CORRECTION DURING THE AUGUST

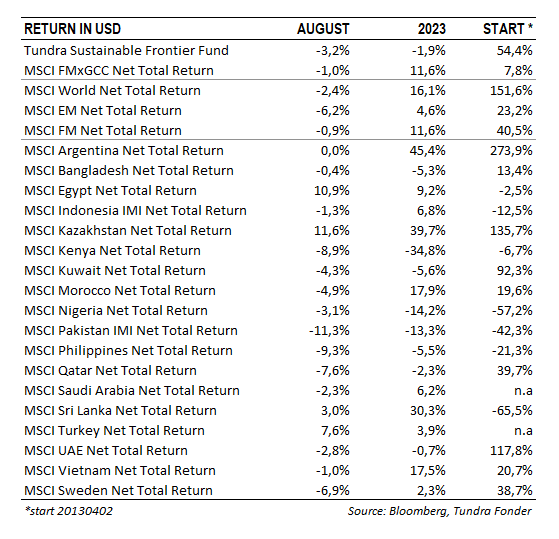

In USD, the fund fell 3.2% during the month (EUR: -1.5%), compared to MSCI FMxGCC Net TR (USD), which fell 1% (EUR: +0.7%) and MSCI EM Net TR (USD), which fell 6.2% (EUR: -4.5%). In terms of absolute return, the largest positive contributions during the month were received from Kazakhstan (0.6%) and Sri Lanka (0.4%). The largest negative contributions were obtained from Pakistan (-2.1%) and Indonesia (-1.1%). The latter two markets also accounted for our main underperformance against the index in August.

WINNERS AND LOSERS DURING THE MONTH – AND A NEW HOLDING

Among individual holdings, we noted several major movements during the month. The fund’s largest position, the Vietnamese IT company FPT (9% of the portfolio), rose 12% in August, partly on rumours that an international player would be interested in taking a larger stake in the company. Given the diversified ownership of the company, we view such an event as complicated and unlikely. Another portfolio company that stood out was Kazakh fintech company Kaspi (5% of the portfolio), which rose 13% during the month. The company’s buyback program continues. The 2022 Kazakh unrest followed by Russia’s invasion of Ukraine significantly affected the Kazakh market, and the company’s share fell by more than 70%. Since then, the stock has gradually recovered but is still 35% below the peak levels of autumn 2021. Based on the forecasts for the full year (USD), the turnover this year will be 67% higher than in 2021, and the net profit is expected to be 70% higher than in 2021. The valuation of just under 11x the expected profit for 2023 can be compared with a historical valuation of just over 20x in 2020 and 2021. Current forecasts point to a continued profit growth of just over 30% in 2024. The “Russia frenzy” that sank the company in 2022 is understandable given Kazakhstan’s historical connection to Russia, but has primarily affected the valuation of the company, rather than the business so far.

Our Sri Lankan companies developed well during the month. Foreign investors have gradually returned to the market. In August, our Sri Lankan renewable energy company Windforce (2% of the portfolio), as part of a consortium, won Sri Lanka’s largest solar procurement to date, a 100 MW solar power plant. The stock rose 9% during the month. Our food retailer, Cargills Ceylon (2% of the portfolio), rose 7% during the month mainly due to foreign buying interest. In USD terms, the stock has now recovered most of what was lost during Sri Lanka’s economic crisis (spring 2021 – spring 2022). The valuation of just over 16x this year’s expected earnings has normalized, although it remains some distance from the levels of 2010-2014 when it varied in the range of 20-40x. Probably thanks to the difficult years the company has gone through, its capital allocation has improved significantly, which can be seen in, for example, the return on equity, which for 2023 is expected to land at 23%, compared to 5-17% in 2010-2014. As we usually say, crises can be difficult, but they also tend to make strong companies stronger.

The biggest negative contribution during the month came from our Indonesian media company Media Nusantara (4% of the portfolio) which fell 17%. This follows a disappointing half-year report, primarily due to falling advertising revenue from their TV channels. This, in turn, can be partly attributed to a troubled advertising market after Indonesia continued to introduce mandatory digital TV broadcast in a phase-wise manner across Indonesia. In the short term, this has excluded a part of the population who still uses analog TV, and this has led to less spending by advertisers on TV commercials. During the month, we had a follow-up meeting with the company when they noted continued problems in the advertising market, while at the same time expressing a hope that advertising revenue will recover before the presidential election in early 2024. The valuation of just over 4x net profit remains undeservedly low given the hidden values we consider it has in its digital assets.

