 13% relative performance vs. our benchmark which mitigated declines in Sri Lanka (-2.7% contribution relative to the index, our sub-portfolio fell 51%), Pakistan (-3.3% contribution, our sub-portfolio fell 24%) and Egypt (-2.2% contribution, our sub-portfolio fell 33%).

2022 was supposed to be a year of recovery when historically extremely low valuations would have the conditions to normalize. Russia’s aggression in Ukraine changed the scenario completely. Raw material prices skyrocketed, which affected several of our countries negatively. During the year, Pakistan devalued its currency by 22% against the US dollar, Egypt by 37%, and Sri Lanka by as much as 45%. Averaged across the fund’s 7 largest markets, this was the worst year for currency markets in over 30 years, worse than the 1997-98 Asian crisis and even worse than the 2008 global financial crisis.

2023 – STILL GREAT UNCERTAINTY BUT WELL DISCOUNTED BY THE MARKET

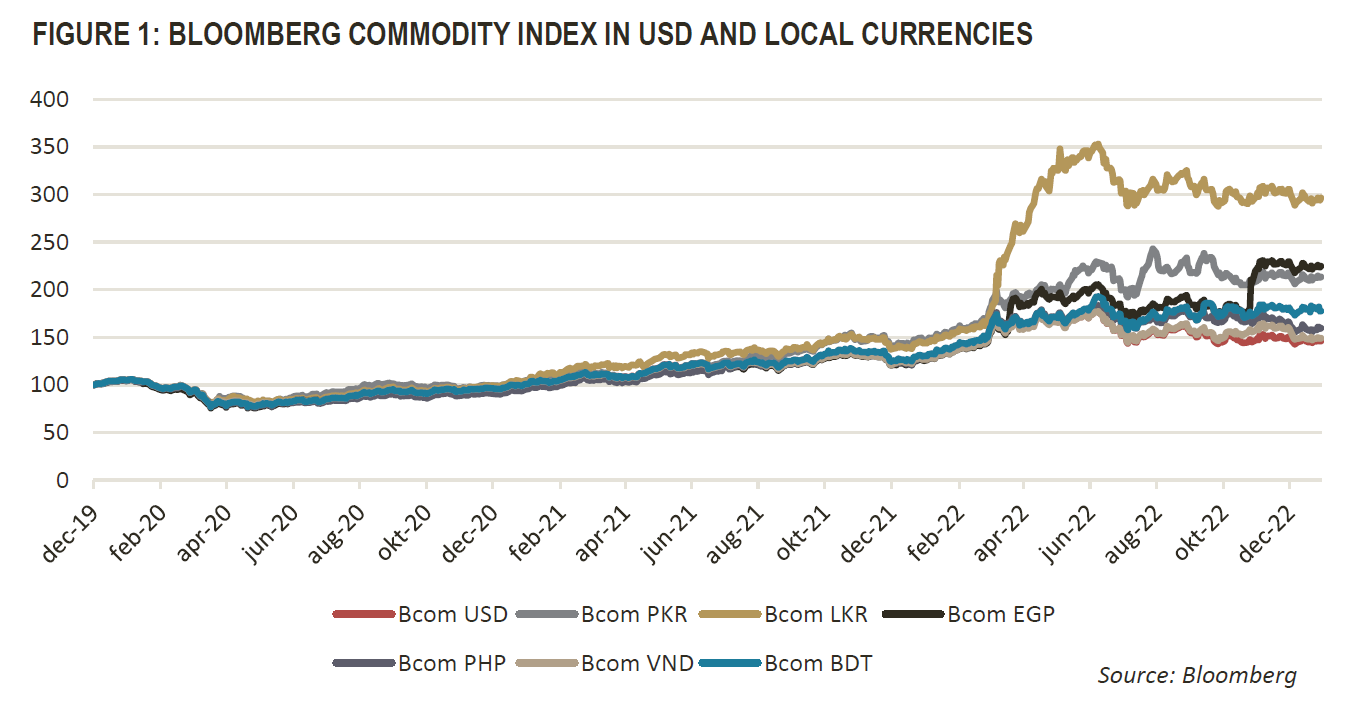

We enter 2023 with significant remaining uncertainty. Figure 1 below shows the Bloomberg Commodity Index converted to exchange rates in the fund’s most important markets since the end of 2019. Calculated in USD, commodity prices have risen by around 50% during the period, which partly explains the higher global inflation during the period. As can be seen in the graph, however, weakened currencies have meant that the price effect has been significantly higher in several of the fund’s more important markets. E.g., in Sri Lanka, commodity prices have increased by nearly 200% during the period, and in Pakistan by 120%, etc.

This in turn means that our countries have been particularly hard-pressed, both concerning inflation trends and from a trade balance perspective. As you know, inflation is normally expressed as price trends on an annual basis. If commodity prices do not continue upward, this means that the price effect from commodities in USD will be neutral to negative from March 2023. Given the weaker currencies in our markets, the effect is slightly delayed. In the Philippines and Vietnam, the timing occurs in April, in Pakistan and Sri Lanka it occurs in May. In Egypt, which relatively recently carried out another major devaluation, relief will only come in December 2023. Even if commodity prices remain at current levels, it will take a few more months before this is visible in the inflation statistics. Although one can sense the light at the end of the tunnel, several of our countries, especially Pakistan, Egypt, and Bangladesh, are in a very stressful situation where the probability is high that we will see some additional one-off adjustments in the exchange rates. The first half of 2023 will continue to be tough, even if it will be difficult to repeat the shocking development in 2022.

