POSITIVE MONTH WITH VIETNAM WEIGHING ON RELATIVE PERFORMANCE

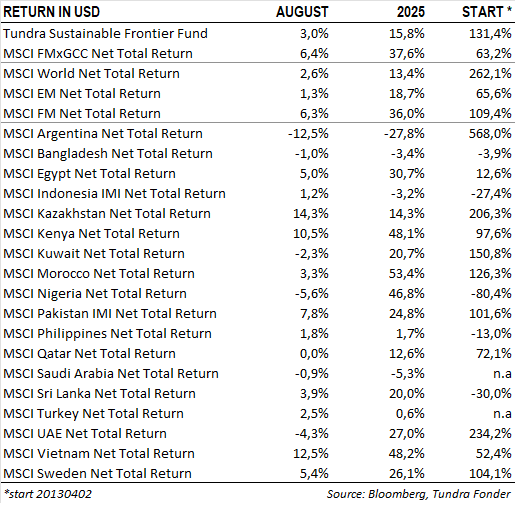

In USD the fund rose 3.0% during the month (EUR: +0.7%), compared with MSCI FMxGCC Net TR (USD), which rose 6.4% (EUR: +4.0%) and MSCI EM Net TR (USD), which rose 1.3% (EUR: -1.0%). In terms of absolute return (USD), Pakistan was the single sub-portfolio contributing most positively (+1.6% absolute contribution), followed by Sri Lanka (+0.8%) and Vietnam (+0.6%), while Nigeria (-0.2%) was the only sub-portfolio contributing negatively. Relative to the index, it was primarily our stock selection in Vietnam (-2.9% portfolio contribution relative to the index), underweight in Kazakhstan (-0.6%), Morocco (-0.5%), and Romania (-0.5%) that weighed negatively.

Among individual positions, the largest positive contributions came from Pakistan’s National Bank of Pakistan (4% of the portfolio), which rose 20%, and Vietnamese port operator Gemadept (4% of the portfolio), which rose 22%. National Bank of Pakistan rallied ahead of its half-year report. The report itself came slightly ahead of expectations, and management indicated greater dividend potential going forward, which was positively interpreted. The share has re-rated threefold since the company finally settled a lawsuit regarding historical pensions in 2024, and it is up eightfold from the bottom in the first quarter of 2023. We gradually built a position in the bank during 2018–2024. For several years, it appeared to be quite a peculiar investment, but in hindsight, it has proved to be one of our better ones of the past decade. The bank is now led by a capable management team with an understanding of shareholder interests, which has meant that its valuation has gradually approached the sector average.

We see Gemadept’s increase as a deserved partial catch-up relative to the broader market. In our view, it is the most attractive listed port operator across both frontier and emerging markets, given its relatively unique combination of low container handling charges (which will rise faster than the global average) and unusually strong expansion opportunities. The share was hit hard in the wake of tariff concerns in the spring and has now merely regained the losses suffered then.

The largest negative portfolio contribution came from Pakistani clothing manufacturer Interloop (3% of the portfolio). The share fell 9% during the month in an otherwise strong Pakistani stock market, where gains were dominated by cyclical companies exposed to the construction sector following the floods (see more below). We also recorded negative contributions from two of our larger Vietnamese holdings, REE Corp and FPT, both of which fell 3% in an otherwise strong Vietnamese stock market. In FPT’s case, the decline followed a rather weak second-quarter report, with IT services sales rising less than expected, both in the US and in Asia. To note is that the second quarter coincided with the peak of tariff concerns, but we will now see some estimate downgrades for the full year. For several years, this was our largest position. We reduced our position at the end of 2024 as we viewed the valuation had become a bit stretched. The share is down nearly 30% since the start of the year. At current levels, the share is once again beginning to look attractive.

During the month, we added two new positions. First, Bangladeshi City Bank, which falls within the same quality spectrum as our already held Brac Bank. We are positive on Bangladesh as an equity market. The country entered the crisis later than, for example, Pakistan and Sri Lanka, and has therefore endured a fairly tough period over the past two years. We now see clear signs that inflation is under control, and the increase in foreign reserves indicates that the major currency adjustment is over for the time being. City Bank is Bangladesh’s third-largest bank in terms of market capitalisation and belongs to the small group of quality banks that we believe will benefit from the ongoing consolidation in the sector. We expect foreign investor interest in Bangladesh to increase going forward, and that City Bank will be one of the first diversification options for international investors.

