THE FUND

The fund rose 1.6% in August, worse than the benchmark index MSCI EFM Africa ex South Africa Net Total Return Index, which rose 4.6%. So far this year, the fund has risen by 6.2%, also behind the benchmark index, which has risen 18%.

At country level, the overweights in Egypt (54% of fund assets) and underweights in Senegal (0%) contributed most positively relative the benchmark. The fund’s underweight in Morocco (0% of fund assets) and overweight in South Africa (2%) contributed most negatively. At the sector level, overweights and stock selection in Consumer Discretionary along with underweight in Material contributed most positively, while the stock selection in Financials and underweights in Communication Services contributed most negatively relative the index. The structural underweight in Commercial International Bank (the bank benchmark weight is almost 20%, while the fund rules cap any company exposure to 10%) cost approx. 1.5% relative to the benchmark after a strong performance in August.

The Swedish krona weakened by 2.5% against the USD, which had a positive effect on the return converted to SEK.

In August, we sold our position in retailer Massmart (South Africa) and decreased our position in Letshego (Financial company based in Botswana) after disappointing results and revised outlook in the near to medium term. (all changes in SEK).

MARKET

The African markets (MSCI EFM Africa xSA Net TR +4.6%) performed better than other Frontier markets (MSCI FMxGCC Net TR), which rose 1.5% in August. Egypt was the best African market rising by 10.4%, followed by Tunisia, which rose 3.4%. Zimbabwe was, again, the worst African market declining 9.2%, while Namibia was the second-worst performer, falling 8.6%. (all changes in SEK).

The Egyptian market (Hermes Index + 10.4% in August) regained momentum after the July inflation figures came in lower than expected (+ 8.7%) and lower than the previous month (+ 9.4%), which increased the hope of an interest rate cut at the central bank’s scheduled meeting at the end of the month. That hope became true when the central bank lowered interest rates by 1.5 percentage points on August 22, more than expected, and the market saw renewed interest. The interest rate cuts are important for the next leg of Egyptian economic growth after the devaluation in 2016. There is a pent-up investment need that is expected to materialize when interest rates fall another 2-3 percentage points. Those investments will lead to increased labor demand and increased consumption, but also increased lending from the banks. The market expects a further 3 percentage points cut in the coming 18 months, of which 1 percentage point is expected before the end of the year.

