THE FUND:

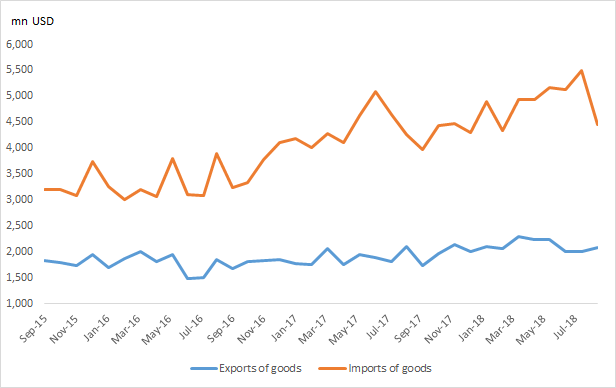

Pakistan’s government needs to do more to reduce imports and increase exports from current levels. Source: State Bank of Pakistan, Tundra Fonder.

During September, the Fund went down by 6.1% as compared to the benchmark’s MSCI Pakistan Net (SEK)’s return of -2.9%. Pakistan’s broader KSE 100 Index slipped downwards by 1.8% while waiting for clarity over the government’s plan to bridge the external financing requirement. Investors continued to speculate about the direction the economic team intends to take before the final announcement in mid-October 2018.

In the outgoing month, the fund reduced its exposure in Attock Petroleum, an Oil and Marketing company, primarily due to a dwindling product mix (furnace oil) and a contraction in the demand for other products such as motor spirit and high speed diesel. The increase in international oil prices coupled with falling PKR, has impacted the inelastic demand for oil. Furthermore, with the government envisioning more efficient RLNG and coal power plants, the a future demand for furnace oil will, in all likelihood, decline. The new power plants have dented earnings growth of several oil and marketing companies prompting us to stay on the sidelines.

THE MARKET:

When the new government took charge, the Current Account Deficit (CAD) clocked in at 5.8% of GDP and FX reserves were at 7 weeks’ worth of imports and declining fast. While economists and investors hypothesized about the government’s next steps, former CEO-turned-Finance Minister, Asad Umar bought time for further deliberations by assuring audiences that “all options, including IMF, are open.” He intends to unveil his recommendations for bridging the external financing gap in mid-October. He will have to make good on his assurances as the market is running low on patience.

As we write this update, the Finance Minister’s ‘mini-budget’ intended to rein in the burgeoning CAD and ensure fiscal discipline, is heading for parliamentary approval. It includes necessary fiscal adjustments in the form of an upward revision in income tax rates and gas prices, cuts to development expenditure, imposition of additional duties on luxury imported items and a hike in levies on cigarette manufacturers all designed to limit the fiscal deficit to 5.1% in FY2019. We think this is a realistic target. By clearing establishing its priorities, the government is set to protect two important stakeholders: the lower middle class and exporters. That said, investors were more curious about the external financing options.

There has been a flurry of developments recently including one highly probable scenario of purchasing oil on deferred payments from Saudi Arab (worth $6bn); and, a somewhat unlikely one of, inviting Saudi Arabia and UAE to invest in the China Pakistan Economic Corridor (CPEC). Both these options may help improve FX reserves. More interesting is the Prime Minister’s visit to China. The Chinese have agreed to bridge the trade deficit with Pakistan worth 3% of GDP and offer bilateral loans to bridge the external gap in the medium term. The IMF team is also in Islamabad at present and it is rumoured that they propose to renegotiate tariffs on power plants and further depreciate the currency by 10%-15%. The Finance Minister has reiterated the need to “get house in order be IMF or no IMF” and will outline his roadmap in two weeks’ time, after the PM’s China visit. And finally, a high-powered delegation from Saudi Arabia is in Pakistan for investment purposes.

Surprisingly, the Current Account Deficit for August 2018 was encouraging at USD 600m (annualised 2.3% of GDP). Helped by currency depreciation of ~18%, monetary tightening from 5.75% to 8.5% (including 100bps last week) and, deferring oil payments, it has already started showing signs of improvement. If this can be sustained over the next 2 to 3 months investors are likely to return anticipating improving prospects on the next leg of a bullish run. Although global Brent Oil prices have touched $85/barrel, the government is mulling over ways to avoid an emerging inflation spiral that may lead to higher borrowing costs and/or unwarranted rate of monetary tightening. If President Trump succeeds in pressuring OPEC to reduce oil prices by the US mid-term elections, Pakistan’s economic managers will be delighted. For the moment, a forward P/E of 7.7x, the index is trading back at very attractive long-term valuations and awaiting policy triggers. Imran Khan’s new government has set high expectations on structural reforms that we are assessing. If even half of these reforms materialize we will see a massive turnaround in the market’s sustainability. Meanwhile, we wait for the Finance Minister complete his visit to China and return with a concrete road-map for investment managers.

DISCLAIMER:

Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.

Kundgrupp / Investortype:

* Ontario and Quebec