THE FUND

The Fund fell 4% in May, worse than the benchmark index MSCI EFM Africa ex South Africa Net Total Return Index, which fell 2.3%. So far this year, the Fund has risen by 8.6%, slightly worse than the benchmark index, which has risen 12%.

At country level, the underweight in Kenya (0% of fund assets) and the overweight in Ghana (4%) contributed most positively relative to the benchmark. The Fund’s overweight in Nigeria (33% of fund assets) and South Africa (4%) contributed most negatively. At the sector level, the underweight in Communication Services and stock selection in Health Care contributed most positively, while share prices in Financials (mainly Nigerian UBA and Access Bank who performed poorly) and the overweight in Consumer Discretionary contributed most negatively relative to the index. The Swedish krona strengthened by 0.5% against USD, which had a negative effect on the return converted to SEK.

Our partial sale of the holding in South African Massmart last month proved, in the short term, to be well timed as the share became the portfolio’s worst holding in May with a decline of 30%. During May, we have reallocated parts of the exposures to our banks. On the one hand, we have decreased in Egyptian Credit Agricole and instead increased in Commercial International Bank (CIB), as the valuation discount in the former to the latter has sharply decreased. In the long term, we see that Credit Agricole deserves to be valued on par with CIB, but taking into account the poorer liquidity of the share, we don’t expect that to happen in the near future. Now the share has performed relatively well, while we were able to invest in CIB’s London-listed GDR at a 5% discount. We have also looked more closely at our Nigerian banks, which led to a reduced position in UBA and FBN and an increase in our position in Access Bank.

Although the market climate is anything but favorable at the moment with declining risk appetite globally, we see that our holdings continue to deliver substantial growth in the first quarter of 2019. Many of the portfolio companies have now reported the result for the first quarter and adjusted for outliers, sales increased on average by 10% and profits by over 30% compared to the last quarter, well above the 15% that the market expects for our holdings for the full year. The valuations have come down further from last month and the portfolio is now valued at around 6x expected profits for 2019, while the yield is expected to be around 7%. Timing the market is notoriously difficult, but we can conclude that today’s valuation is clearly lower than the historical average, which in itself should limit the downside, while the potential upside in a few years’ time looks attractive (all changes in SEK).

MARKET

The African markets (MSCI EFM Africa xSA Net TR (SEK) -2.3%) performed worse than other Frontier markets (MSCI FMxGCC Net TR (SEK)), which rose 2% in May. Zimbabwe was the best African market rising 40.9%, followed by Nigeria, which rose 7.5%. Last month’s winner South Africa became the worst African market, with a decline of 7%, while Egypt was the second-worst performer falling 5.6%. The remarkable upturn in Zimbabwe remains due to the “wrong” reasons, i.e. it is driven by investors seeking protection against rising inflation, and although the new currency policy, in theory, can solve some outstanding issues, the new currency is overvalued despite a depreciation of more than 60% in May. It is still difficult to transfer money out of the country, which means that “paper profits” run a high risk of turning into nothing (all changes in SEK).

The Egyptian market (Hermes Index -5.6% in May) was apathetic in the absence of either positive and/or negative news. The central bank kept the policy rate unchanged, in line with market expectations. Electricity prices will be raised by an average of 15% from 1 July, also in line with expectations.

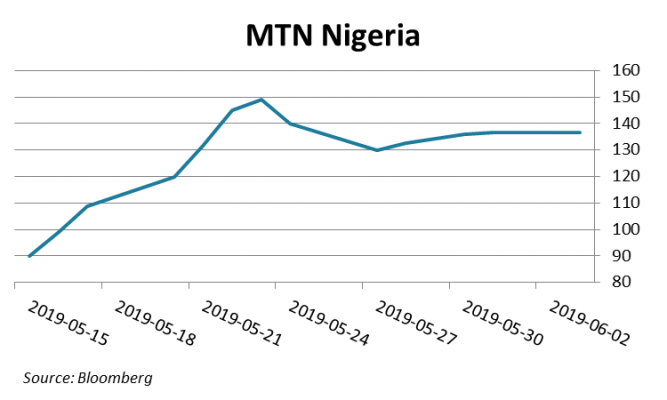

Nigeria (Nigeria Stock Exchange Main Index +7.5%) didn’t do much better, but the index still ended the month as one of the best in Africa after the long-awaited listing of MTN Nigeria that was conducted in the middle of the month. The listing was made “by introduction”, i.e. without issuing new shares (just as Spotify did at its listing in New York last year) at NGN 90 per share, which was the average price for transactions made in the last six months. The interest was huge and the sellers few, which led to the share trading limit up (10%/day) in the first five trading days. The company is now valued at USD 7.7 bn, which can be compared with the Nigerian stock exchange’s largest company Dangote Cement, which is valued at USD SEK 9.5 bn and the second largest company Nestlé Nigeria’s USD 3.2 bn. MTN Nigeria is 80% controlled by MTN Group (listed in South Africa) who said that they will sell shares at a later date after the ongoing tax dispute concerning USD 2 bn has been settled.

In Kenya (Nairobi All Share Index -4.2%), the stock market’s giant, telecom operator Safaricom, released the result for the fiscal year ending March. Earnings per share increased by 15%, which was slightly worse than the market expected and the share traded down. Equity Bank’s purchase of part of Atlas Mara’s African banks in April was also not noticeably rewarded and the stock ended the month 5% lower than the month before.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.