THE FUND

The Fund fell -0.8% in May, worse than the benchmark index MSCI EFM Africa ex South Africa Net Total Return Index, which rose 0,1%. So far this year, the Fund has fallen by 19,1%, in line with the benchmark index, which has fallen 19,0%. At a country level, underweights in Kenya (3% of fund assets) and overweights in Nigeria (22%) contributed most positively relative to the benchmark. The Fund’s overweights in Egypt (41% of fund assets) and overweights in Ghana (10%) contributed most negatively. At the sector level, overweights and stock picks in Financials along with overweights in Health Care contributed most positively, while the underweights in Materials and overweights in Consumer Discretionary contributed most negatively relative to the benchmark index. The Swedish krona strengthened 3.6% versus the USD in May, decreasing the SEK return of the Fund (all changes in SEK).

A mixed bag of results continued to come from our holdings as well as the rest of the markets, mostly to be ignored by the market as investors are more focused on trying to figure out how bad Q2 will be and how much (if any) of a recovery we will see in Q3 and onwards. Two of our larger holdings sold off on the back of disappointing results, Egyptian power conglomerate El Sewedy as well as Credit Agricole Egypt (-18% and -13% respectively). Better than expected numbers from another top 10 holding, Egyptian Cleopatra Hospitals, on the other hand saw very little impact from COVID-19 and the stock rose 15% in May.

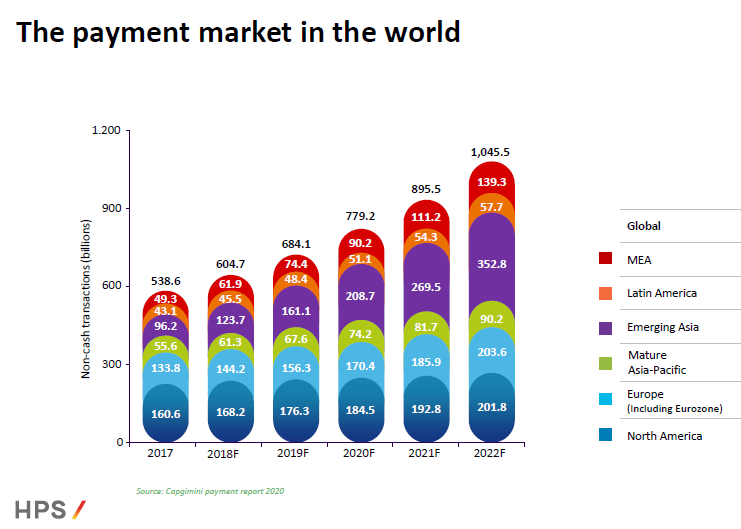

The Fund made a new investment in Morocco as we invested approx. 3% in Hightech Payment Systems (HPS). HPS is one of the world’s leading electronic payment value chain suppliers, offering a suite of solutions e.g. mobile wallets, fraud detection, and e-commerce support. The company is active in over 90 countries and has more than 400 clients (including several top 100 financial institutions). We have followed the company for some time and had a meeting with the management in January. We have been impressed by the growth they have delivered (sales FY14-19 CAGR +25%, Net profit FY14-19CAGR +31%) as well as the prospects ahead. The industry growth is expected to be above 15% in the coming years and even higher growth is expected in Asia and Africa where HPS has more than 65% of their revenue. While PowerCard (the product suite name) or HPS is not recognized by end consumers, HPS has a strong reputation in the payment industry offering smarter and better integration with already existing systems, or by replacing them in full. As an example, one of their projects with Amex resulted in reducing the number of systems from 16 to 1 to handle all international payment flows, a huge productivity gain. We like the sector and we like the company due to its proven ability to provide smarter solutions to an industry in transformation as well as fast growth. As a subcontractor to the fintech players, the company does not get the same attention as those companies, but lessons learned from technological leaps in other industries are that it is often the companies that “sell the shovels to the gold diggers” who makes the most money. The market capitalization of USD 300m and the valuation (P/E 32x) would probably have looked different with a listing in a more well-known stock exchange than Casablanca. In addition, we would probably define it as one of only a few in our portfolio that is a clear acquisition candidate.

MARKET

African equity markets were unchanged in May (MSCI EFM Africa xSA Net TR +0.1%), underperforming other Frontier markets (MSCI FMxGCC Net TR), which rose 4.2% during the month. Nigeria was the best African stock market rising 8.8% followed by Namibia, rising 2.9%. Ghana was the worst African market declining 10.6% while Egypt was the second-worst performer, falling 8%. The late arrival of COVID-19 and rising numbers of infected in the African countries continue to haunt the stock markets on the continent (all changes in SEK).

Egypt (Hermes Index -8% in May, -23.6% year to date) PMI number for May recovered strongly to 40.7 in May from 29.7 in April, still below 44.2 recorded in March and still below 50 indicating a continued contraction in economic activity. The central bank kept interest rates unchanged, allowing earlier cuts more time to feed through to the economy. IMF approved a USD 2.8bn lending package and Egypt later raised USD 5bn in Eurobonds. Receiving more than USD 22bn in interest, the 30-year bond was priced at 8.875%, the 12 year at 7.625%, and the 4 year at 5.75%. This should cover the funding needs for the FY20/21 fiscal year.

Nigeria’s (Nigeria Stock Exchange Main Index +8.8% in May, -4.5% year to date) stock market recovery was led by cement producers, consumer staples, and financials. The cement names surprised with rising sales in Q1. A recovery in global oil prices helped and was reflected in Nigerian PMI going up to 40.7 in May from 37.1 in April. The central bank surprised the market and cut rates by 1%-point to 12.5%, which should support the economy going forward.

Industry numbers in Kenya (Nairobi All Share Index -4.9% in May, -19.3% year to date) showed that banks restructured almost 10% of outstanding loans in the first quarter increasing worries on what’s to come. The central bank disappointed the market by keeping rates at 7% instead of an expected 0.25%-point cut. Ghana (GSE Composite Index -10.6% in May, -13.2% year to date) also recorded a recovery in PMI as May numbers came in at 46.7, up from 31.7 in April. Morocco (MASI Free Float All Shares Index +1.9% in May, -19.8% year to date) is in talks with international lenders for new funding after borrowing USD 3bn in April from IMF. No further details are available as of yet.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.