Our Pakistani IT company Systems Ltd (6% of the portfolio) fell 10% during the month after a result that came in below expectations, primarily due to lower margins. Recent acquisitions and continued significant new hires had a negative impact, while the company continues to grow significantly faster than the long-term ambition of 25% per year. During the second quarter, turnover rose by just over 100% (40% in USD) y-o-y. The primary growth area for the company currently is the Middle East, which now makes up 52% of revenues. The number of customers has risen to 150, compared to 100 at the end of 1H22. With a turnover of just over USD 160m on an annual basis, the company remains a drop in the ocean from a global perspective (1.0% of Indian Infosys and 0.5% of Tata Consultancy), and we look positively on its continued focus on expansion, even if it means that there will be periods when margins suffer.

The fund has taken a small position in the Turkish company Logo. The company is Turkey’s leading ERP solution provider in the category of small and medium-sized companies and is the leading player in Turkey’s ambition to digitize smaller companies’ accounting and invoicing. This is a good example of when we find structural growth outside our traditional hunting grounds (low-income and lower-middle-income countries) which has more to do with the nature of the business than the economic phase the country is in. Digitizing the economy is an important area for emerging markets in their efforts to reduce corruption and streamline tax systems. For the companies, there are significant productivity gains to be gained through more efficient administration. Investment opportunities in this type of business tend to emerge a little later in a country’s growth journey and the successful companies have 20-30 years ahead of them to try to replicate the growth that companies such as Swedish Fortnox have historically achieved. Another portfolio company in the same category, albeit in a different sector (fintech), we have Kazakh Kaspi.

IMPORTANT COUNTRY NEWS

In USD, Vietnam fell 1% during the month. Declining global economic activity has hit the country’s trade (both exports and imports) in the short term and negatively affected the population’s propensity to consume. However, the trade surplus for the first eight months of the year of USD 20.2 billion is the highest the country has ever shown, and both exports and imports have increased for four months in a row up to August, something we have not seen since 2020. Committed foreign direct investment increased for the fifth month in a row and rose during August by a whopping 54%, albeit from a low base. Notably, China’s committed FDI increased by 91% year-on-year in the first 8 months of the year, the highest growth since 2019. On September 10, US President Joe Biden will visit Vietnam to discuss the countries’ cooperation. A very odd event during August was when the Vietnamese conglomerate Vingroup listed its electric car manufacturer VinFast through a SPAC listing in the US (with less than 1% free-float). After just over three years of operation, the company is expected to deliver just under 50,000 cars in 2023, and the product quality reviews have been (to put it mildly) mixed. The company should have a maximum turnover of USD 200 million this year and has been losing money for several years. The need for capital was probably the reason why Vingroup was forced to sell its promising food retail chain to the Masan Group. At its highest during the month, the company reached a valuation of close to USD 200 billion (!) only to end the month at approximately USD 80 billion. For comparison, Chinese electric car maker BYD can be mentioned, which manufactures just over 3 million vehicles, has a turnover of USD 23 billion, is profitable, and is valued at just under USD 100 billion. We won’t even go into the complexities of succeeding as a late entrant in a capital and R&D-intensive industry that increasingly resembles a hornet’s nest. We thought these kinds of crazy SPAC stories were a thing of the past and are surprised that they are still being repeated. Unfortunately, the losers are often retail investors who are drawn into speculation tangles.

Pakistan fell 11% during the month, after the substantial rise in July. During August, the incumbent government handed over power to an interim government (on paper a politically neutral constellation tasked with running the country until the election). Relatively immediately, however, it emerged that they intend for the interim government to sit until sometime into 2024. The official explanation is that they want the election to be based on the recent census, which they claim is technically not ready. The decision has generated some criticism, primarily within the country. Given that it is the head of the army who now takes the most important meetings with foreign investors, we don’t really see any practical difference. Easing of import restrictions meant the country’s current account slipped back into negative territory in August, and although inflation fell to 27% (from 28% in July), the economic situation remains dire. The currency weakened a further 6% against the USD during the month, given increased imports and as a market-priced currency is part of the agreement with the IMF. A positive surprise was that Pakistan’s country weight in the MSCI Frontier Index during the month increased from 0.6% to 2.9%. This happened due to changes in MSCI’s methodology to calculate index weights where greater focus is placed on liquidity, rather than market capitalization. We think it is a wise decision and for Pakistan, it means that more index-monitoring investors will find it harder to ignore the market, which remains historically undervalued (the KSE100 index valued at P/E 3.7x on expected earnings for the full year 2023).

