CAUTIOUS RECOVERY IN APRIL

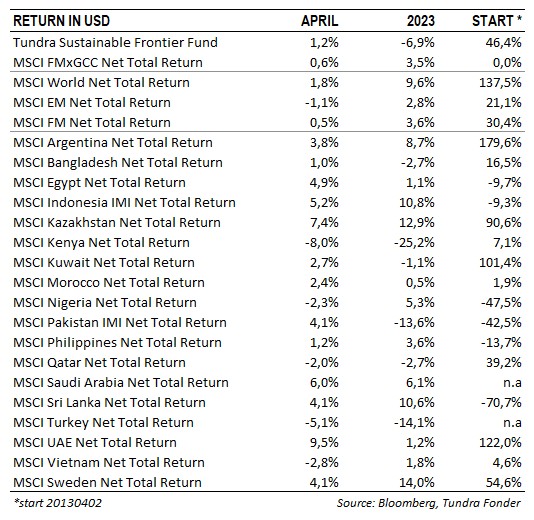

In USD the fund rose 1.2% (EUR: +0.3%) during the month of April, compared to the fund’s benchmark MSCI FMxGCC Net TR (USD) which rose 0.6% (EUR: -0.4%) and MSCI EM Net TR (USD) which fell 1.1% (EUR -2.1%). Calculated in USD, the largest absolute contributions were received from Egypt (+0.9% portfolio contribution, sub-portfolio rose 13%) and Kazakhstan (+0.4% portfolio contribution, sub-portfolio rose 11%), while the largest negative contributions were received from Vietnam (-0.6%, the sub-portfolio fell 2%) and Morocco (-0.1%, the sub-portfolio fell 3%). In Egypt, it was primarily the fund’s largest Egyptian holding, GB Corp (previously GB Auto) that contributed. The stock rose 27% during the month without any particular news. Even post the rise, the valuation remains undemanding (P/E’23E 4.2x) given the strong growth in the company’s financing business. In Kazakhstan, our only position in the country, fintech company Kaspi, rose 11% after releasing another report that beat expectations. In Vietnam, Masan Group fell 7% ahead of its first quarter report. The report released on April 28th came in slightly below expectations, but the stock recovered slightly after the announcement.

18 of our portfolio companies released their results for the first quarter during the month. There were small deviations relative to expectations, but some are worth highlighting. The Vietnamese real estate crisis that began last year and the continued weak export orders have started to impact the propensity to consume and continue to weigh on consumer demand, something we also noted in the fourth quarter reports. Vietnamese consumer conglomerate Masan Group (4% of the fund) delivered a below-expected result, with costs associated with the continued expansion of the grocery chain Winmart combined with weaker consumer demand and lower profit contributions from banking business weighing on results. Also in the report from the Vietnamese leading IT-consultant FPT (9% of the fund), we saw a clear slowdown in the local demand for IT services (-5% on an annual basis), but this was compensated by unexpectedly strong demand internationally where sales increased by a whopping 32%. The order book rose 44% compared to the same period last year, which bodes well for the remainder of the year. Overall revenue rose 20% in the first quarter, while profit after tax rose 21%. REE Corp (7% of the fund), which operates primarily in renewable energy, saw profits in the first quarter increase by 7% year-on-year while revenue rose 15%. We have expected a slight drop in profits in 2023, given that their hydro business had an exceptionally good year in 2022 with unusually high water levels. During the month, however, the company guided for unchanged profit in 2023, which is likely to cause some revisions upward on profit estimates.

In Pakistan, the picture was generally positive. As expected, our largest Pakistani holding, IT company Systems Ltd (7% of the fund), delivered a strong report with sales up just over 100% compared to the corresponding quarter in 2022, and profits up just over 200%. The result was heavily doped by exchange rate gains from the devalued PKR, with 85% of the company’s revenue coming from exports. A good hedge in troubled times but should not be extrapolated. The company has recently expanded into new markets (e.g. Saudi Arabia, Egypt, South Africa, Australia, and Singapore), which means increased costs are expected to weigh on margins throughout the year. We noted a certain slowdown from the American market, which was however more than compensated by unexpectedly strong development in the Middle East. Pakistan’s Meezan Bank (3% of the fund) impressed with earnings growth of nearly 70% year-on-year in the first quarter. The currently very high interest rate situation in Pakistan favours the bank’s net interest income and the forecast for the full year of a profit of PKR 31/share (P/E’23E 3.2x) looks conservative. However, Meezan Bank is also currently benefiting disproportionately from the current troubled climate in Pakistan and should from next year come down to more normal profit growth of 10-20% per year. Worth noting is that the bank has doubled its earnings, in USD, over the last three years, an impressive achievement given the problems Pakistan has faced during this period. The clothing manufacturer Interloop (2% of the fund) also released a strong report. Just like Systems Ltd, Interloop also benefits from the fact that more than 90% of sales come from exports. The extremely strong last quarter will not be representative for the rest of the year, but if we look at the rolling twelve-month rate, revenues increased by just under 40% and profit after tax by just over 100%. In addition to the company benefiting from the weaker Pakistani rupee, it also rides strongly on its strong sustainability profile with structurally growing demand from increasingly aware buyers. We often talk about the importance of choosing companies that are adapted to the local conditions. Systems, Meezan and Interloop currently make up 75% of our Pakistani sub-portfolio and have done well despite the macro concerns.