We also added Digital Mobility Solutions, which could be described as a “Sri Lankan UBER”. The company’s focus is ride-hailing (similar to Uber and Grab), later complemented by food and goods deliveries. During the summer, we carried out due diligence on the company, which in our eyes should still be considered a start-up. We have strong confidence in the founder and the management team and believe this is a company that will look significantly different in 3–4 years in terms of its service offering.

KEY MARKET NEWS

It was a relatively calm month on the geopolitical front, with unusually few statements from Trump, and the larger issues revolved around the potential peace process between Russia and Ukraine. Indications from the Fed regarding future rate cuts lifted sentiment in both developed and emerging markets. Lower rates in the US provide additional support for our markets, which are already in a relatively positive phase with narrower trade deficits and rising reserves. In earlier monthly letters (see February 2025), we pointed out Vietnam as a market particularly likely to welcome a Fed cut.

The largest index market, Vietnam (30% of MSCI FMxGCC), accounted for a large part of the index’s increase during the month, with a 13% rise. As earlier this year, however, it was once again a somewhat peculiar rally, centred on the financial sector and the Vingroup group of companies (read more below).

Bangladesh fell 1% during the month. Inflation rose in July to 8.55% (from 8.48% in June), primarily due to higher food prices. Consensus is that inflation will gradually ease in line with stabilising global commodity prices. Exports rose 9.5% and remittances 18.4% during the first two months of the fiscal year, which strengthened reserves. The central bank has bought around USD 1 billion to counter BDT appreciation. At the same time, the pharmaceutical sector has been hit by renewed regulatory uncertainty after the reintroduction of state price controls on basic medicines, creating risks for profitability. The Election Commission has presented a plan targeting February 2026 as a national election month, meaning politics will increasingly influence sentiment going forward.

Pakistan rose 8% during the month. Our Pakistani holdings reported mixed quarterly results, with Meezan Bank and National Bank beating expectations. Systems Ltd delivered in line with expectations, with strong growth (+18% revenues, +59% profit), while AGP and Abbott Pakistan grew earnings but failed to impress the market. Moody’s raised the country’s credit rating to Caa1, citing IMF-backed reforms and a stronger external balance. The current account showed a deficit of USD 254 million in July, but improved 27% YoY on the back of higher remittances. Meanwhile, the country was hit by severe floods in Punjab and other provinces, with over one million people displaced and significant agricultural risks. Inflation has nevertheless continued to fall (3.0% in August), meaning the central bank is expected to keep rates unchanged.

Sri Lanka rose 1% in August, but was briefly unsettled by the arrest of former president Wickremesinghe, which the opposition called politically motivated. Several former senior politicians have been detained, which could signal a new phase of accountability in politics. President Dissanayake has been praised during his first year in office, showing great responsibility and an understanding of market economics. However, he must be careful not to rekindle the mistrust many investors felt towards him just months before the election. Several of our holdings reported quarterly results. Sampath Bank reported a 17% drop in earnings, but strong growth in both lending and deposits. Hemas grew profits by 26%, driven by healthcare, while Windforce increased profits by 28% through new plants and acquisitions. On the macro side, the current account posted another surplus (+USD 245 million), bringing the year-to-date surplus to USD 1.7 billion. Market sentiment is expected to remain supported by improving macro data and IMF-backed reforms.

