THE FUND OUTPERFORMED DURING A ROUGH MONTH

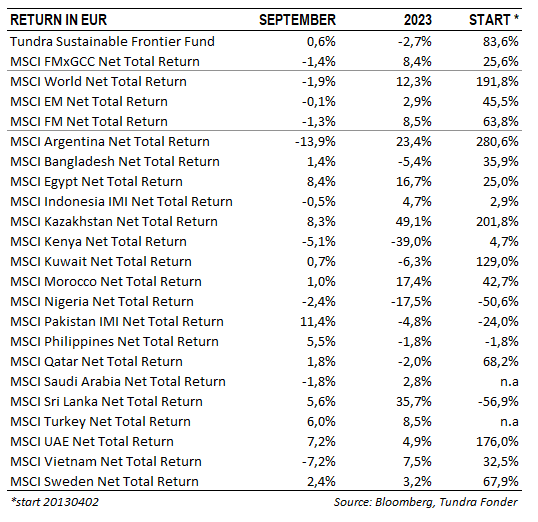

In USD, the fund fell 1.9% during the month (EUR: +0.6%), compared to MSCI FMxGCC Index Net TR (USD), which fell 3.9% (EUR: -1.4%), and MSCI EM Net TR (USD), which fell 2.6% (EUR: -0.1%). During a turbulent month, positive contributions were limited to Pakistan and the Philippines. Our Pakistan sub-portfolio rose 6% during the month and contributed 0.9%-points to the fund’s absolute return. The Pakistani rupee strengthened 6% against the US dollar during September after Pakistani authorities cracked down on currency smuggling and signaled that elections will be held in January 2024. Textile company Interloop, whose competitive advantage primarily is its well-developed sustainability framework, rose 31% during the month after another strong set of results.

In the Philippines, our holdings in Century Pacific Foods (long shelf-life foods) and Puregold (grocery chain) rose by 4% each. Century Pacific shares were included in local indices during the month while Puregold rose on hopes of gradually improving consumer demand after two tough years. Despite growth being in line with our expectations (8-10% per year), Puregold has had difficulty attracting investors, given continued weak investor interest in the Philippines. The stock now trades at a P/E of 8.7x on 2023 expected earnings, compared to 19.7x on average over the past ten years and 14.8x over the past five years. It can be compared with Swedish Axfood, which has a similar local market position in Sweden (one of the three largest grocery retailers). Axfood is valued at around 20x 2023 earnings and is expected to grow significantly slower (3-4% per year). The majority of Puregold’s business is explicitly aimed at Filipinos in the lowest income categories, which means that the company’s target market over time is expected to be the fastest growing.

The largest negative contributions during the month came primarily from Vietnam (-0.8%-points) and Egypt (-0.7%-points). The Vietnamese stock market fell 10% during the month and was primarily dragged down by the Vingroup companies (approx. 20% of the index, distributed among three companies: Vingroup, VinHomes, and VinRetail) where the fund has no investments. Vingroup stocks came under pressure because of concerns about the group’s unknown financing commitment for the separately listed EV manufacturer VinFast (see previous monthly newsletter). We met Vingroup and VinFast during our recent trip to Vietnam (see more below). Our Vietnamese sub-portfolio fell 3% during the month. The biggest negative contributor was the IT company FPT Corp, which fell 5% during the month. However, it must be put in relation to the share’s rise of 38% (USD) since the turn of the year. In Egypt, two of our holdings, GB Corp (fintech and automobile) and Juhayna (dairy and juice) fell 11% and 13%, respectively, after a couple of months of strong performance.

IMPRESSIONS FROM OUR TRIP TO VIETNAM

We are just back after a week in Vietnam, where we visited Hanoi (the capital) and Ho Chi Minh City (the country’s main business hub). We met our largest portfolio companies but also a number of the country’s leading companies in various sectors, as well as representatives from both the central bank and the stock exchanges. Based on economic statistics alone, Vietnam (with the exception of raw material exporting Indonesia) is one of our markets that coped best with Covid-19 and the subsequent inflationary shock. Growth fell from a steady 6-8% in the years 2013-2019 to below 3% in 2020-2021, but then recovered to 8% in 2022. Unlike most emerging markets, inflation remained relatively modest and came in at just over 3% in 2022. The Vietnamese currency, the Dong, has been one of the most stable emerging market currencies, depreciating only 4% against the US dollar over the past three-year period. A beacon of stability compared to countries such as Bangladesh, Egypt, Pakistan and Sri Lanka.

