MACRO WORRIES OVERSHADOW STRONG RESULTS

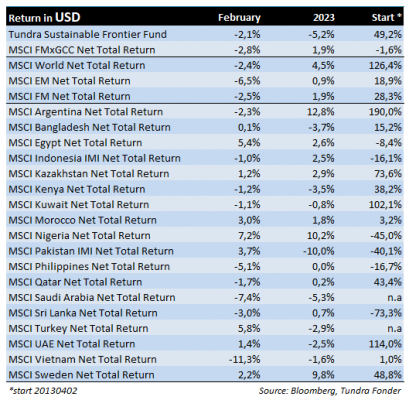

In USD the fund fell 2.1% (EUR: -0.1%), better than the fund’s benchmark MSCI FMxGCC Net TR (USD) which fell 2.8% (EUR: -0.8%), and MSCI EM Net TR (USD) which fell 6.5% (EUR: -4.6%).

On a country level, our main positive contributors relative to the benchmark were Vietnam, Pakistan, and Sri Lanka, while the main negative relative contribution came from Indonesia and the Philippines. Among our holdings, we gained most from Pakistani IT company Systems Ltd and Egyptian auto manufacturer/financial service company GB Auto. The worst contributors were Vietnamese REE Corp and FTP Corp.

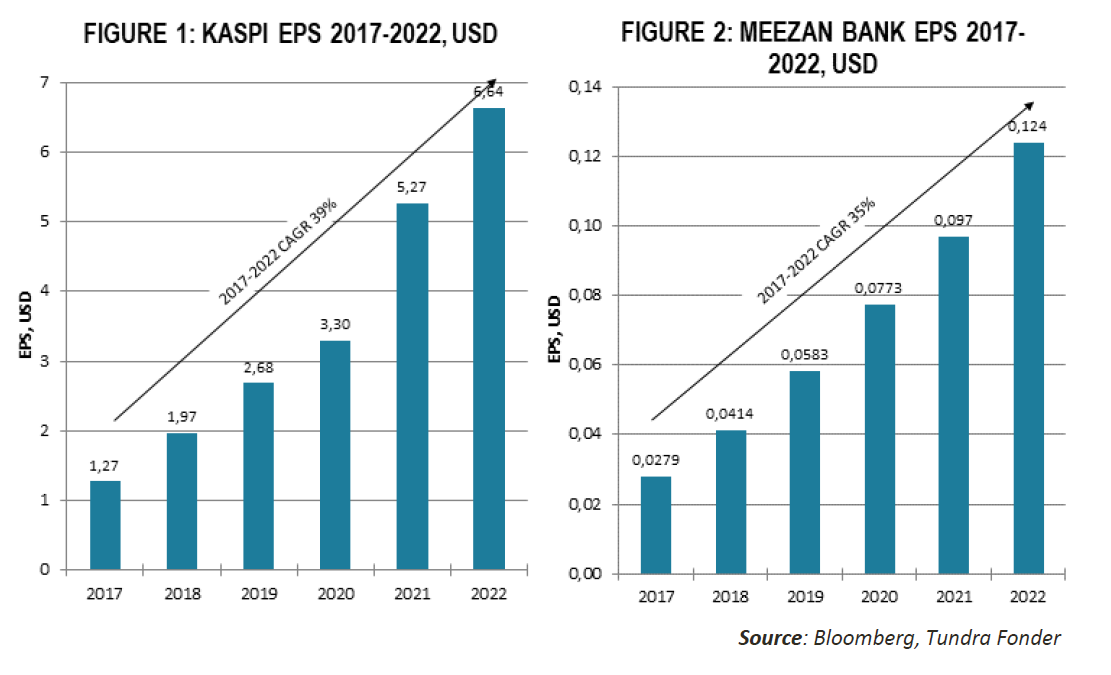

A few more of our holdings released results, showing strong growth. Our Kazakhstani fintech Kaspi beat forecasts and delivered 38% EPS growth for the full year, finishing the year with a very strong fourth quarter with increasing volumes in all three business areas (fintech, payments, and marketplace). Our Pakistani Islamic bank Meezan also produced record earnings with 4Q EPS growth of 93% YoY on the back of higher Net Interest Margins (the difference between lending and deposit rates), while the calendar Year EPS grew by 59%. National Bank of Pakistan also recorded very strong growth with EPS increasing 185% in the fourth quarter, but mainly due to base effects with a one-off charge booked in Q4 2021. Calendar year earnings grew more moderately, but still a good 8%. Both banks benefit from the higher interest environment in Pakistan as well as the weaker currency. Sri Lankan Sampath Bank released surprisingly strong numbers as well, also on the back of higher NIMs. Higher provisions, however, muted full-year earnings growing by 1.5%.

The Sri Lankan equity market continued to rise on positive progress in the bilateral/IMF discussions on debt restructuring. After the staff-level agreement with IMF in September last year, discussions with India and Paris Club, only China remains. China looks to be willing to come to an agreement, but the final details are still being negotiated to align with IMF conditions.

