THE FUND

The Fund rose 2.5% in November, better than the benchmark index MSCI EFM Africa ex South Africa Net Total Return Index, which rose 0.3%. So far this year the Fund has risen by 7.0%, underperforming the benchmark index, which has risen 18.8%. At a country level, overweigths in Nigeria (33% of fund assets) and stock picks in Kenya (5%) contributed most positively relative the benchmark. The Fund’s underweights in Morocco (0% of fund assets) and overweigths in Egypt (49%) contributed most negatively. At the sector level, overweigths in Financials along with underweights in Communication Services contributed most positively, while the overweigths in Consumer Discretionary and underweights in Consumer Staples contributed most negatively relative the benchmark index. The Swedish krona strengthened 1% versus the USD in November, decreasing the SEK return of the Fund. (all changes in SEK).

Most of the companies in the Fund have now released results for the third quarter and on an aggregated level sales and profits grew by approx. 15% in USD vs the same period last year. This looks much stronger than developed markets where sales are unchanged and profits fell around 10%. Valuations remain attractive at 6.5x estimated earnings for current year, 1.1x book value and an estimated dividend yield of 6.3%.

MARKET

In November, the African markets (MSCI EFM Africa xSA Net TR +0.3%) outperformed other Frontier markets (MSCI FMxGCC Net TR), which fell 1.4% during the month. Nigeria was the best African market rising 2.5% followed by Zimbabwe, which rose 2.3%. Zambia was the worst African market declining 11.3% as the Kwatcha depreciated 10% vs USD, while Egypt was the second-worst performer, falling 5%. (all changes in SEK).

The Egyptian market (Hermes Index -5% in November) failed to excite investors. The central bank cut rates as expected by 100 bps to 12.25% (only 0.5%-points above the level pre-devaluation in November 2016) as inflation noted a new low at 3.1% in October thanks to stable food prices and base effects. This is likely the bottom and inflation will move upwards from here.

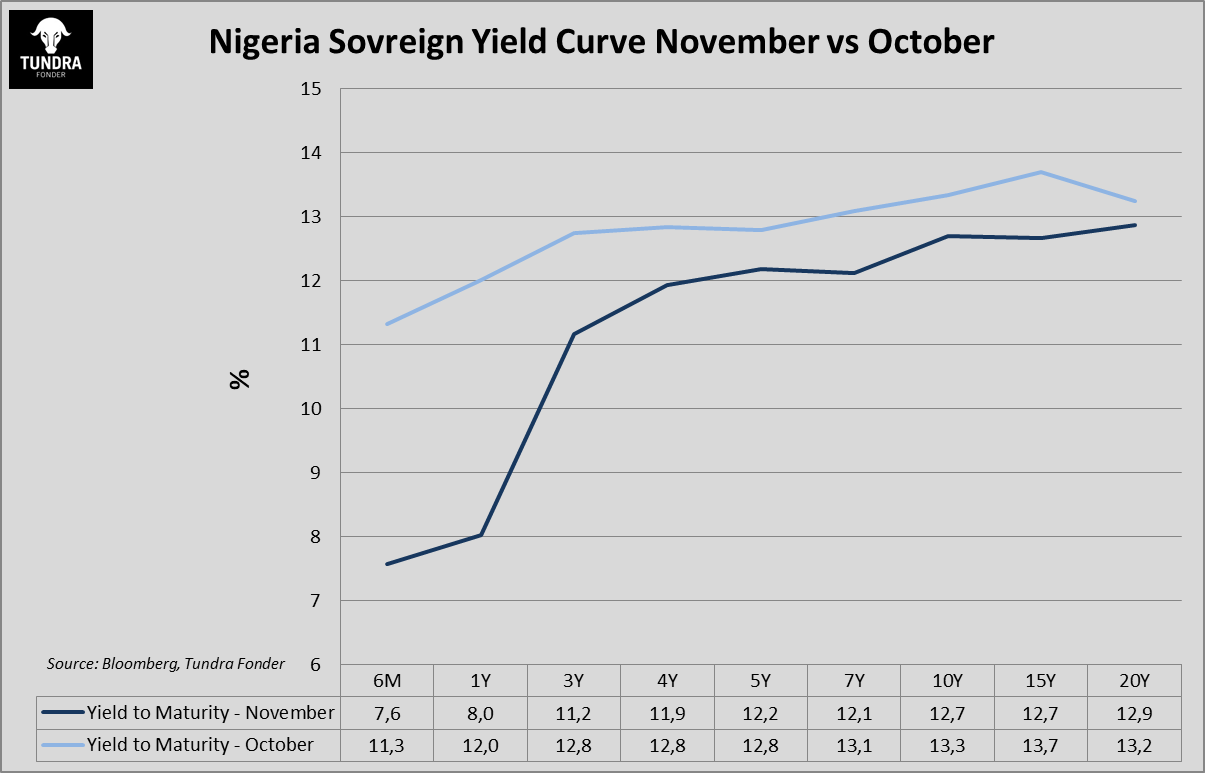

The Nigerian stock market (Nigeria Stock Exchange Main Index +2.5%), led by the banks, rallied at the beginning of the month, fueled by speculations on massive money flows hitting the stock market after being banned from the local Open Market Operations auctions. Originally designed to mop up extra liquidity from the financial sector, it also became a hot investment alternative offering higher yields versus T-bills. Only local and foreign banks are now allowed to participate in the auctions. The stock market reacted very positively as most of the banks are trading at 10-year lows on P/E and P/B and offer attractive dividend yields, but the local bonds reacted even more. 3-month T-bills yielded around 11.1% in October, now trades at around 6.5%, 1 year T-bills now offer 8.4% versus above 13% in October. Worth noting is that with inflation recorded at 11.6% in October, due to the border closure to Benin to stop illegal smuggling of foodstuff, most of the bonds are now trading at negative real returns.

In Kenya (Nairobi All Share Index -1.1%) the market is trying to adjust to a reality without rate caps, and the financial sector continued to rise while index heavyweight Safaricom retreated slightly. Equity Bank´s performance was also aided by announcing a purchase of 66.5% of Banque Commerciale du Congo to be merged with their local subsidiary in DRC. The central bank cut interest rates by 0.50 %-points.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.