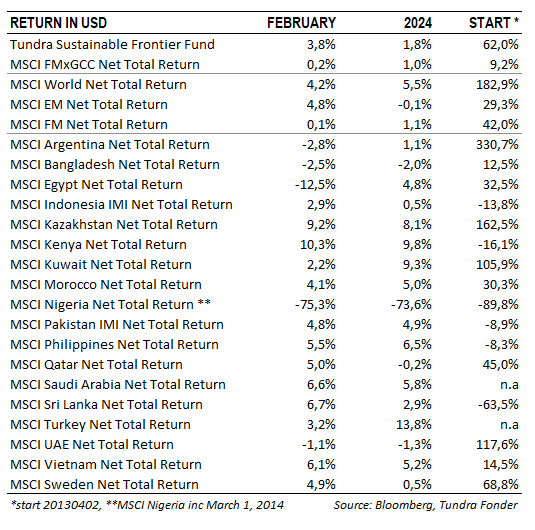

VIETNAM AND PAKISTAN DROVE RETURNS IN FEBRUARY

In USD, the fund rose 4.6% (EUR: +5.4%) during February compared to MSCI FMxGCC Net TR (USD), which rose 0.8% (EUR: +1.5%), and MSCI EM Net TR (USD), which rose 5.2% (EUR: 6.0%). During the month, we received primarily positive contributions from our holdings in Vietnam and Pakistan (together 44% of the fund’s total exposure at the end of the month). Both our Vietnamese sub-portfolio and our Pakistani sub-portfolio rose 9% during the month. Our largest holding (9% of the fund), Vietnamese IT company FPT Corp, performed strongly, rising 13%. In Pakistan, the gain was led by our second largest position in the country, Meezan Bank, which rose 17% during the month. Pakistan’s equity market heaved a sigh of relief after the government outcome looked to be as expected with a PML-N led government. Minor negative contributions were received from Nigeria (-50 bps) where two of our smaller Nigerian positions, Access Holdings and Stanbic, fell despite a further 10% weakening of the currency.

IMPRESSIONS FROM OUR TRIP TO VIETNAM

Tundra’s Chief Investment Officer, Mattias Martinsson, is traveling in Asia during the first half of the year. This is to enable more efficient traveling during a very hectic first half of the year. During the last week of February, we stopped by Vietnam, where we participated in the biggest investor conference of the year. We met our portfolio companies, other leading players, and some colleagues in the industry. It was 6 months since our last visit, which took place during a period of relatively greater uncertainty. Several of the conclusions still apply. For example. the greater impact of the global interest rate climate on Vietnam, given its higher integration into the world economy and higher penetration of consumer credit and housing loans, as well as the concern many investors feel about the problems in Vietnam’s largest company, Vingroup. Read more about the background here. A difference now, compared to 6 months ago, is that the banks give the impression of having a better overview of their exposure towards the real estate sector. The tone from the companies in the consumer sector is somewhat more positive, even if the hopes for a recovery in private consumption from the second half of 2024 indicate that the current demand situation remains under pressure. Three of our six portfolio companies were represented at the conference and they all did well.

EGYPT ON ITS WAY OUT OF THE CRISIS

Last month, it was Nigeria that took steps to solve the problem of insufficient access to foreign exchange. We talked about the specific problem several of our countries have found themselves in recent years, where they ended up with a cash flow problem for payments in foreign currency. The only remaining country in our group of low-income and lower-middle-class countries that needs to loosen its “knot” is now Egypt, and during the month it announced a comprehensive restructuring plan. In an agreement with the United Arab Emirates, Egypt will receive investment of USD 35 billion (including USD 24 fresh capital injection) as the Abu Dhabi Developments Holding Company acquires the right to develop parts of the Ras El Hekma area, situated in the north with a coastline to the Mediterranean Sea. The amount can be compared against the market estimates of approximately USD 15 billion required to clear the queues of repatriations in the country that have built up in recent years. Total estimated investments (over decades should be added) have been stated at about USD 150 billion, and Egypt will have a profit share of 35% of future profits. There is a clear logic behind the agreement. The Gulf countries, including the United Arab Emirates, have an abundance of capital, but limited land area. Egypt has a long coastline along the Mediterranean Sea, which today is yet to be properly developed. The cultural similarities between the countries likely help as well. Based on the agreement, Egypt will probably also conclude a new agreement with the IMF. At some point, probably in the next month, we will see a devaluation of the Egyptian currency, but given the good preparations, this can take place in a controlled manner and is likely to be followed by considerable optimism for the future. It is however important that Egypt, just like other crisis-ridden lower-middle-income countries utilize this chance of a fresh start, and take the necessary steps to ensure a more stable path forward.

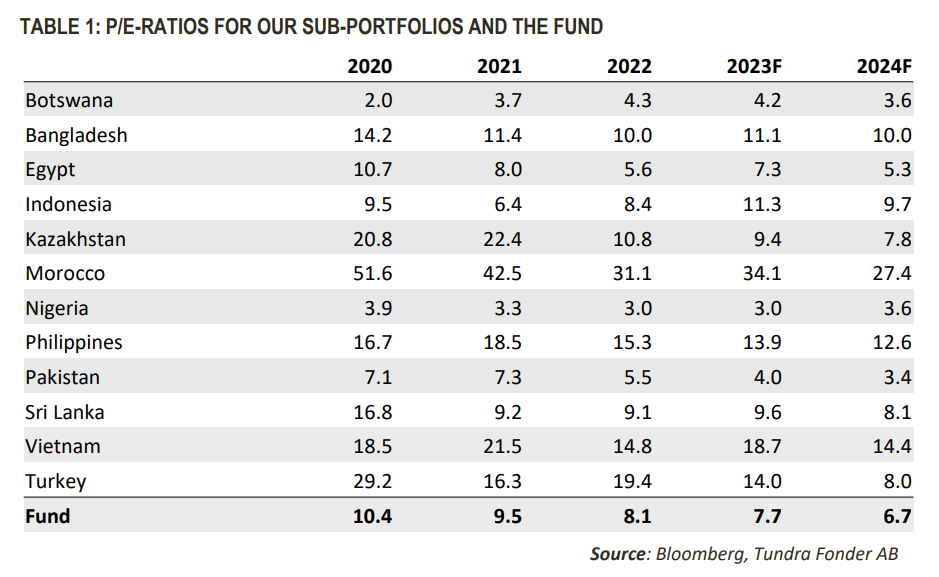

Egypt is the last of our markets that now seems to have found a workable way forward. Provided this is confirmed, we believe investors will be able to focus more on the performance of the individual companies. The fund is currently valued at a P/E of 7.7x on 2023 earnings, a valuation that is expected to fall to 6.7x on 2024 expected earnings. The exact same portfolio was valued at the end of 2020 at 10.4x and at the end of 2021 at 9.5x, which gives us reason to state that the portfolio seems cautiously valued in the face of a market climate that is likely to be more positive from here.

___________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.