PAKISTAN JUMPED DURING A WEAK MONTH

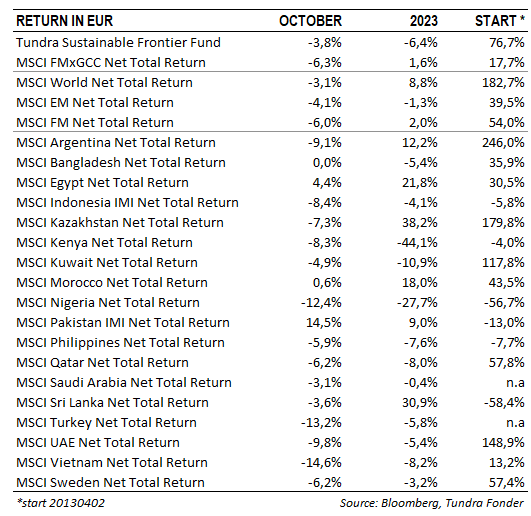

In USD, the fund fell 3.6% during the month (EUR: -3.8%), compared to MSCI FMxGCC Net TR (USD), which fell 6.1% (EUR: -6.3%) and MSCI EM Net TR (USD), which fell 3.9% (EUR: -4.1%). In USD, the largest absolute contribution (+2.2% portfolio impact) was received from Pakistan, where both the market and our sub-portfolio rose 14%. The second-best contribution came from Indonesia (+0.6% portfolio impact), where our largest holding, Hermina Hospitals, rose 13% after a strong interim report, where growth and margin targets were also raised for the coming year. We also received a positive contribution from Egypt (+0.4% portfolio impact), where our sub-portfolio rose 4% as the recovery continued despite the unrest in the Gaza Strip. The biggest negative contribution during the month (-4.3% portfolio impact) came from Vietnam, where our sub-portfolio fell 16%, slightly underperforming the market (-14%).

Pakistan’s rise during the month can be explained by decreasing political and economic uncertainty combined with extremely depressed valuations. Most indications right now are that the new government will be led by the PML-N with the returning Nawaz Sharif as prime minister. The election date is set for February 11, 2024. While Sharif’s return likely minimizes the likelihood of far-reaching reforms, it represents a familiar environment for business from the past 10 years. The market also senses that the peak of the inflation cycle has passed for this time. Inflation for October came in at just under 27%, compared to the peak of 38% in May. Market consensus expects inflation will fall to between 14-17% at the end of 2024 and that the policy rate will be cut by 500-600 basis points from the current very high policy rate of 22%. Thus, if no further unexpected shock occurs, we enter 2024 with expectations of some form of political stability and falling interest rates.

During October, the market (KSE100 index) actually set a new all-time high in local currency and thus passed the previous peak from May 2017. However, given the sharp weakening of the Pakistani rupee over the past 6 years, the stock market is down over 60% in US dollar terms. During the same period, listed companies’ profits have increased by 200% in local currency and 25% in US dollars. The valuation in May 2017 was P/E 12x and today it is 4x. When we highlight Pakistan as an interesting equity market, it has never been about how well-managed the country is. The case has always been the presence of a large number of very well-managed companies that through decades have learned to handle difficult local conditions. Foreign investors have always underestimated the resilience of companies in bad times. A top-down strategy (an analysis based on overall macroeconomic conditions) must be done down to the company level. The fact that this is rarely done explains large parts of fluctuations in smaller emerging markets, which tend to be either in a state of exuberance or deep pessimism. The reality on the ground is most of the time different. In the long-run equity markets are driven by profit growth (theoretically by the cash flow trend). Pakistan has in the last 6 years gone through the worst crisis the country has seen in the last 30 years. An investor’s worst nightmare, you could say. What happened? Corporate profits in USD have increased by 25%. The average P/E ratio over the past ten years is 8.7x annual earnings, compared to 3.7x currently. We believe the conditions are good for the country now, entering a period where the stock market is gradually finding its way back to its historical multiples.

