STRONG MONTH DRIVEN BY KEY HOLDINGS IN PAKISTAN AND BANGLADESH

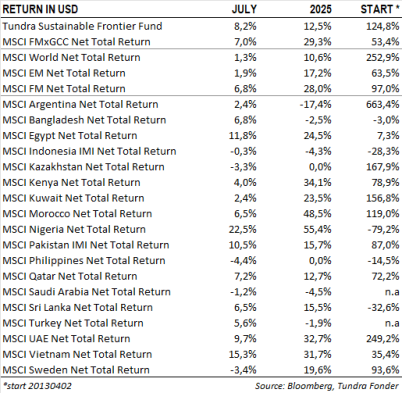

In USD the fund rose by 8.2% during the month (EUR: +11.0%), compared to an increase of 7.0% for the MSCI FMxGCC Net TR (USD) (EUR: +9.9%), and 1.9% for the MSCI EM Net TR (USD) (EUR: +4.7%). In terms of absolute return (measured in USD), Pakistan was the single largest positive contributor (+4.2% absolute contribution), followed by Bangladesh (+2.3%) and Egypt (+1.3%), while Philippines (-0.2%), and Kazakhstan (-0.1%) were the only sub-portfolios to detract. Relative to our benchmark, the main positive contributions came from our overweight and stock selection in Pakistan (+3.7% relative contribution), Bangladesh (+2.3%), Egypt (+1.4%), Nigeria (+0.7%), and Sri Lanka (+0.5%). These more than offset the continued weak stock selection in Vietnam (-4.2%), and our underweight in Morocco (-1.1%).

Among individual holdings, the strongest positive contributors were Pakistani Systems (8% of the portfolio), which rose by 28%, and Bangladeshi BRAC Bank (6% of the portfolio), which soared by 39%. Systems rallied primarily on the announcement of its acquisition of an international business services (BPO) company, combined with news of a significant service agreement with Accenture. This marks a notable step towards commercialising a new type of service, which could have a meaningful impact on the company’s future earnings growth. BRAC Bank led the advance in a reawakened Bangladeshi equity market. We interpret the rally in Bangladesh as a response to the country’s (expected) improvements in macroeconomic indicators, and signs that higher-quality banks are gaining significant market share. During the month, we observed notable foreign investor interest in the bank. The main detractor was Philippine company Century Pacific (3% of the portfolio), which fell by 10% amid a weak domestic equity market in July.

KEY MARKET DEVELOPMENTS

Easing concerns over US tariff measures provided broad support to the markets throughout the month. Pakistan, Vietnam, Bangladesh, and Sri Lanka all concluded agreements in line with the more optimistic expectations among market participants. However, we note the persistence of the more discretionary elements of the negotiations, with both Brazil (50% proposed tariffs) and India (25% + additional 25%) temporarily falling out of favour with Trump for reasons likely beyond trade balances alone.

Vietnam rose by 15% during the month. The resolution of the tariff discussions was a key factor, with the US and Vietnam ultimately agreeing to a 20% tariff rate—down from the initial proposal of 46%. The strained relationship between the US and India (currently facing tariffs of 50%)— Vietnam’s most significant competitor for foreign direct investment—was also a supportive element. However, part of the rally in Vietnam could be characterised as lower quality, with gains driven primarily by more speculative and volatile names, such as the Vingroup companies and brokerage firms. By comparison, the broader domestic VN Index rose by “only” 9% over the month. Nevertheless, appetite for Vietnamese equities has clearly returned, and sentiment has improved markedly.

Another strong performer was Pakistan, which climbed 11% during the month. The US and Pakistan agreed on a 19% tariff rate for Pakistani exports—at the lower end of projections among more optimistic analysts. Talks of potential US investments in Pakistan’s commodity sector were also well received. Positive economic data, including the country’s first current account surplus in 14 years and a credit rating upgrade by Fitch, further improved sentiment. The acquisition of an international BPO firm by flagship company Systems (up 28% over the month) also boosted confidence among local investors.

___________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.