A TESTING YEAR – BUT THE OUTLOOK IS BRIGHT

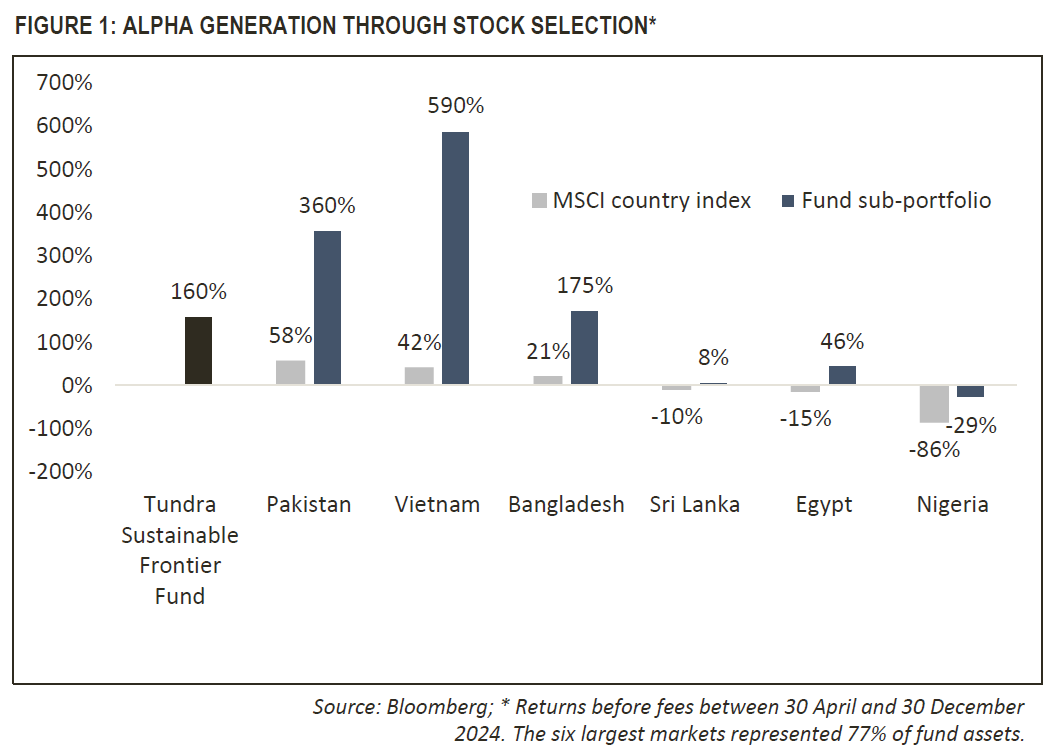

It has been a somewhat unusual year where, on the one hand, we note clearly positive developments in our core markets, but at the same time, we have yet to see a clear pay-off in the fund. Tundra’s definition of frontier markets is low-income and lower-middle-income countries. Over time, investors can expect the overwhelming majority of the fund’s exposure to be in these countries. This year, however, these markets have not been able to match the index-heavy winners, Morocco (+53%, 16% of the index) and Romania (+40%, 12% of the index). For many years, we have been able to compensate for weak market performance in our countries with a strong stock selection. The chart below shows the fund’s gross return (in USD) before fees relative to the six largest markets since inception. The grey bars represent the performance of each market, the blue bars the fund’s country portfolio in the same market. Notably, the fund has outperformed each of the six largest markets we have invested in since inception. Our ability over time to select the right stocks is the key reason why we dare to take such significant overweights in individual markets, such as Pakistan.

As can be seen in the chart, Vietnam has been one of the markets where we have been particularly successful over time. Last year was also exceptionally strong. The sub-portfolio rose 49% against the market’s -6% (USD). However, this year has been particularly weak, with our Vietnamese sub-portfolio down 6%, while the index is up 48%. When we dissect the index development and review the list of the twenty largest contributors to the index, we conclude that, with perhaps the exception of one or two banks, these are companies we will always avoid.

At the top of the list is the conglomerate Vingroup (+206%), which in our eyes remains a clear example of a vision gone astray, resulting in capital destruction. We believe the share will eventually stabilise at no more than half its current level, and even then, the owner must demonstrate a genuine interest in creating shareholder value to attract investors.

