A DIFFICULT START TO THE YEAR

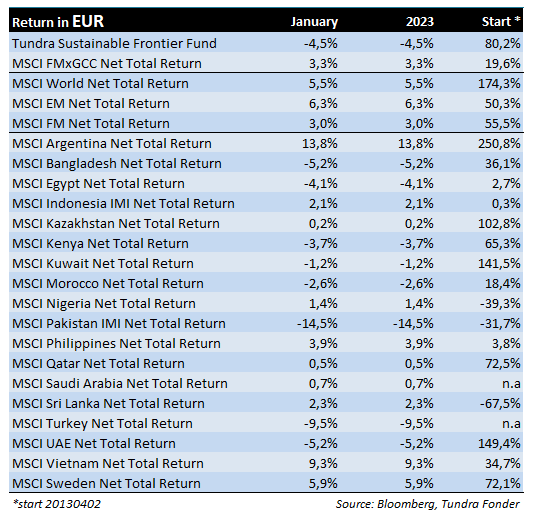

In USD the fund fell 3.1% (EUR: -4.5%), compared to the fund’s benchmark MSCI FMxGCC Net TR (USD) which rose 4.8% (EUR: +3.3%), and MSCI EM Net TR (USD) which rose 7.1% (EUR: +6.3%). The fund’s high Active Share is the reason for our high outperformance against the index over time, but there will also be months when it hurts. During the month the fund’s underperformance can be explained by three events: Our Pakistan sub-portfolio was down 20% in USD as the Rupee devalued by 15%. As a result, we lost around 3% in absolute returns and slightly more vs. the benchmark. Our Vietnamese sub-portfolio, which performed very well last year, did not keep up with the recovery in the Vietnamese stock market. Our sub-portfolio rose 6%, compared to the market which rose 9% – this cost us around 2% in return against the benchmark. Finally, our Egyptian sub-portfolio fell 14% during January against the backdrop of the country’s decision to devalue its currency by roughly 18%. As a result, we lost around 1.3% in absolute and relative performance.

Among positive contributors was the fund’s largest position, the Vietnamese IT company FPT, which stood out with a rise of 9%. Also worth noting was our smaller position in Sri Lanka’s Sampath Bank, which rose a whopping 28% after Sri Lanka moved closer to an agreement with its creditors in the ongoing debt restructuring.

Egypt devalued the currency by 18% during the month. In the case of Egypt, the current situation is difficult but relatively predictable. There is an existing dialogue with the IMF, and Egypt follows the main guidelines, especially regarding a floating exchange rate. More sensitive parts remain, such as increased privatization and reduced military/government involvement in the economy, but these are topics of discussion that the country has some time to deal with.

In Pakistan’s case, the current government was finally forced to give in to the IMF’s demands and float the currency, which meant a 15% devaluation during the month, while raising the policy rate another 1% (to 17%). A market-determined currency has been one of the demands of the IMF, and the recently announced hike in fuel prices is another. However, there are more difficult decisions to be made, which include the elimination of subsidies in the power market and increased taxation. That Pakistan and the IMF agree is a first, necessary, step. There is an aggravating factor in the fact that the current government enjoys minimal support among the population. With the upcoming election this autumn it means that the credibility vis-à-vis their creditors (the IMF, but also bilateral lenders) is rightly considered somewhat difficult to assess (will what is agreed upon also apply after the election?). Former Prime Minister Imran Khan’s party PTI would likely attain a majority should an election be held today. Even if Pakistan manages to reach an agreement with the IMF, an announced election date is thus likely to be required for investors to be willing to make a long-term commitment toward the equity market. Until then, the stock market remains difficult to assess.