Behind the economic statistics, however, the picture has been more complex. Vietnam’s high economic activity and good access to capital have meant a strong expansion of credit to the real estate sector, and consumer credit is also significantly more common in Vietnam than in any of our other countries. About 7 million Vietnamese (7% of the population) have a stock account with some broker. It is more than 10x higher than in any of our other markets. Leverage is available, and common. The country has an unusually high level of trade (exports and imports together are roughly 200% of GDP with a certain trade surplus). Exports from foreign companies with operations in Vietnam make up roughly 70% of total exports and investments continue. Vietnam remains one of the countries that benefit from the so-called reshoring trend, i.e., foreign companies’ production that is reallocated from other countries (primarily China as of recent). However, the slowdown in global demand has meant that the number of overtime hours has decreased for Vietnamese workers. This has affected their ability to consume. In addition, the higher interest rates, especially in 2022, have meant higher interest costs and less room for consumption. The equity market’s 30% decline in 2022 was also a blow to the part of the population that invests in the equity market. During 2021 and 2022, several lending scandals and corruption problems emerged in the real estate sector, which created concern and limited the opportunities for real estate companies to finance themselves outside the banking sector.

The Vietnamese Dong has experienced some pressure. Vietnam’s relatively low deposit rates (from an emerging market perspective) have meant that more capital from the foreign companies on site has been repatriated (brought home) to be invested at higher interest rates in other countries. Thus, the central bank is currently in a dilemma. To keep private consumption up, lower interest rates are needed, which could also be justified by the more modest inflation, but at the same time, the low (relative) interest rate risks weakening the currency, creating anxiety among the population, and ultimately raising inflation. Many Vietnamese still remember the period 2008-2011 when inflation in two waves reached 20% and the dong over a three-year period weakened 25%. The country does not want to risk ending up there again.

Vietnam’s tremendous economic progress, including its ability to attract international capital, over the past ten years makes the country relatively unique. It has taken the step into the global economy and is moving forward faster than any of our other markets. With this integration, however, there are also periods when you get to taste the flip side of the coin, the increased influence of external factors. Vietnam remains in a structural growth phase with the continued inflow of foreign investment. We also like the awareness of the need to invest in human capital and to create more sustainable competitive advantages, in a similar way that South Korea and Taiwan have succeeded. A country that wants to go all the way to a high-income country must constantly develop, and the local companies must follow the development. The way Vietnam has dealt with the corruption scandals and the problems in the real estate sector also shows the ability to quickly take measures that stabilize difficult situations. In the short term, however, Vietnam finds itself in a dilemma where it must act with caution and with consideration of global developments, not least global interest rate developments.

COMPANY MEETINGS IN VIETNAM

On the trip, we met our portfolio companies and several of the larger listed companies in various sectors. In general, they described the current economic situation as a continued subdued level of activity, but with gradual improvements going forward. As always, it is about which sector they operate in and to what extent the companies have been affected by the somewhat tougher climate of recent years.

IT company FPT, which is the fund’s largest position, has had a good year. The share price is up 38%. Declining demand locally for IT services has been compensated by increased demand abroad, especially from Japan. REE Corp, which is the fund’s second-largest position, has also fared well. The development of renewable energy is a structural trend that is only marginally affected by declining economic activity. An important customer category for their solutions in rooftop solar panels is foreign companies that operate in industrial parks. Demand from these customers remains strong. REE also has a group of properties located not far from Ho Chi Minh City’s current airport, where during the year, it primarily worked on completing its latest office building (E-town 6). Upon completion, it will become one of the three largest owners of commercial real estate in the city. The vacancy rate has increased from 1-2% to 3-4%, but they are now seeing a stabilisation. The new property should be completed by the end of the year and the company expects 80% occupancy before the end of 2025.