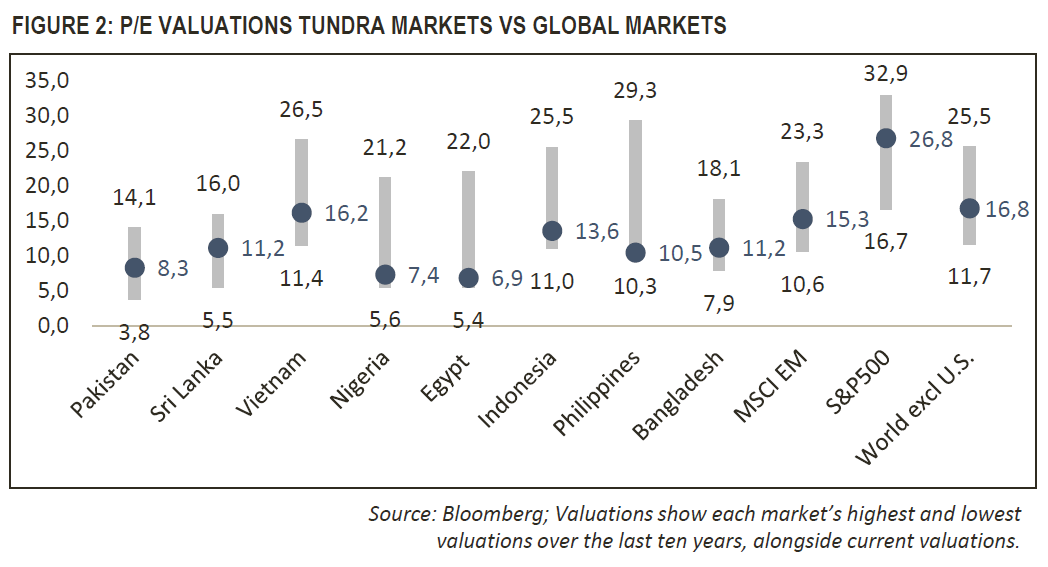

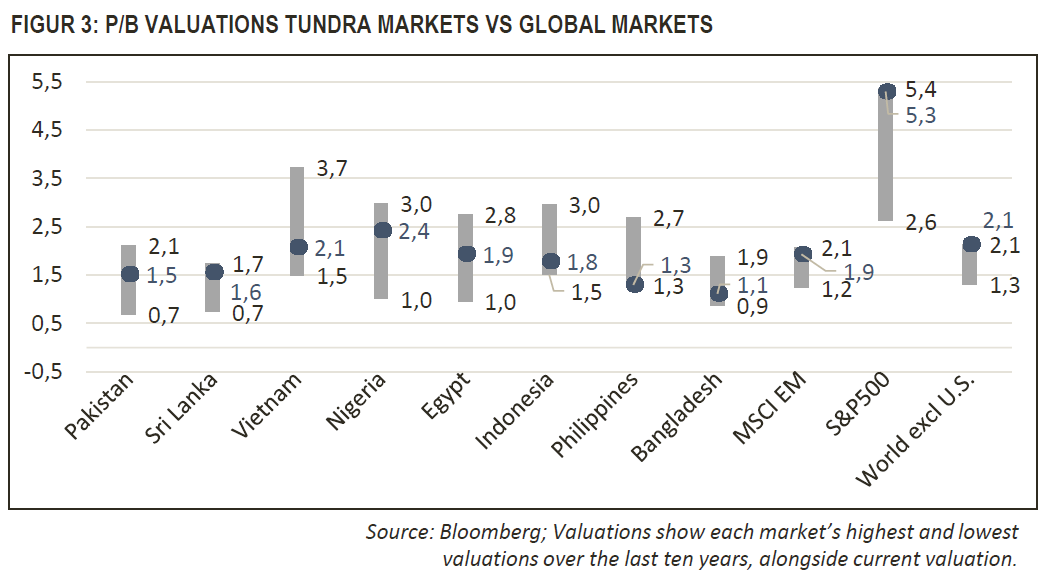

Looking ahead, one must begin by noting that the outlook has rarely been so free of potential roadblocks. The worst pessimism is behind us. With few exceptions (the Philippines), we have left the most extreme valuation troughs (see Figures 2 and 3). Some of our markets, such as Pakistan and Sri Lanka, are back at their ten-year average valuations, but we are still well below the decade’s peaks.

We believe there is reason to believe we are entering a new cycle and that we are still in the early stages of a longer-term trend:

• In all the years we have managed the fund, there have almost always been at least one or two major concerns in individual markets, such as risk of devaluation or political instability. The crisis recently endured by Sri Lanka, Pakistan, Egypt, Nigeria, and Bangladesh was the deepest we have witnessed in three decades. Experience shows that the deeper and more protracted the crises, the longer the recoveries tend to last. After the Asian and Russian crises of 1997–98, for example, followed a very strong decade for the smaller emerging markets, right up until the global financial crisis of 2007–08.