IMF discussions with Pakistan are also progressing, although at a slower pace than the market initially anticipated, adding some uncertainties to the market conditions. The central bank surprised with a 300 bps rate hike on March 2nd to counter the higher-than-expected inflation of 31,55% in February. The currency still lost approx. 6% on the news (but has since regained part of the fall) after strengthening for most of February. The rate hike and devaluation are likely to please the IMF, as are the in January and February hiked gas and petrol prices, along with increased taxation to raise government revenue and decrease the budget deficit. The political situation remains uncertain with the opposition trying to force new elections, while the incumbent government is trying to delay the election as it would be disastrous for them given the latest opinion polls.

The very uncertain Nigerian presidential elections concluded Bola Tinubu from the ruling APC party as the winner with 36.6% of the votes and main opposition PDP candidate Abubakar getting 29.1%, and newcomer Obi from the Labour Party getting an impressive 25%. Voter turnout was however a big disappointment with only 27% of registered voters turning up to vote, compared to 35% in the 2019 elections. Tinubu is due to be inaugurated at the end of May, and markets will closely watch every decision to make sure the more market-friendly and necessary reforms are delivered upon.

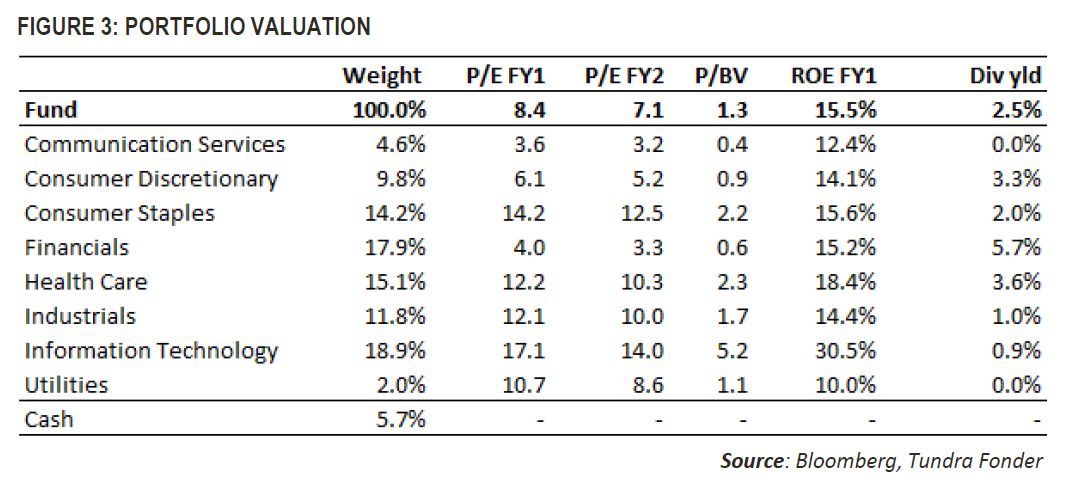

Although the final phase of a crisis often presents great investment opportunities, it is also difficult, and there is always the risk that what looks incredibly cheap will become even cheaper. Several of our markets are in the eye of the storm where worst-case outcomes are fairly well illuminated. This suggests that it will be difficult to surprise negatively from here, even if we are still missing some pieces of the puzzle to be able to see ahead. 24 of our 39 portfolio companies (58% of portfolio assets) have now released their reports for the fourth quarter. The average profit growth (expressed as median) is 10% for the full year. Among our 20 largest holdings, 13 have reported. 10 shows positive profit growth (median 25%). 2022 was a very difficult year for the majority of our markets, but we note that the vast majority of our portfolio companies continue to grow. The average valuation in the fund for the current year (fiscal year 2023 for the companies that reported for 2022 and 2022 for others) is P/E 8.4x, with expected earnings growth of 16% for the year that follows. The average P/BV valuation is 1.3x with a 16% average return on equity and a dividend yield of 2.5%. In the long term, stock prices are driven by underlying earnings growth, but the big swings in between come from changes in what is commonly called sentiment (when the investor collective oscillates between fear and greed). If we exclude the risks of new global events, it is difficult to see investors in our markets becoming more fearful than they currently are. Although there are plenty of concerns remaining in the short term, and a multi-year investment horizon is required, this suggests that investors should continue to gradually increase their allocation to our part of the world.

______________________________________________________________________

TUNDRA SUSTAINABLE FRONTIER FUND REPLACES THE SWAN WITH THE EU’S REGULATIONS FOR SUSTAINABILITY

In connection with the new EU regulation under the Sustainable Finance Disclosure Regulation (SFDR), new requirements are applied to funds’ sustainability work as of March 2021. Tundra has therefore decided on July 4 not to continue with the Nordic Ecolabelling of the fund. According to the new regulations, sustainability reporting must take place in a uniform manner and funds are divided into different categories. The Tundra Sustainable Frontier Fund is classified as an Article 8 fund (Light green: promotes environmental or social characteristics). The investment philosophy of the fund remains the same; management of the fund and is not affected by the change.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.