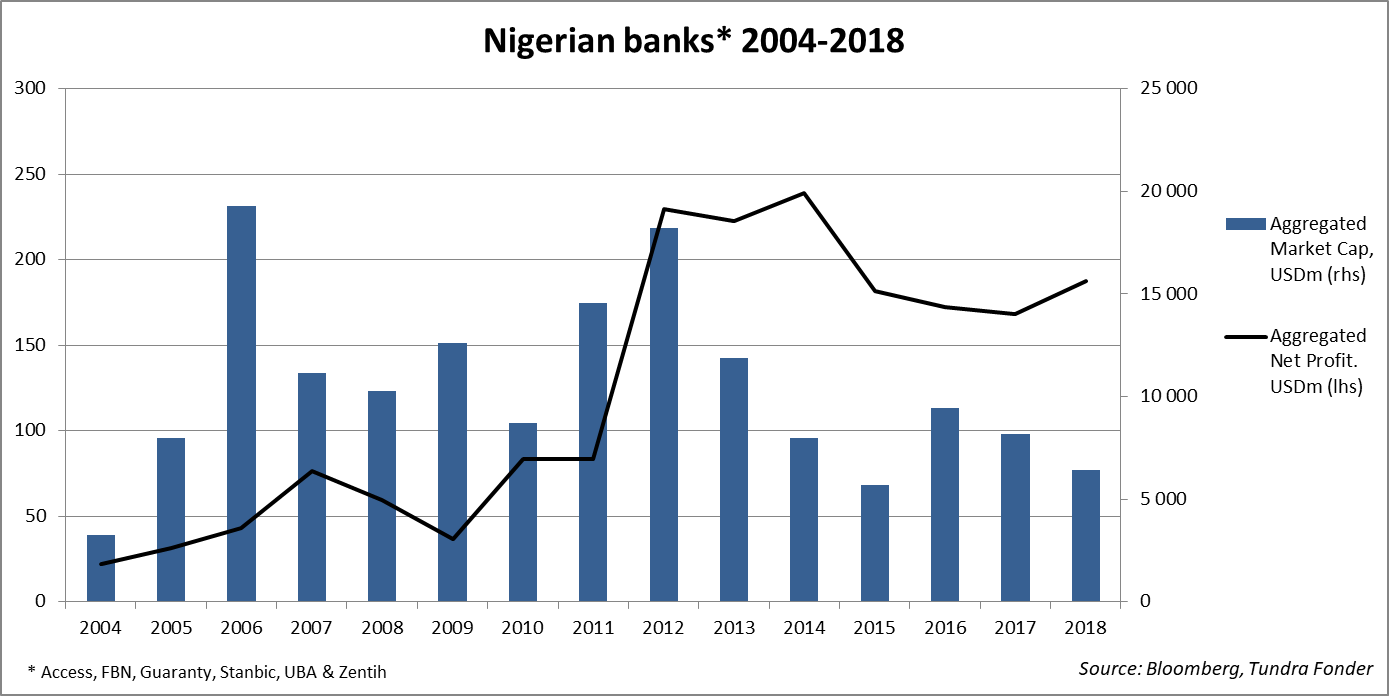

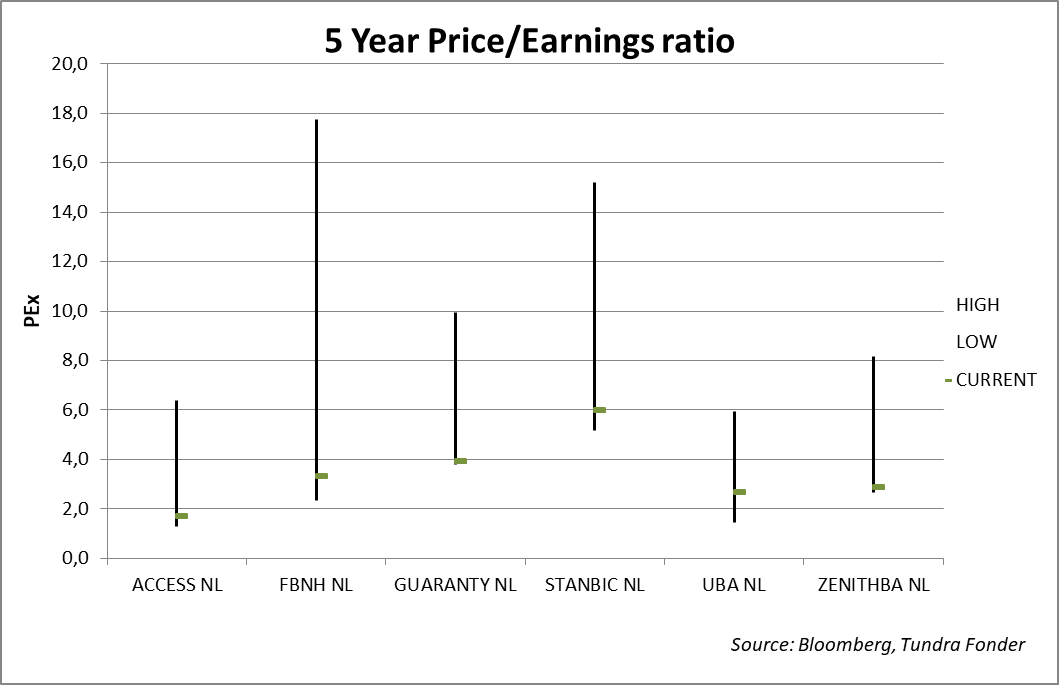

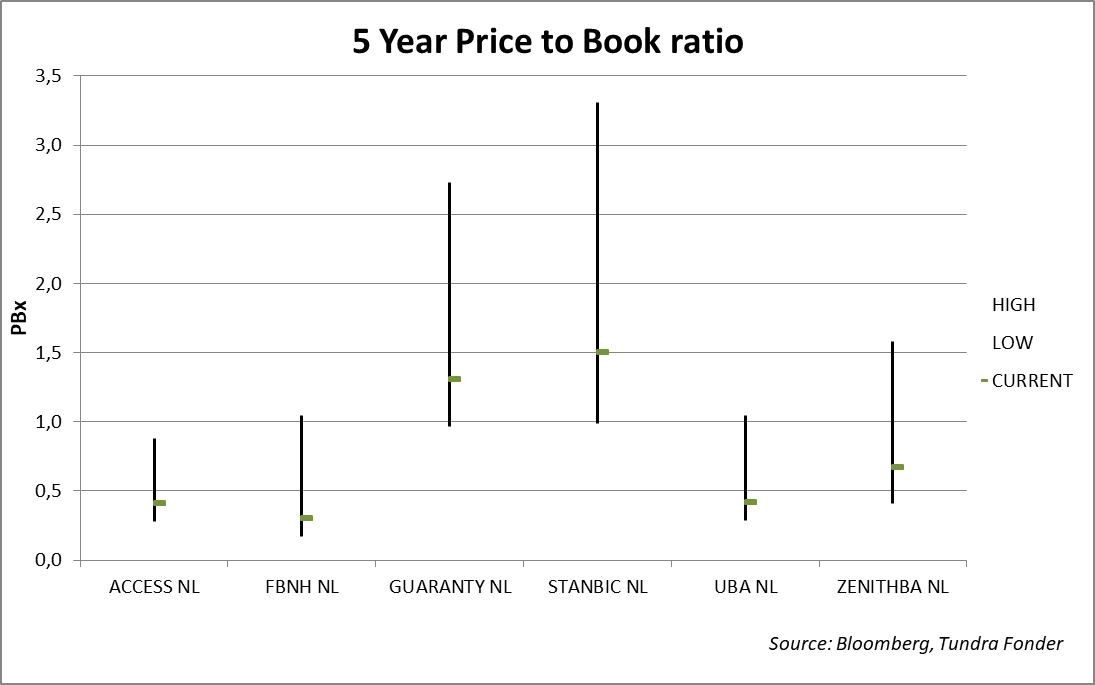

The fund’s second major country exposure in Nigeria (Nigeria Stock Exchange Main Index + 2%) is still facing headwinds. GDP for the second quarter of this year rose by just below 2%, slightly worse than expected. The lack of reforms makes it difficult for the economy to regain momentum. Without e.g. reliable electricity supply and better-developed infrastructure, it’s difficult to attract industrial companies. A recent example is that Toyota has just decided to place an assembly plant in Ghana instead of Nigeria, despite Nigeria’s population being 200m against Ghana’s 30m. The investment need in Nigeria’s’ infrastructure is not new, and companies are naturally used to operating in those circumstances, but in the longer term creating a stronger, more diversified economy requires investments. Naturally, companies that are not as dependent on physical infrastructure are doing better. In the fund, we have more than 30% of the assets invested in Nigeria, all in the financial sector, partly for the reasons stated above. Over the past 15 years, the six Nigerian banks we hold have increased their assets by almost 30% per year (43.6% per annum for the best bank and 21% per annum for the worst). Profitability (measured as net profit/assets) has averaged 2.4% (3.6% for the best bank and 1.5% for the worst). Despite several major crises over the past 15 years, profits have grown by over 25% annually in local currency. We have seen several major devaluations during the same period, but despite this, the profits for these six banks have grown from a total of USD 200m in 2004 to USD 1855m in 2018. This represents an average growth of 17%, although growth has been slower in recent years. Since 2012, profits have decreased by 18% (in USD), but at the same time, the market-value has decreased by 65% (in USD). Currently, our six banks are trading at 3.5x the estimated profit for the current year, 0.8x book value and a dividend yield of 10%. The valuations indicate that the market attributes almost no growth going forward, even though we know that the bank penetration in Nigeria is still very low and that most companies are still basically excluded from the loan market. The banks have traditionally grown by opening new offices. It has been a complicated and expensive process. There is now a strong focus on growing through electronic platforms and this has also made retail customers an attractive target group for cheaper borrowing and other revenues such as credit cards. For example, Zenith Bank attracted 800,000 new customers during the first half of 2019 and issued 1.2m new credit cards. If they continue to add at the same rate in the second half, they will have doubled the number of customers to 10 million vs 5 million two years ago. The retail customer segment will generate a significant portion of future revenues and further diversify banks’ revenues. We find it difficult to see the sector as anything but very attractive, despite the challenges that exist.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.