• The world is changing rapidly. Unpredictable leadership in the world’s largest economy has made the need for diversification clearer to many. At the same time, we now face new global economic conditions. Even though further rate cuts are likely in developed markets, it is improbable that we will again see the near-zero interest rates that prevailed in Europe and the US between May 2009 and spring 2022. During that period, we were not only competing with a stellar US stock market, but also with real estate, private equity, and speculative companies for which profitability was of secondary concern. One cannot blame global investors for choosing the easy route. If they could borrow at 0.5%, achieve 2% returns, and leverage the investment three times, there was little reason to bother with exotic markets, which are perceived as risky.

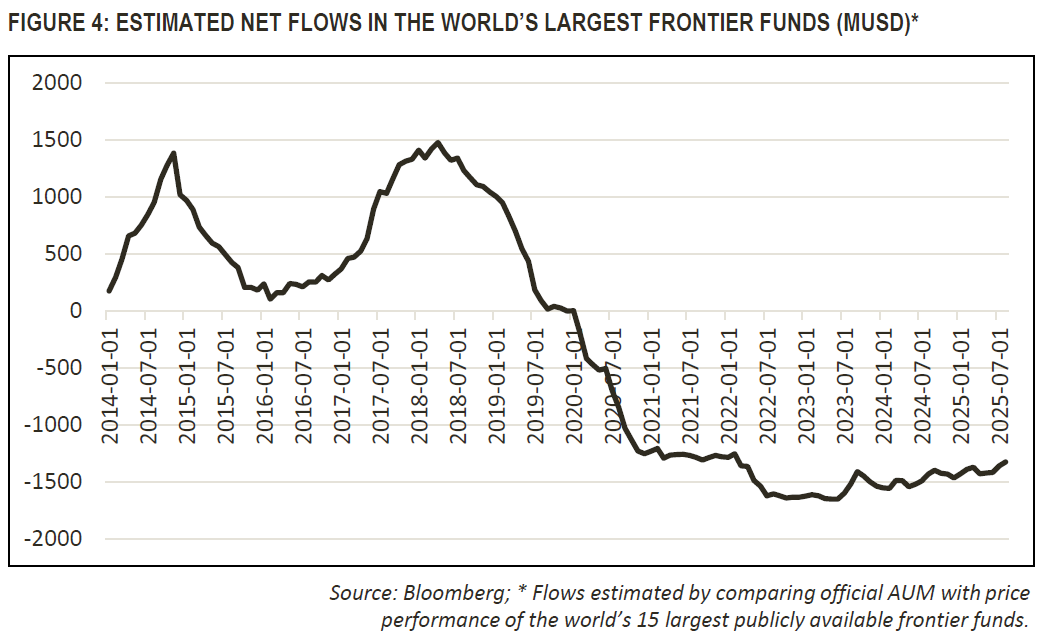

• We are now back in a more normal rate environment, while the geopolitical situation means the world’s largest economy no longer necessarily appears as the safe haven it has been in recent decades. Much, therefore, suggests we will see more diversification decisions in the coming years. The last peak of interest in frontier markets was in 2014. From spring 2018, outflows were relatively constant for six years (see Figure 4), before flattening out. Without constant crisis headlines about devaluations, debt restructurings, and runaway current account deficits, the stability may now emerge that is needed for investors to return. At Tundra, we already see growing curiosity from foreign investors, and we consider it likely that capital flows will improve in the coming years.