When we put the crisis in a valuation context, we conclude that the current uncertainty is well discounted by the stock market. The P/E ratio (KSE100 index) is currently trading at 4.2x rolling twelve-month earnings, which can be compared to the ten-year average of 9.2x and the 5-year average of 8.0x. Correspondingly, the P/BV-valuation of the market is currently at 0.7x, which can be compared to the ten-year average of 1.4x and the five-year average of 1.1x. In strategy reports issued by global brokerage firms looking into 2023, Pakistan is generally considered uninvestable, for good reason, given the prevailing uncertainty. If we were to put on our most pessimistic lenses and assume that the country is unable to deal with the ongoing crisis, the economy grinds to a halt resulting in all corporate profits being erased for 2023, one should remember that current annual profits (e.g. cash-flows) make up around 10-12% of a company’s value – less than the market decline so far this year. If we extend the halt for another year i.e., a two-year elimination of all profits, we end up with just over 20% fundamentally justified decline, decently in line with the market performance so far. One must have great humility for the short-term movements of the market given prevailing uncertainty, but also be aware that current values require that the country not only fall flat on its stomach but also stay down for several years.

In Bangladesh, an agreement was reached with the IMF regarding a financial support program of USD 4.7 billion, which is positive. As part of the agreement, Bangladesh has, among other things, committed to introducing a banking emergency to restructure bad loans in the banking sector and agreed to a market-determined currency. The Bangladesh agreement was implemented from a stronger economic backdrop and should be seen as more preventive than urgent, an important difference to the situation in Pakistan.

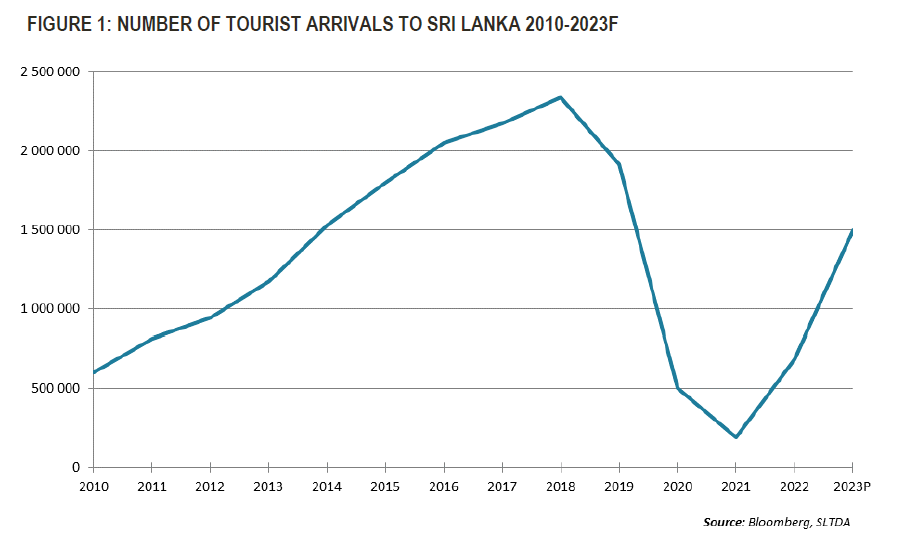

In Sri Lanka, India has now expressed its support for a debt restructuring. Sri Lanka is now waiting for the country’s most important lender, China, to take a positive stance, which opens up an agreement with the IMF and an opportunity for Sri Lanka to look forward again. During the month, the central bank decided to leave the policy rate unchanged. Tourism is now starting to get going again in earnest. During January, 102,000 tourists arrived, 24% more than the corresponding month in 2022. For 2023, the forecast from the SLTDA (Sri Lanka Tourism Development Authority) is currently about 1.5 million tourists, which can be compared to the best year so far (2018), when 2.5 million tourists visited the country and the worst year (2021) when only 200 000 million arrived. If we only compare the January figure with the peak years of 2018 and 2019 (before the Easter attack) it indicates a somewhat lower number for 2023, (1-1.2 million).

Sri Lanka’s tourism revenue has been a major source of income for the country since the end of the civil war in mid-2009 and the number of arrivals steadily increased until the spring of 2019. Then the country was first hit by the horrific Easter attack, followed by COVID-19, shutting down from April 2020 to the end of 2021, and then followed by domestic unrest that forced the president to resign.