One of the more memorable visits was when we visited EV manufacturer VinFast’s production facility in Haiphong (on the coast, 1.5 hours outside of Hanoi). The factory is twice the size of Tesla’s first factory and has the capacity to produce 300,000 cars a year (this year around 50,000 cars are expected to be sold). The level of ambition is high, the factories are equipped with the absolute latest technology, including a high degree of robotization. We got to test drive the latest models and those with longer experience with other EV manufacturers (including Tesla) said that the cars stood up well to the competition. However, the question you must ask yourself is the group’s financial strength. Enormous investments are required to fulfil the company’s ambition to become a major car manufacturer, and branding is very important. Will car buyers in the next few years be prepared to pay almost as much for a VinFast car as they are for a Mercedes or a Tesla? The uncertainty surrounding financing has hit the parent company Vingroup (owns 49% in VinFast) hard. It is fantastic to see the level of ambition that is being shown, but from a crass investment perspective, we find it difficult to be convinced. VinFast was listed through a SPAC listing in the USA in August 2023 and initially reached insane valuation levels of almost USD 200 billion. End of September, the market capitalization was USD 28.8 billion. It is important to put each company in context. Even this valuation requires that the company sells approx. 1 million cars (20x more than expected for 2023), shows profitability in line with Tesla (approx. 10% net margin) and is valued at P/E 10x (note: Both BMW and Ford are valued at just above P/E 6x and are showing net margins of 4-7%). One should also not forget the need for investment that would entail tripling one’s production capacity. It is of course not impossible that the project will ultimately be profitable for the investors, but the odds are not in their favor. The upside risk is that the company somehow succeeds in persuading new investors to invest in the project at current or even higher valuations, or that it receives government support to realize it. None of these options are completely unrealistic, but not nearly enough for us to consider an investment.

HOW ARE OUR PORTFOLIO COMPANIES FARING?