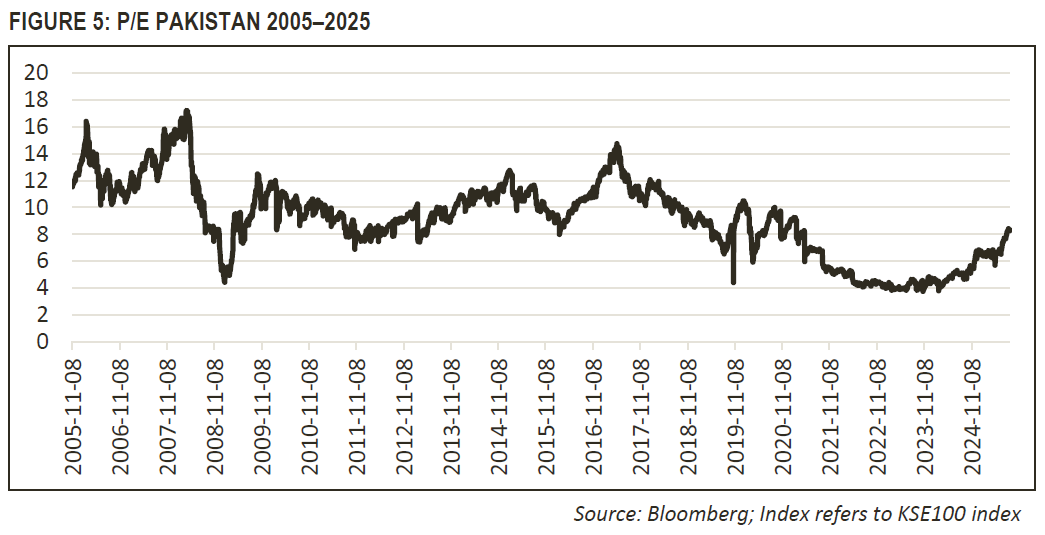

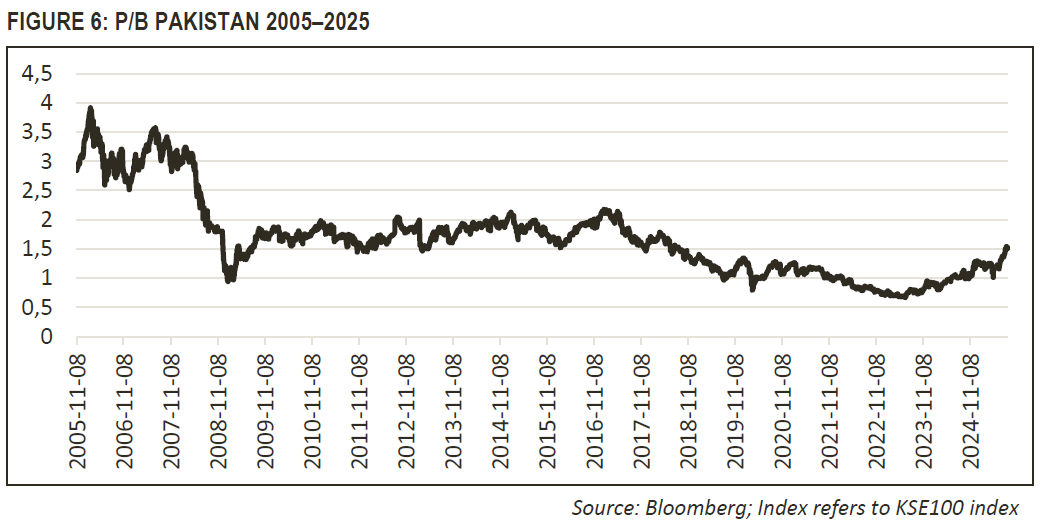

• The first recovery phase is behind us, the phase in which the most pessimistic expectations are disproved and markets bounce back to a more normal valuation range. Frequent readers of our monthly letters know how we like to compare current equity and earnings valuations with each market’s ten-year average. In the initial upswing, this was a reasonable main argument (i.e., “do not be overly pessimistic”). It is however important to remember that the past ten years have been very weak for most of our markets, with constant crises and unusually sharp currency depreciations, which affected risk appetite and valuations. It may be that we are now entering a new phase where we can look back to periods when such concerns were not in focus, and our markets were viewed through a more neutral lens. If we look even further back to more optimistic periods, valuations still appear modest. A good example of this is our largest market, Pakistan.

We are emerging from 15 years of complete US dominance in global investments. A whole generation of fund managers has grown up in a climate where it was almost pointless even to glance at other markets. But there are now plenty of arguments as to why our markets should be entering a better period. As a frontier market fund manager, one becomes hardened. There will certainly be negative surprises along the way. But when we study each market, what it has endured and where it stands now, we think that we are likely to have several years ahead of us with a more normal market environment, where higher nominal profit growth is not largely eroded by recurring devaluations or declining risk appetite resulting in multiple contractions. Our existing base case is that we should have 5–6 years of a very favourable market climate ahead of us. What happens thereafter, and how sustainable the improvement proves to be, will depend on the lessons our markets draw.

___________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.