We, who have visited the country several times and consider it to be one of the world’s most interesting destinations, have no doubts whatsoever that within a couple of years, the country will pass the previous top listing from 2018. Historically, the average income per arriving tourist is approx. USD 1,800. If SLTDA ‘s forecast for 2023 turns out to be correct, it thus means a revenue of approx. USD 2.7 billion for the year (barely 4% of GDP), which should increase in the years thereafter. Sri Lanka is a country located next door to one of the world’s most important economic zones (India). During the last 4 years, the country was hit by two disastrous events (Easter attacks and COVID-19), fully exposing its most pronounced vulnerability (high FX-denominated debt). With these issues now being addressed/improved the country has a good chance to re-enter its long- term trajectory forward.

In Vietnam, the president had to resign in January in the aftermath of the corruption scandal we discussed in previous monthly letters. The incident had limited impact given his relatively insignificant role in the country’s politics. However, there is some uncertainty about whether this is the end of the corruption scandal, or more is to be expected, which in the short term remains a risk for the country. We are also somewhat concerned that the resulting problems in the credit market short-term can hurt private consumption.

In February, the reporting season begins, but already in the last days of January, just under a third of the portfolio (calculated as a percentage of fund assets) reported.

The fund’s largest holding, Vietnamese IT company FPT (9% of the fund), increased its turnover by 22% and profit after tax by 23% for the full year. The result came in just below expectations due to a weaker yen (Japan accounts for 40% of the company’s IT exports), where the company took a hit during the fourth The company is trading at 16x the just-ended year’s earnings, and consensus currently expects earnings growth of 20% for 2023.

The fund’s third largest holding, Vietnamese REE Corp (8% of the fund), which expands mainly in renewable energy, increased turnover by 61%, and profit after tax increased by 45%. The result was slightly higher than expected due to strong performance for the contracting business. This line of business includes the construction of solar-energy facilities. The company is trading at 11x the just- ended year’s profit. In 2023, profits are expected to fall 12% on the back of a normalization in profits for hydropower operations after 2022 was unusually favorable with high water

Our two companies with a focus on Vietnamese consumers operated under more difficult Masan Group’s (3% of the fund) results came in slightly below expectations. Adjusted for the disposal of its animal feed business at the end of 2021, revenue rose 3% year-on- year, while like-for-like profit grew marginally. More cautious Vietnamese consumers meant lower purchases per basket in the company’s food business and some restraint in demand for their food products as well. The company is valued at 40x the just-ended year’s profit and is expected to increase profit by roughly 35% in 2023 in line with the continued expansion of the company’s food chain and normalization of margins. Mobile World (3% of the fund), which operates both electronics chains (approx. 70% of turnover) and food trade (approx. 25%), noted a decreasing purchasing power among consumers, which led to larger discounts and falling margins. The company’s sales rose 8% for the full year, while profit after tax fell 16%. The company is valued at 15x the just-ended year’s earnings and is expected to increase earnings by 27% in 2023. Both Masan and Mobile World noted deterioration towards the end of the year, which means there is a risk that the forecasts for 2023 may need to be slightly adjusted down.

Our Bangladeshi pharmaceutical company Square Pharma (8% of the fund) released its half-yearly report (the company’s fiscal year ends in June). Both turnover and profit rose 10% year-on-year, which was slightly above However, we should see a certain deterioration in profitability in the coming six months, given the impact of the weakening of the Bangladeshi Taka in recent months (higher costs of imported raw materials). The stock trades at just under 10x earnings for the just-ended calendar year and is expected to show earnings growth of 9% for the next twelve months.