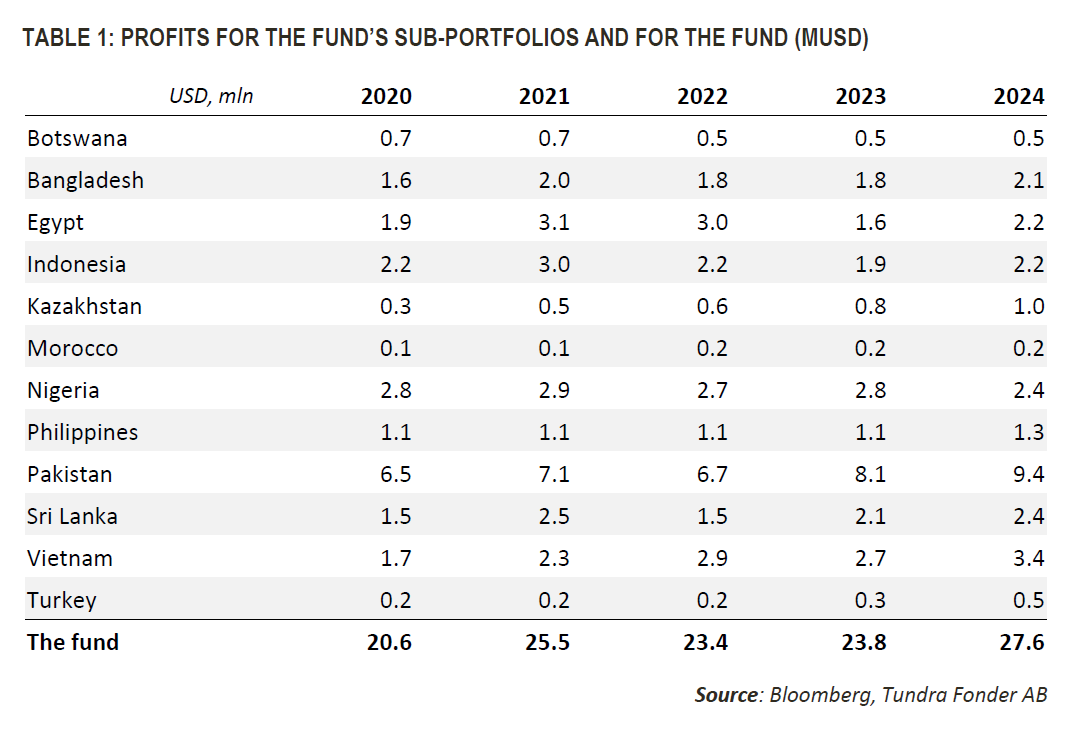

We continue our quarterly update of the profit development in the portfolio companies, where the purpose is to illustrate the difference between price development and actual fundamental development in the companies we own (See monthly newsletter of March and June for background). Table 1 shows the fund’s profits distributed at the country level (each owned share x profit per share). To calculate the P/E ratio for the fund as a whole, the portfolio NAV (MUSD 175.6 ex cash per 30/9) is then divided by the fund’s total earnings, i.e., the expected P/E ratio for 2023 is 7.4x (175.6 / 23.8 = 7.4). Table 1 below illustrates the historical profit development for the current portfolio (i.e., current number of shares, back to 2020). Here you can also understand the sensitivity to changes in estimates in individual markets. For example. a 10% drop in earnings in Vietnam would cause the portfolio’s P/E ratio valuation to rise from 7.4x to 7.5x, while a corresponding fall in Pakistan would see the valuation rise to 7.6x.

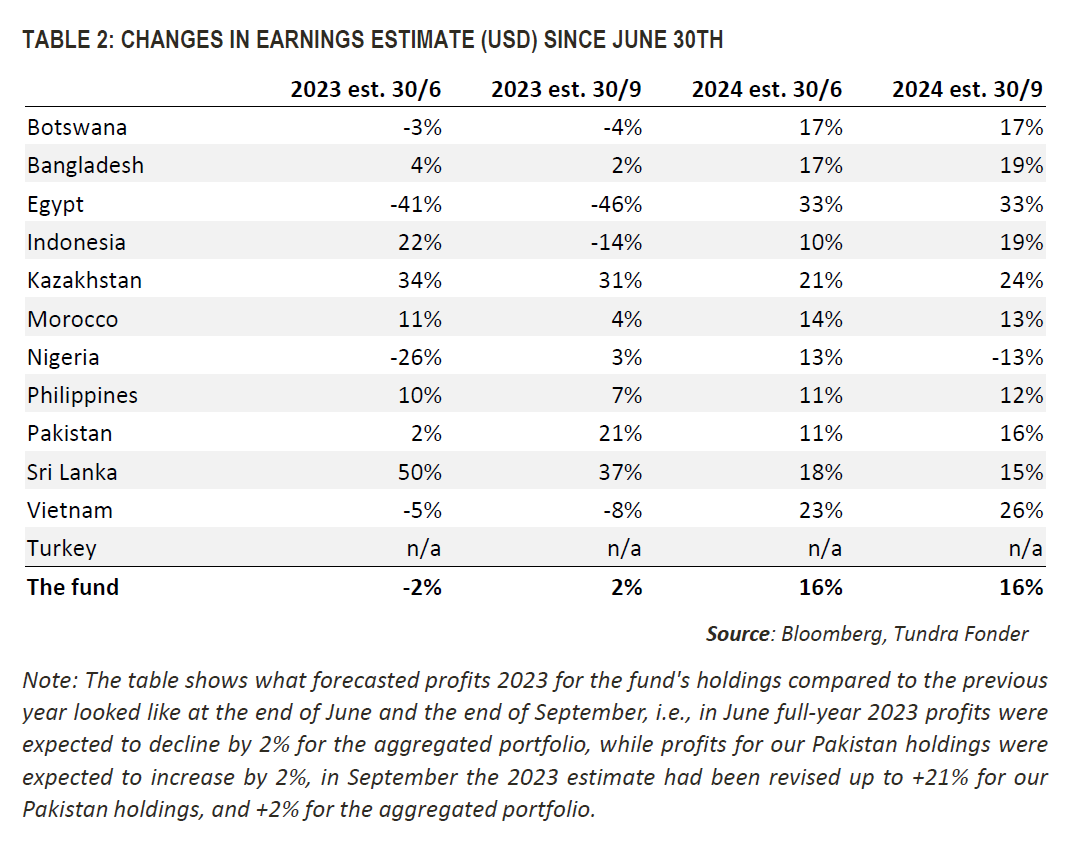

Table 2 shows how the estimates have changed since the previous measurement (June 30). At the portfolio level, the profit estimate has been adjusted up 4%-points since June 30th, from -2% to +2%. A lot has happened in individual countries. Profit estimates for our holdings in Pakistan have been adjusted upward significantly, mainly due to the banks’ higher profitability in the current high-interest rate environment. For 2023, the market is probably right, but it is likely to be optimistic to adjust the 2024 estimates as well, given the higher base effect for 2023. However, the adjustments in Pakistan are a useful reminder that negative headlines are not always reflected in companies’ earnings.