Kazakh fintech company Kaspi’s (4% of the fund) result was impressive again, exceeding expectations. Profits rose 52% year-on-year, while revenue rose 53%. Although we expect lower growth in the remaining quarters, the pace is currently higher than market forecasts for 2023 (expected profit and revenue growth of 28% and 32%). The company’s valuation took a significant hit in connection with Russia’s invasion of Ukraine. However, the current valuation of 9x 2023 forecasted earnings is not very demanding.

On the news side, it was a relatively quiet month where a certain calm settled in as investors continue to get used to continued high inflation and interest rates, something that drives local capital to the fixed-income market instead of the equity market. We are however gradually approaching the time for improvements at the macro level and better visibility ahead and earnings have held up well, even when converted to USD. Of our markets, Pakistan remains at the center of attention currently. At the same time as the discussions with the IMF continue, the government and the opposition have now sat down at the negotiating table to arrive at a date for the election. As previously stated, we believe it is necessary that the timing be determined so that the market can start looking ahead again.

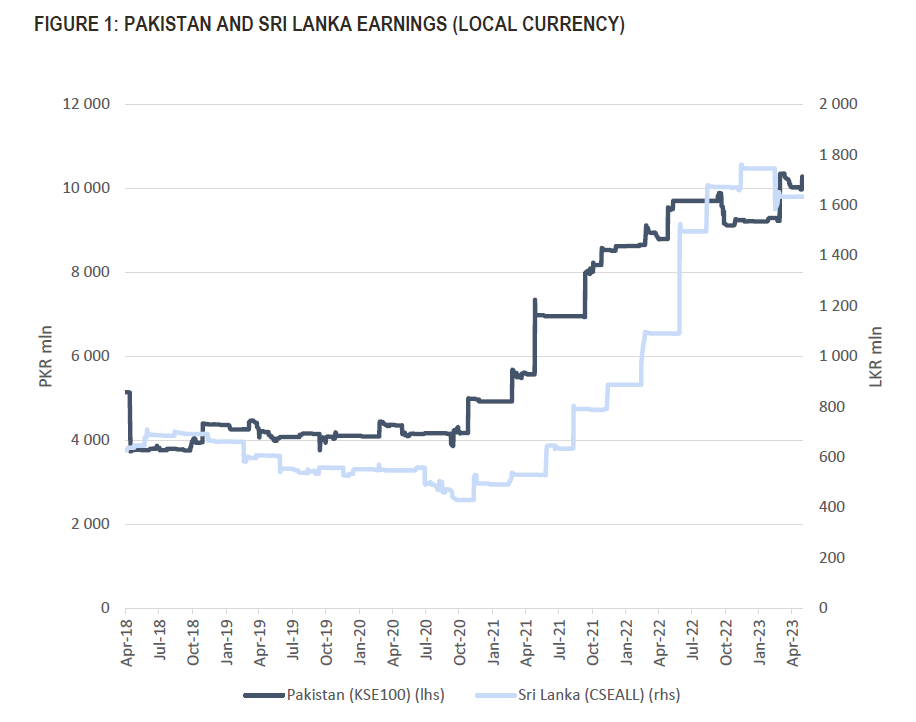

Sri Lanka and Pakistan have been the two most severely affected markets in the past year. As an investor, however, one must distinguish between a country’s problems and its impact on the profit development of the listed companies. We note that corporate profits in Sri Lanka and Pakistan have so far held up well, where the companies have generally succeeded in compensating for devaluations and higher costs (Figure 1).

It may seem strange that companies can continue to grow despite quite terrible headlines, but it is quite logical. Equities are real assets (e.g., machinery and land) whose value is relatively constant regardless of the currency you choose to measure them in. The owners of these assets require a certain level of return on the real value. Assuming they supply a good or service that fills a societal demand, they are thus able to raise prices and their profit in local currency in times of devaluation just to maintain a certain required rate of return. Exchange rate movements are perhaps the most mentioned point of concern among foreign investors but have limited empirical support based on the impact on profits in 1-2 years perspective. Even less so if the portfolio is positioned in companies that tend to weather these periods better than average. The damage that occurs is instead that the fear of the unknown lowers the valuation multiples in exposed markets until the crisis is perceived to be over. This phenomenon, rather than the fundamental impact, is what creates most of the swings we see in our equity markets, and it creates good buying opportunities for long-term investors. As Warren Buffett once said: “The stock market is a device for transferring money from the impatient to the patient”.

___________________________________

TUNDRA SUSTAINABLE FRONTIER FUND REPLACES THE SWAN WITH THE EU’S REGULATIONS FOR SUSTAINABILITY

In connection with the new EU regulation under the Sustainable Finance Disclosure Regulation (SFDR), new requirements are applied to funds’ sustainability work as of March 2021. Tundra has therefore decided on July 4 not to continue with the Nordic Ecolabelling of the fund. According to the new regulations, sustainability reporting must take place in a uniform manner and funds are divided into different categories. The Tundra Sustainable Frontier Fund is classified as an Article 8 fund (Light green: promotes environmental or social characteristics). The investment philosophy of the fund remains the same; management of the fund and is not affected by the change.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.