In the previous monthly newsletter (link: https://t.co/k7NHu34TaG), we discussed in more detail why the equity market in Vietnam has gone through a turbulent period. Good access to capital and rapid credit expansion has meant that both the population and companies need lower interest rates. At the same time, the central bank finds it difficult to satisfy this request because it risks weakening the currency. Few central banks in the world are probably currently more interested in the actions of the US central bank than Vietnam. Vietnam’s flagship conglomerate VinGroup is surrounded by rumours of financing problems in its prestige project VinFast, and other companies with some kind of refinancing need are also drawn into the worries. Consumer companies are weighed down by the wariness of Vietnamese consumers in this environment. Of our Vietnamese sub-portfolio, consumer companies (Mobile World & Masan Group) make up just under 20% (4.5% of the entire fund’s managed capital). Both companies fell more than 20% during the month ahead of expectedly weak Q3 reports.

The unrest in the Gaza Strip initially caused concern in the world’s stock exchanges, but after relatively modest reactions in neighbouring countries, the markets calmed down. The market’s worst-case scenario is that more countries enter the war, which could mean significantly higher oil prices. The fact that oil prices fell during the month should be seen as an indication that the likelihood of this remains low.

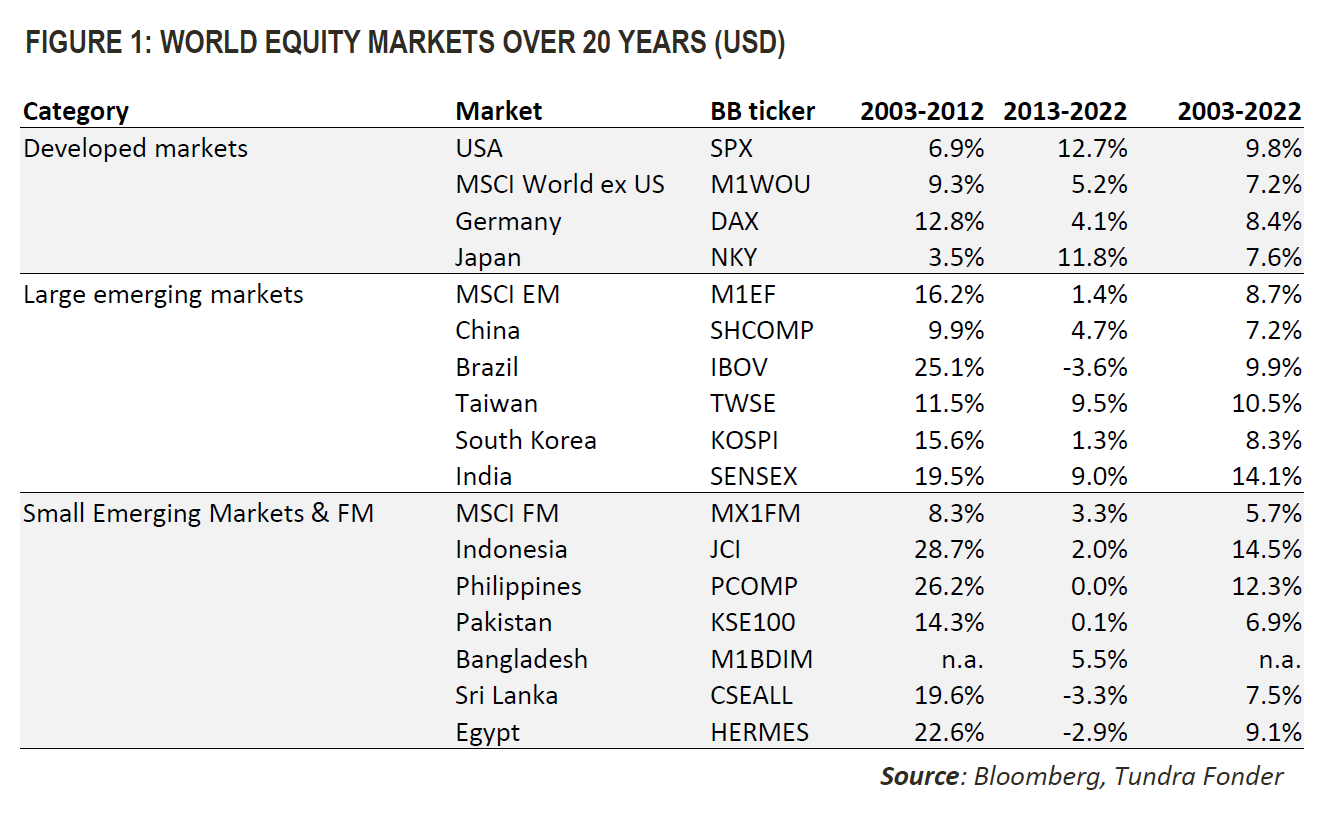

Emerging markets never got to enjoy the extremely low and/or negative interest rates introduced in the US and Europe after the global financial crisis. From April 2009, Europe and the US benefitted from essentially zero interest for just over 13 years. An experiment of modern monetary theory that came to an abrupt halt in 2022 but was highly contributory to developed markets, led by the US, outperforming emerging markets in the last decade. Emerging markets have lived under different conditions. During the same period, the central banks in emerging markets continued to act according to a traditional monetary policy where the interest rate was used as a control instrument to manage inflation expectations. The outflows of foreign capital have also meant that they have been forced to maintain higher interest rates than would normally be necessary to keep the balance of payments under control. They were never close to the environment that characterized the US and Europe. Instead, they were generally quicker to react when inflation globally started climbing in 2021 and in many cases have had to act more aggressively to maintain investor confidence.

