DAWN IN FRONTIER MARKETS

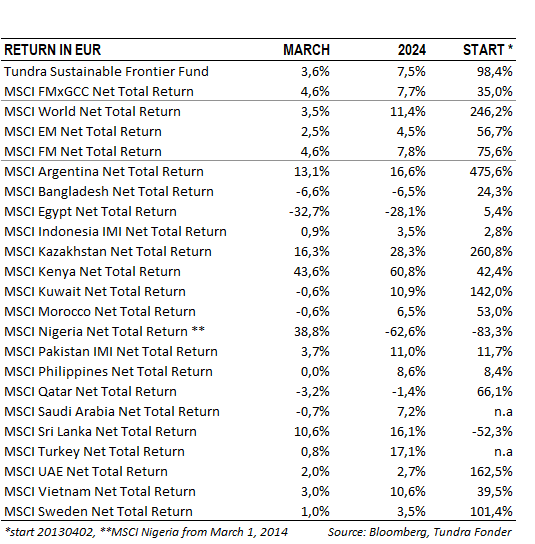

In USD, the fund rose 3.3% (EUR: +3.6%) compared to MSCI FMxGCC Net TR (USD), which rose 4.2% (EUR: +4.6%), and MSCI EM Net TR (USD), which rose 2.2% (EUR: +2.5%). In absolute terms, we received the largest positive contributions from Pakistan, Vietnam, Kazakhstan, and Nigeria, while Egypt weighed on portfolio returns following the country’s devaluation.

In Pakistan (20% of the portfolio), our sub-portfolio rose 7% in USD, compared to the market, which rose 4%. The main contributions came from our two bank positions. The biggest of them, Meezan Bank, rose 18% during the month. Even after this year’s rise of 40%, the country’s fastest-growing bank is valued at around 4x earnings with a dividend yield of 9%. Our second banking position in Pakistan, National Bank of Pakistan, rose a whopping 37% after the Supreme Court finally ruled in a legal case concerning the company’s pension debt to former employees that has weighed on the share price for several years. The ruled payout was lower than the market’s expectations, but more importantly means that the company now can resume its dividend, which has been withheld for the past seven years pending the outcome of the court case. In 2014-2016, the company paid out between 69-79% of its profit in dividends. It can be put in relation to the current valuation of approximately 1.5x the annual profit. Even if we adjust for a more normal interest rate climate, the company’s current valuation should be at 2-2.5x annual profit, which could mean a dividend yield of 30-40% going forward, at current price levels. That is roughly twice as high as the average in an already low-valued sector, in a market that we believe is at the beginning of a long-term upswing.

In Vietnam (25% of the portfolio), our sub-portfolio rose 5%, compared to the market which rose 3%. We received the largest portfolio contribution from the fund’s largest company, the IT company FPT Corp, which rose 6% during the month after the company’s report for the first 2 months of the year (the company reports preliminary results monthly) was well in line with the market’s expectations. The consumer conglomerate Mobile World also stood out with a rise of 10%. In the investor conference we attended at the end of February, the company showed optimism that the worst was now behind the company, which likely contributed to the rise.

In Kazakhstan (5% of the portfolio), our only position, the fintech company Kaspi, rose 23% during the month following its change of listing to NASDAQ and the release of a bullish report from one of the global brokerages. In connection with the listing, the company carried out a secondary offering, which significantly improved the liquidity in the stock. In its previously somewhat hidden listing in London, the stock traded an average of USD 3m/day over the past twelve months. In the last month, the stock traded USD 36m/day in the US. The higher liquidity puts the company on the radar also for larger funds. Kaspi has a relatively unique business model where the company, from its origins as a bank, has developed an ecosystem of e-commerce operations with integrated consumer credit and payment services that have led to superior profitability. Even after the re-rating, the share is valued at around 10x the annual profit. Its dominant market share in both payments and e-commerce in Kazakhstan makes the company unique and difficult to compare directly with other e-commerce companies, who generally are much less profitable but work in a wider geographical space. Expected profit growth of 20% and now more easily comparable with peers in the US and Latin America, means the company still looks attractive at current levels.

In Nigeria (3% of the portfolio), our sub-portfolio rose a whopping 48% during the month, compared to the market, which rose 39%. Three of our four banking positions (Access Co, Guaranty, and Zenith) all rose closer to 50% during the month, while Stanbic “only” rose 22%. The gain during the month was boosted by the fact that the Nigerian Naira strengthened by 15% against the US dollar. During the month, the authorities announced that they had now cleared all frozen payments in foreign currency, approximately USD 7 billion.

In Egypt (8% of the portfolio), the devaluation the market was waiting for finally took place, after the country at the end of February presented a significant investment commitment from the United Arab Emirates and reached a new agreement with the IMF. The currency initially fell from 30.8/USD to 50 but recovered towards the end of the month and closed the month at just over 47/USD. The equity market reacted positively but could not fully compensate for the weakening of the currency during the month. Our sub-portfolio fell 20% in USD, which gave a negative portfolio contribution of around 2%. However, the well-prepared package of measures backed by credible investors means that the situation is very reminiscent of the fall of 2016 when we first entered Egypt. That time was followed by a rise of around 100% (in USD) over the next 18 months. The situation ahead looks interesting.

