WEAK MONTH BUT POSITIVE SIGNS AHEAD

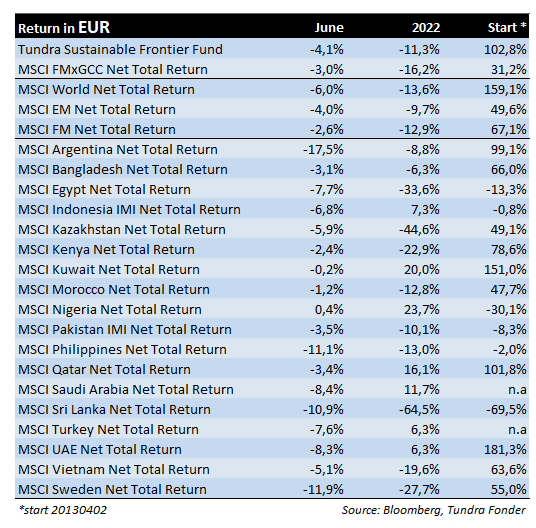

In USD the fund fell 6.8% in June (EUR: -4.1%), compared with MSCI FMxGCC Net TR (USD) which fell 5.7% (EUR: -3.0%) and MSCI EM Net TR (USD) which fell 6.6% (EUR: -4.0%). It was a weak month for global equities where the world index fell 9% (USD) and sentiment was sour across Tundra’s markets as well. The largest negative contributions were received from Pakistan (-1.6% portfolio contribution) where the sub-portfolio fell 8%, from Vietnam (-1.0% portfolio contribution) where the sub-portfolio fell 4%, Egypt (-0.7% portfolio contribution) where the sub-portfolio fell 12% and from the Philippines (-0.6% portfolio contribution) where the sub-portfolio fell 8%. We did not have positive contributions from any of our countries’ sub-portfolios during the month.

At the company level, our largest single positive portfolio contribution (+0.3%) came from Indonesian Hermina Hospitals, which is one of Indonesia’s leading private healthcare providers. The share rose 7% (USD) in a declining market after one of the largest conglomerates of Indonesia, Astra International, increased its holdings further, from 4.9% to 5.4%. Our largest negative contribution (- 0.7%) was received from Pakistan’s Meezan Bank. The share fell 16% in the month after the government raised corporate tax for Pakistani banks, from 35% to 39%, and introduced an additional super-tax of 10% for FY2022. The taxes are part of the budget concessions Pakistan has been forced to make in negotiations with the IMF. For Meezan Bank, the changes mean that the profit estimate for 2022 will be adjusted downwards by about 20%. Looking into 2023, it will affect estimates by around 7-9%. After the adjustments, the company is trading at 5x the annual profit for 2022 and about 4x for 2023. We, therefore, believe that it is well discounted in the share price. During the month we divested our remaining stake in Egyptian pharmaceutical distributor Ibnsina Pharma. The position has for a while been below 1% of the portfolio, which means we either have to increase, or divest. We concluded we lacked the conviction to increase versus our other holdings; therefore, we decided to divest. During the month we increased our position in Egyptian education company, CIRA, and Philippine consumer staples company Century Pacific Food Inc.

For global markets, the discussion is now beginning to focus on the risks of recession in the world economy, given the sharp rise in interest rates. It may sound scary, but global growth generally has a limited impact on our companies’ operations. They have suffered significantly more from the soaring commodity prices that have negatively impacted most of our countries’ balance of payments, driven up inflation and interest rates, and caused risk aversion towards equities. A global recession would mean lower demand for raw materials. This would in turn lower prices for raw materials which would impact the majority of our markets strongly positively. The balance of payments would improve, which would take pressure off currencies and inflation would come down, which would push interest rates back down. In June, we saw the first significant correction in commodity prices since the start of the war in Ukraine. Bloomberg’s commodity index fell 11%, touching the levels just before the war began. The decline was broad with double-digit declines for several important commodities. Leading futures for natural gas, wheat, zinc, and nickel stood out with corrections of almost 20%. Given the very sensitive supply and demand situation, one should be careful about drawing more far-reaching conclusions. And even if commodity prices now peak, inflation in our markets will also be affected by other factors, such as currency weakening, rising interest rates, and the phasing out of subsidies. Inflation in Pakistan rose to 21.3% year-on-year in June, primarily due to abolished fuel subsidies. Similarly, inflation in Sri Lanka jumped to 54.6% as the effects of the sharp devaluation were absorbed in prices. Countries’ conditions and historical handling of the crisis will mean that they will be affected differently.