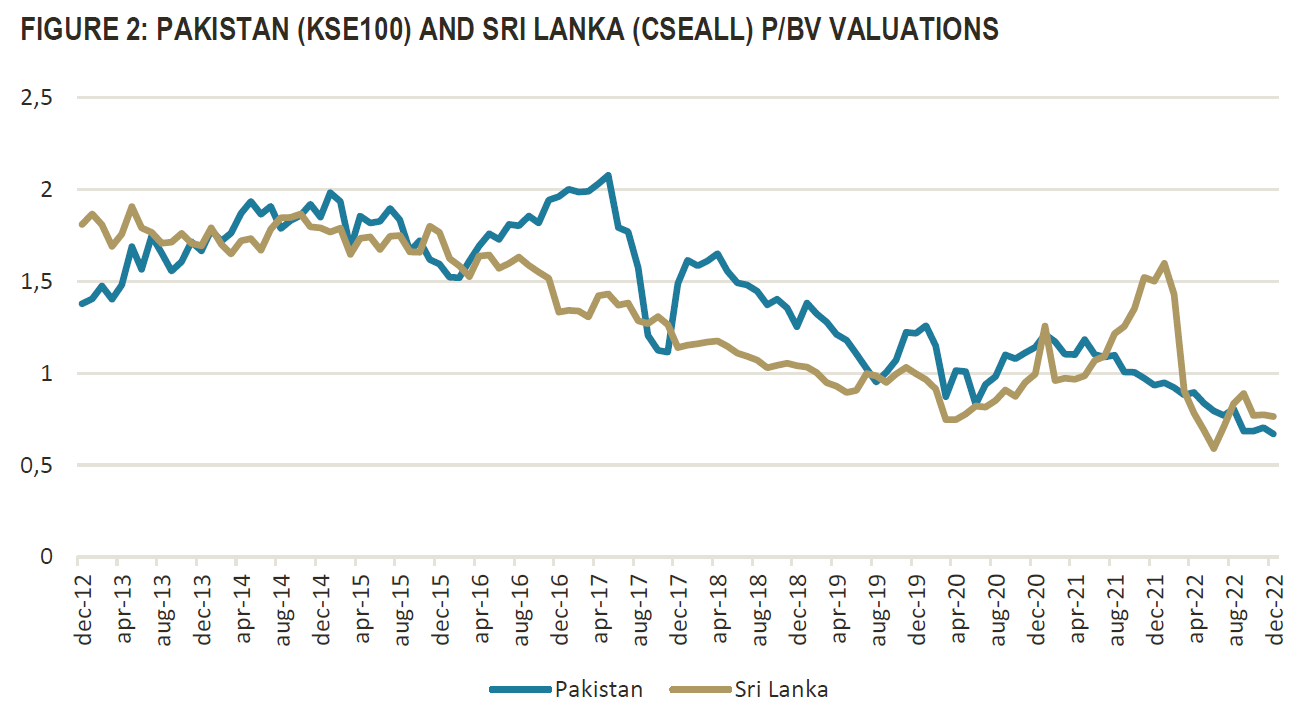

Of our more significant markets, Pakistan, uncertainty is currently at its pinnacle. The current coalition, which is a mixture of parties with ideologically very different backgrounds, has been an unfortunate solution. The coalition already lacked the support of a majority of the population when they came to power in the spring of 2022 and the situation now appears to have become unsustainable. In desperate attempts to win back confidence ahead of the planned elections in the fall of 2023, rational economic policy has had to stand aside, temporarily halting disbursements from the IMF. There are, therefore, concerns that Pakistan’s opportunities to extend the multi- and bilateral loans that the country’s foreign debt primarily consists of will not be possible. Some form of restructuring of Pakistan’s debts now seems inevitable. As we said earlier, Pakistan’s situation is significantly different from Sri Lanka’s. Most of the country’s external debt consists of bilateral and multilateral loans with countries with which Pakistan has strong and long-standing friendships (China and the Gulf countries). Restructuring can thus be relatively undramatic if the political deadlock is broken. Whether measuring equity valuation or P/E ratios, Pakistan is at levels investors have not seen in decades, and even below Sri Lankan levels.

Just before the publication of this monthly letter news broke that Pakistan potentially have secured slightly more than USD 9 billion in support for the flooding disaster earlier this year. If it materializes it could help the country bridge the current very difficult situation and would mean desperately needed alleviation for its people. But for investors to be able to look ahead, however, a prerequisite is that the current political deadlock is broken. We, therefore, hope we will see a decision regarding the political continuation early in 2023.

If we sum up our thoughts, we note that even in a more positive scenario, it will take a couple of months into the year before the news flow in our markets improves, and 2023 will be a year when most countries at best lick their wounds. As always when it comes to the stock market, however, it is not about how good or bad the conditions are, but how well investors price them. How overconfident, or fearful, they are.