PORTFOLIO COMPANIES’ PERFORMANCE

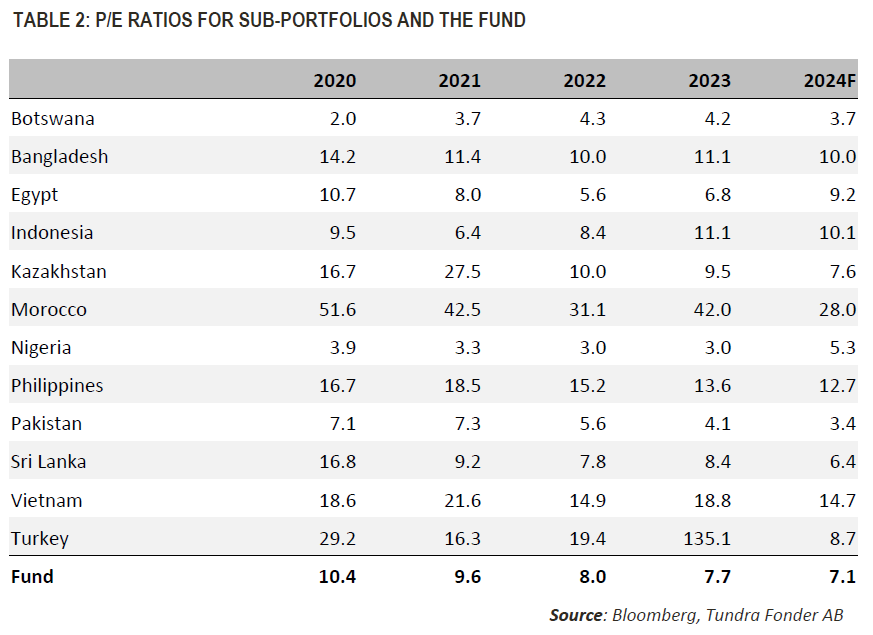

Looking at the valuation of the fund on a consolidated basis, we note that it is valued at 7.7x 2023 earnings, and 7.1x expected earnings for 2024. This compares to the same portfolio’s valuation at the end of 2020, which was 10.4x, and at the end of 2021, which was 9.6x

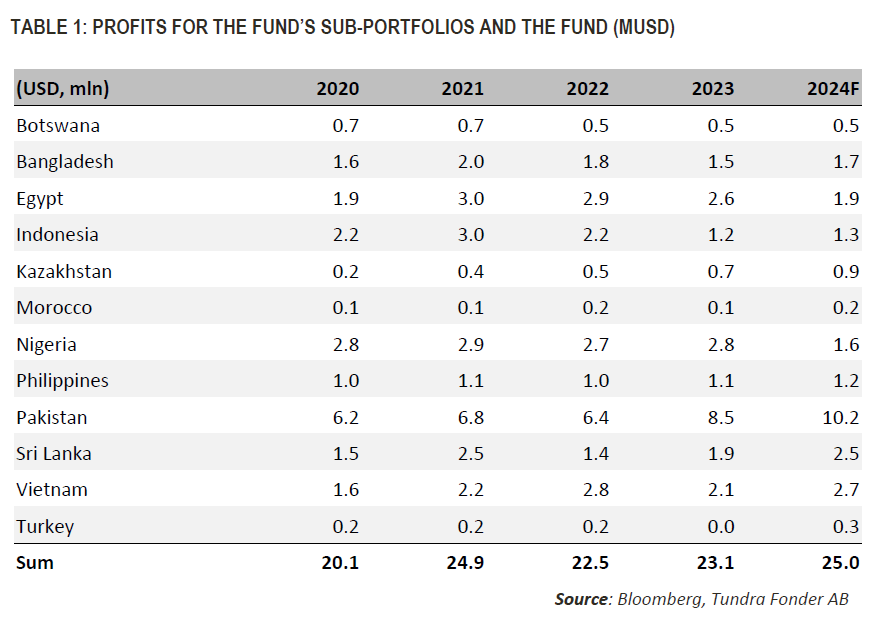

The fund’s thematic focus on what the World Bank describes as low-income and lower-middle-income countries has been perhaps the most difficult geographic area to invest in for equity investors over the past four years. Several of our countries (Sri Lanka, Pakistan, Bangladesh, Nigeria, and Egypt) have gone through the most severe crises they have seen in several decades. The investment climate has been likened to sailing through a storm, varying in strength, but with a constant threat of new storms on the horizon. Those who have followed our market letters can conclude that we have remained optimistic, even during more troubled times. This optimism is based on our expectations for our companies’ resilience and fundamental performance, which we believe the market has underestimated. When we look back at the profit development of our companies in recent years, we note that, as expected, as a group they have done very well during this turbulent period. However, investor concerns have meant that valuations have come down significantly. Based on profits generated in 2023, the fund would need to rise 30% to catch up with the average valuations from the end of 2020 and 2021. Based on profit forecasts for 2024, the fund would need to rise 40% to reach the same valuation. This of course requires more investors to enter our markets. A natural question is therefore to ask if there is reason to believe that this will happen? We think so. What we find is that the horizon in front of us right now is unusually free of immediate market-specific macro-economic, and political, concerns. We should expect a period where investors can focus more on the higher growth in our markets and our companies. The situation is very reminiscent of late 2011 when our markets had worked their way through the aftermath of the global financial crisis, and international investors gradually began to find their way back to our part of the world. We thus look forward to seeing what the remainder of 2024 will bring. Provided that no unexpected geopolitical events occur, a positive phase should be able to extend for several years to come. Dawn is approaching.

______________________________________________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.