Estimates among our Nigerian holdings have also been revised up significantly following the half-year reports that showed large trading gains in the wake of the devaluation, however, the market (probably correctly) does not expect the gains to be sustained, as reflected in the changes to estimates for 2024. The earnings estimate in Indonesia has been revised down significantly, mainly due to major downward revisions in estimates for Media Nusantara (3% of the portfolio) following their weak half-year results. Similarly, estimates in Sri Lanka have been revised down from previously very high estimated 50% earnings growth. For 2024, the estimates are unchanged at the portfolio level, although the expected higher base for 2023 is carried forward.

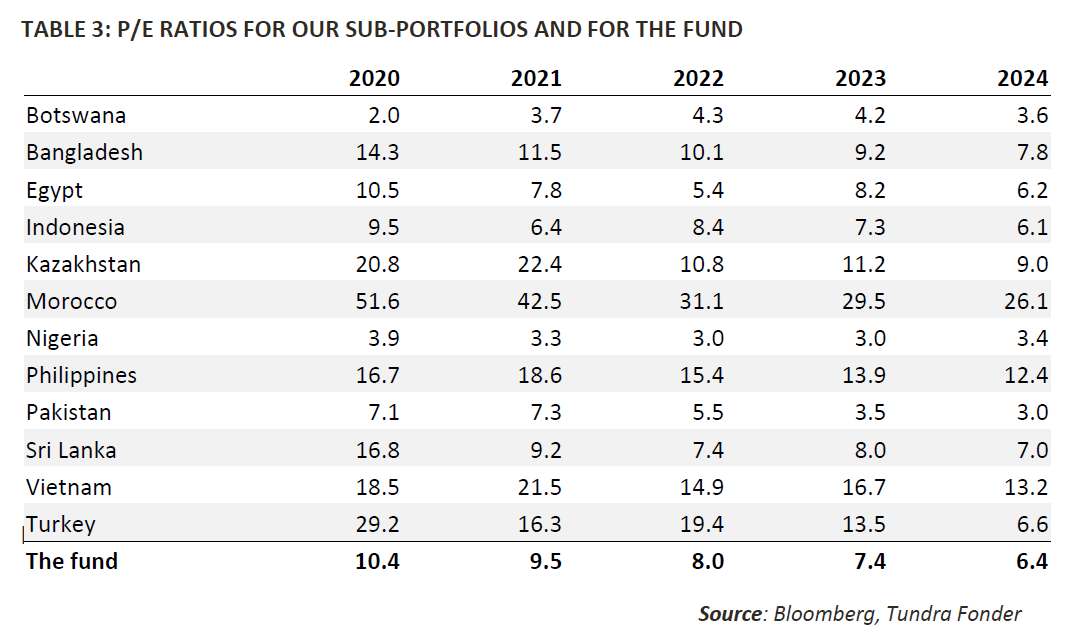

In Table 3, we look at the valuations for 2023 and 2024, which are basically unchanged since 30/6 (then P/E 7.5x and 6.4x, respectively). This is explained by the fact that the fund has risen 2.8% in USD since the previous quarter’s change. We note that the current portfolio held at the end of the quarter was valued 29% higher (P/E 9.5x vs. 7.4x) at the end of 2021 and 41% higher (10.4x vs. 7.4x) at the end of 2020. Expectations are thus still low, which in a positive scenario should mean an upside from higher multiples and in a worse scenario provides good protection on the downside.

______________________________________________________________________

TUNDRA SUSTAINABLE FRONTIER FUND REPLACES THE SWAN WITH THE EU’S REGULATIONS FOR SUSTAINABILITY

In connection with the new EU regulation under the Sustainable Finance Disclosure Regulation (SFDR), new requirements are applied to funds’ sustainability work as of March 2021. Tundra has therefore decided on July 4 not to continue with the Nordic Ecolabelling of the fund. According to the new regulations, sustainability reporting must take place in a uniform manner and funds are divided into different categories. The Tundra Sustainable Frontier Fund is classified as an Article 8 fund (Light green: promotes environmental or social characteristics). The investment philosophy of the fund remains the same; management of the fund and is not affected by the change.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.