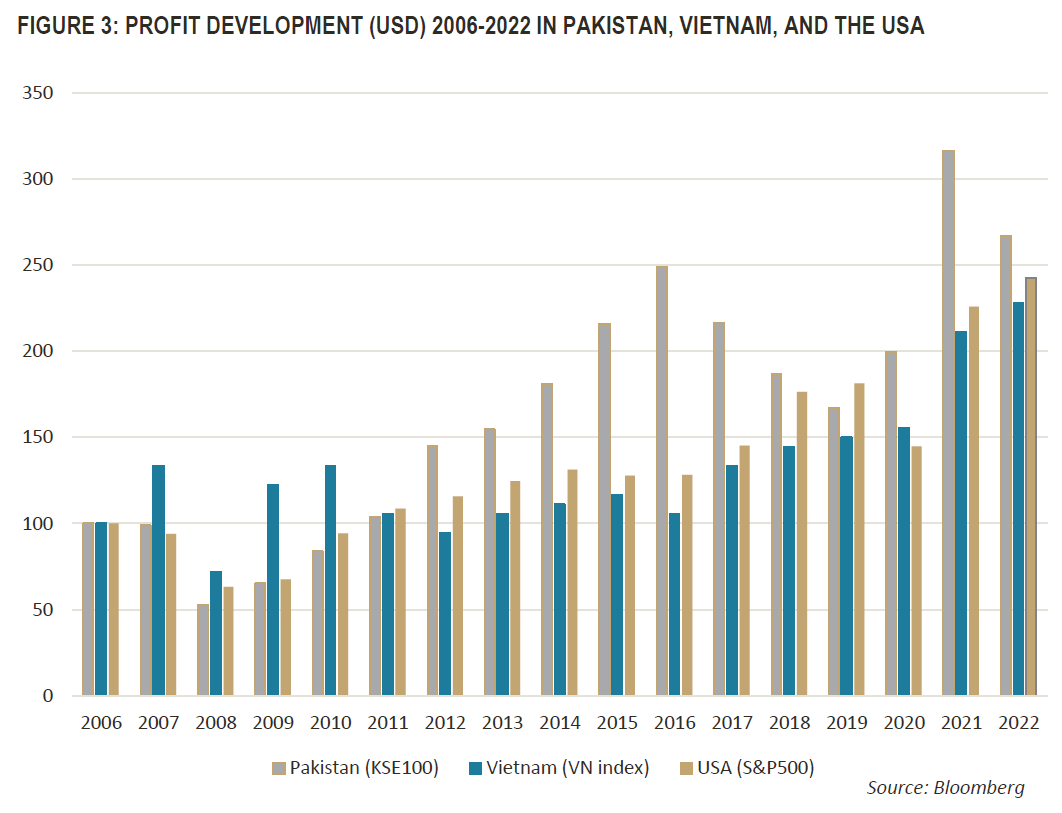

For a fund manager who deals with several of the trickiest markets in the world and who has also worked against decent headwinds for a couple of years, it is reasonable to question where our optimism comes from. The answer lies in the actual profit development over time, despite constant crisis headlines. If we take the fund’s two largest markets, Vietnam and Pakistan (together 43% of the fund’s assets), as an example, we note that the profit performance (in USD) of both stock markets over the past 16 years (as far back as statistics are available via Bloomberg) delivered in line with the USA, a country that you can probably say had at least ten years with fairly ideal conditions (zero interest rate climate with the possibility to leverage to a completely different extent than is possible in less developed stock markets).

During the same period (2006-12-29 – 2022-12-30 in USD), the stock market in Pakistan has risen 8%, Vietnam 109%, and the USA 274%. One can of course invoke several explanations, e.g. the outflow of capital from our markets to more developed ones given the historic zero interest rate climate in the West, political uncertainty, economic uncertainty, currency depreciations, etc., etc. An indisputable fact is, however, that stock markets over longer periods will reflect the underlying earnings trend. Our readers are aware by now that our absolute strength is to select good companies, regardless of which markets we invest in. Since the fund’s launch, this has meant that the fund has given an excess return of 61% against its benchmark and a 38% higher return than the broader emerging markets index. We cannot influence how the market chooses to value the profits our companies generate. We can continue to invest in what we believe are the best companies, guided by our investment philosophy, where fundamentals and sustainability are prerequisites. We believe great companies not only serve their shareholders but also benefit their markets and the people who live there to continue to develop.

______________________________________________________________________

TUNDRA SUSTAINABLE FRONTIER FUND REPLACES THE SWAN WITH THE EU’S REGULATIONS FOR SUSTAINABILITY

In connection with the new EU regulation under the Sustainable Finance Disclosure Regulation (SFDR), new requirements are applied to funds’ sustainability work as of March 2021. Tundra has therefore decided on July 4 not to continue with the Nordic Ecolabelling of the fund. According to the new regulations, sustainability reporting must take place in a uniform manner and funds are divided into different categories. The Tundra Sustainable Frontier Fund is classified as an Article 8 fund (Light green: promotes environmental or social characteristics). The investment philosophy of the fund remains the same; management of the fund and is not affected by the change.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.