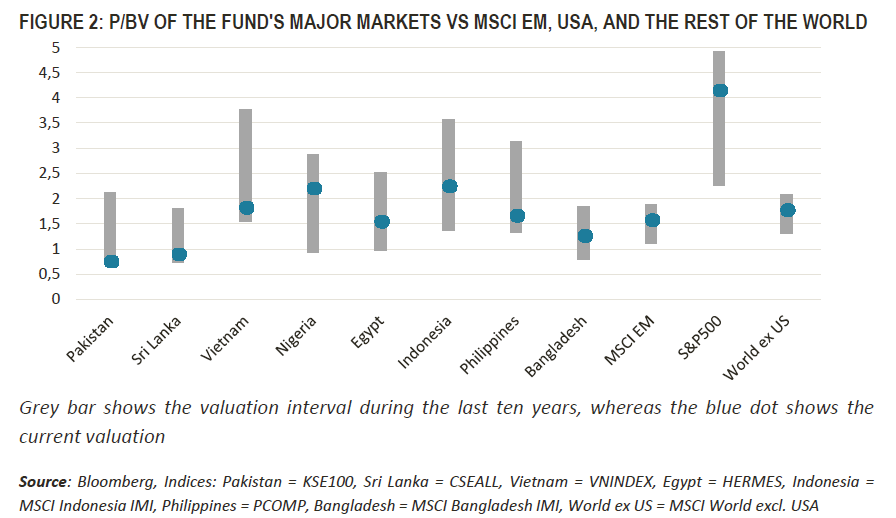

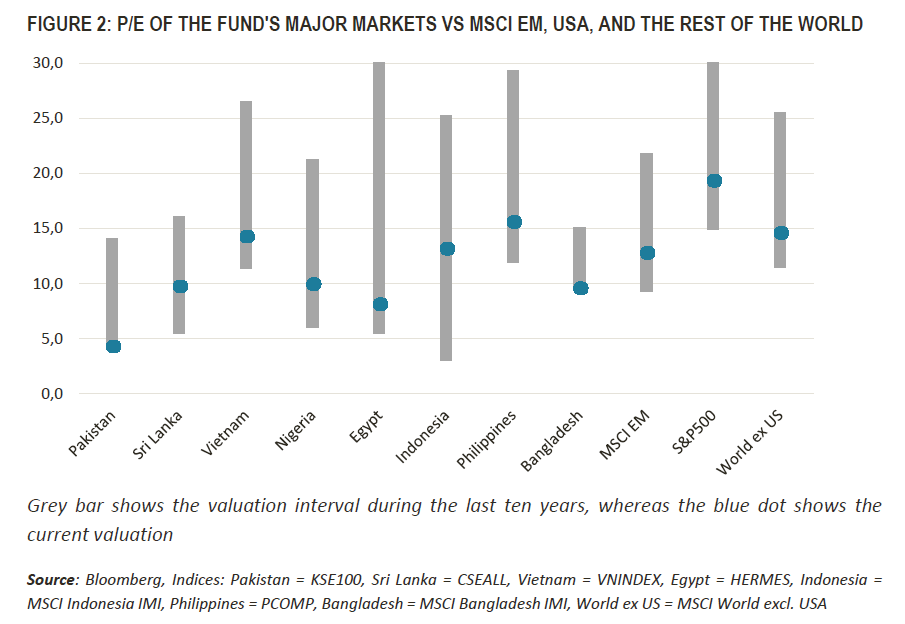

The events in Pakistan and Egypt during January mean two very expected negative events have now unfolded, clearing the path forward somewhat. Yet our markets have another couple of tough months ahead and equity markets will remain volatile waiting for us to move past the worst. The short-term market uncertainty must however be set against valuations, where our most vulnerable markets seem to have priced in very negative scenarios more than sufficiently (see Figure 2 and Figure 3), although still lacking a trigger for revaluations.

In this market climate, our focus remains on the fundamentals of individual companies with a focus on making full use of the opportunities that surface during troubled times.

______________________________________________________________________

TUNDRA SUSTAINABLE FRONTIER FUND REPLACES THE SWAN WITH THE EU’S REGULATIONS FOR SUSTAINABILITY

In connection with the new EU regulation under the Sustainable Finance Disclosure Regulation (SFDR), new requirements are applied to funds’ sustainability work as of March 2021. Tundra has therefore decided on July 4 not to continue with the Nordic Ecolabelling of the fund. According to the new regulations, sustainability reporting must take place in a uniform manner and funds are divided into different categories. The Tundra Sustainable Frontier Fund is classified as an Article 8 fund (Light green: promotes environmental or social characteristics). The investment philosophy of the fund remains the same; management of the fund and is not affected by the change.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.