Sri Lanka rose 3% during the month. The central bank paused its interest rate cuts despite inflation falling further to 4% year-on-year in August. Ongoing discussions regarding the privatization of several state-owned companies were received positively, while we continue to await results from the ongoing discussions with private owners of USD-denominated bonds.

PROSPECTS AHEAD

We have had a shaky year behind us where several of our traditional core markets had a hard time, and our stock-picking in the largest markets (Vietnam and Pakistan) did not protect us. It is very reminiscent of the period from spring 2018 until summer 2019. Given our long-term investment horizon and very high active share, years like 2023 are unavoidable from time to time. Our average annual excess return, after fees, taxes, and all other costs, is at about 4% per year since the start just over 10 years ago. It is an acceptable added value delivered to our unitholders, and we hope that we can increase this gap again going forward.

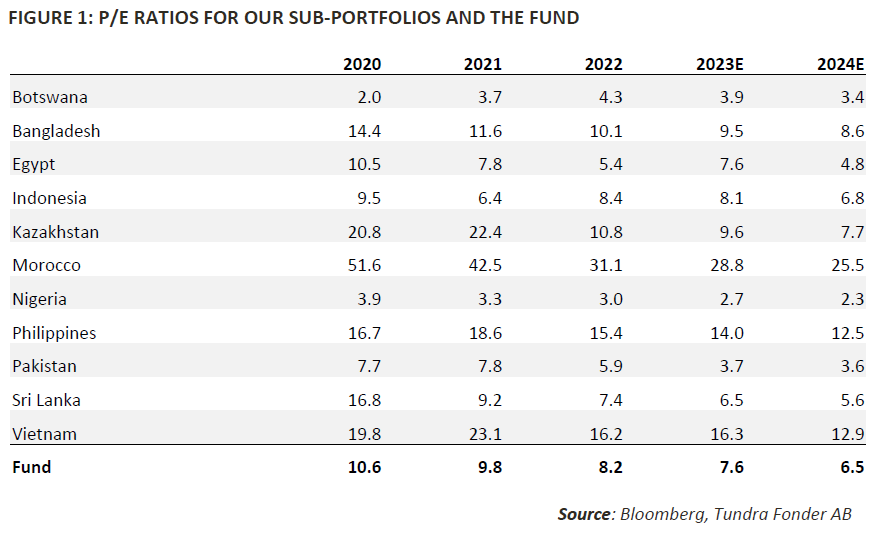

The headlines in the majority of our markets remain quite deplorable, but as an investor, you should remember that equity markets are forward-looking. As a rule of thumb, the condition the equity markets are in today tends to reflect the reality about 6 months later, and we do not see that our markets will be in a worse condition in 6 months than they are today. Valuations remain low with an average valuation for the portfolio at P/E 7.6x 2023 expected earnings and 6.5x for 2024. The exact same portfolio (pro forma) was valued at 10.6x in 2020. It reflects the anxiety our markets have gone through but also signals that only a slightly less pessimistic investment climate can provide a fairly nice recovery, while also providing significant protection if the global investment climate deteriorates further.

___________________________________

TUNDRA SUSTAINABLE FRONTIER FUND REPLACES THE SWAN WITH THE EU’S REGULATIONS FOR SUSTAINABILITY

In connection with the new EU regulation under the Sustainable Finance Disclosure Regulation (SFDR), new requirements are applied to funds’ sustainability work as of March 2021. Tundra has therefore decided on July 4 not to continue with the Nordic Ecolabelling of the fund. According to the new regulations, sustainability reporting must take place in a uniform manner and funds are divided into different categories. The Tundra Sustainable Frontier Fund is classified as an Article 8 fund (Light green: promotes environmental or social characteristics). The investment philosophy of the fund remains the same; management of the fund and is not affected by the change.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.