The external situation remains difficult, but equity markets tend to anticipate events and their performance is primarily driven by changes in expectations – positive or negative. Among our markets, we note that the two hardest hit, Sri Lanka and Pakistan, are now closer to agreements with the IMF. The IMF visited Sri Lanka during the month and an agreement in principle on a support package is expected to be announced in July or August. A final agreement will depend on a successful restructuring of the country’s external debt. The debt restructuring should not be completed until the autumn at the earliest, and the country (and the equity market) can thus, with the help of the IMF, begin repairing the damage caused by the government. We find it difficult to see that expectations will deteriorate further, simply because they are so close to zero. In the case of Pakistan, very tough budgetary measures were taken during the month. An extra corporate tax of 10% for the just concluded financial year is introduced for most of the listed companies. The banks, which have been criticized for their prudent lending and for profiting from the high interest rates, saw their corporate tax increase from 35% to 39%. In combination with the elimination of fuel subsidies, the IMF should now be reasonably satisfied, which means that the debt program should be able to resume shortly. Even after this year’s (temporary) tax increase, the stock market’s valuation will be around 4x the current year’s profits, compared with just under 10x on average over the past ten years. It is very conservative given how far into the crisis we are.

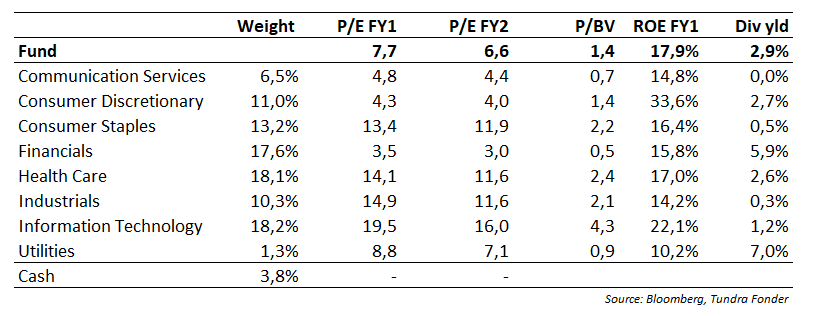

The headlines will continue to be dramatic for some time to come. As we have discussed in previous monthly letters, however, investors must try to ignore single years of difficult conditions. There is no other correct way to measure a company’s value than by calculating the net present value of estimated future cash flows. In such a model, the current year’s cash flow makes up approximately 10% of the company’s total value, assuming estimates beyond remain unchanged. If we embrace a truly pessimistic perspective and extrapolate the analysis to three years of zero cash flow, the valuation impact is about 25% of the company’s value. Assuming you own companies that can withstand this type of crisis without the business taking permanent damage, and that the long-term growth conditions remain intact, the market’s overreaction during turbulent times means a fantastic long-term buying opportunity. To quote Warren Buffett: “The stock market is a device for transferring money from the impatient to the patient ”. Our focus remains to try to ensure that our portfolio at all times reflects the absolute best long-term investment opportunities. The portfolio’s valuation is currently 7.7x the current year’s profits (see Figure 1). We will not be immune to developments in the rest of the world, but we are encouraged by the fact that our markets to a large extent have already discounted significantly worse times ahead.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.