As we now enter a period of declining inflation, it is likely that emerging markets will once again be slightly ahead of developed markets. China is already in a phase of monetary policy stimulus, Brazil first raised rates in March 2021 but started cutting interest rates in August. In smaller growth markets that have been in crisis, the movements can be particularly large. Sri Lanka has cut the policy rate by 550 basis points in 2023, and Pakistan is expected to follow suit in 2024 (the market expects a cut of at least 500 basis points). Interest rates in developed markets will also come down again. However, the side effects from the period 2009-2022 will likely remain in the memory of the world’s central banks and what awaits is likely a period where it will again cost to borrow money and developed markets’ massive advantage from the last decade will as a result be reduced. A concrete way to express it is that it will no longer be worth buying a property that yields 2% because of the ability to borrow at 1%. Making money will be a little more difficult and it may again be worthwhile for developed market investors to look outside their home market. As can be seen in Figure 1, the last ten years have been tough for emerging markets with few exceptions (India and Taiwan). From 2013-2022, the US was essentially the only market investors needed to own, as S&P 500 outclassed emerging markets. The decade before that, the roles were reversed, and the very best equity markets were found among the smaller emerging markets. After ten weak years, concluded by the worst crisis smaller emerging markets have seen in 30 years, and with improvements in sight, a period of higher returns should follow.

______________________________________________________________________

TUNDRA SUSTAINABLE FRONTIER FUND REPLACES THE SWAN WITH THE EU’S REGULATIONS FOR SUSTAINABILITY

In connection with the new EU regulation under the Sustainable Finance Disclosure Regulation (SFDR), new requirements are applied to funds’ sustainability work as of March 2021. Tundra has therefore decided on July 4 not to continue with the Nordic Ecolabelling of the fund. According to the new regulations, sustainability reporting must take place in a uniform manner and funds are divided into different categories. The Tundra Sustainable Frontier Fund is classified as an Article 8 fund (Light green: promotes environmental or social characteristics). The investment philosophy of the fund remains the same; management of the fund and is not affected by the change.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.