THE FUND:

The fund fell 5.2% in December, compared to the fund’s benchmark index MSCI FMxGCC Net TR (SEK), which fell 5.9% and MSCI EM Net TR (SEK), which fell 4.6%. Positive contributions accrued from the underweight in Argentina (1.3%), an absence of holdings in Romania (1.2%), stock selection in Vietnam (0.9%), and the absence of holdings in Kenya (0.6%). Pakistan (-2.3%), Turkey (-0.8%), and Sri Lanka (-0.5%) were the largest negative contributers. Egypt (0.2%) was the only market to make a positive absolute contribution during the month. Few transactions were conducted during the month. However, we sold our entire position in John Keells Holdings, a Sri Lankan conglomerate. The share has performed strongly since the start of the political turbulence in Sri Lanka and we note that given the relative valuation of other potential investments, competition has pushed it out.

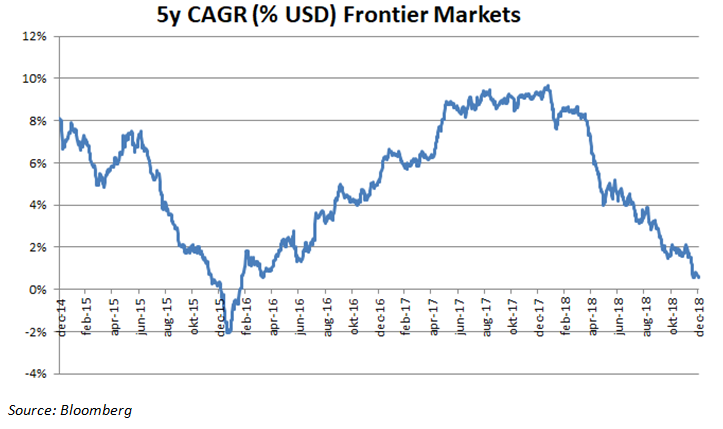

For the year as a whole, the fund fell 7.9%, compared to MSCI FMxGCC Net TR (SEK), which fell 17.5% and MSCI EM Net TR (SEK), which fell 7.1%. Our decision to completely exclude the largest index market, Argentina, at the time added about 14% outperformance during the year. Stock selection in Egypt added just under 4% outperformance, and the position we took in Turkey in September added 0.7%. Among negative contributions, Sri Lanka and Pakistan were the two main underperformers (costing 2.4% each) but our stock selection in Vietnam (-1.1%) also contributed negatively. We cannot say that we are satisfied after a year of negative returns. However, given the market conditions, we are pleased to have retained such a large share of our unitholders’ investment during what we consider to be some of the toughest market conditions since the financial crisis in 2008.

MARKET:

MSCI FMxGCC Net TR (SEK) fell 5.9% during the month, compared to MSCI FM Net TR (SEK), which fell 5.0% and MSCI EM Net TR (SEK), which fell 4.6%. The stronger Swedish krona lowered the return by about 1.5% during the month. We note that none of the largest markets showed positive returns in SEK. Romania fell just under 18% on a new tax proposal that would mainly hit the banking sector’s profits. Nigeria (-1.9%) performed better than the benchmark after the state’s lawsuit including fines against the telecom giant MTN was re-negotiated and settled amicably.

In 2018, the development was very weak, with a decline of 17.5% during the year. Argentina was the main culprit crashing 48% during the year. Of the larger markets outside the Middle East, only Romania (+11.5%) rose noticeably.

Looking at the broader frontier index MSCI FM Net TR, which includes the Middle East, we conclude that it performed significantly better during the year (-9.2% vs -17.5% ex-gulf). The primary reason was the rise of, what is now, the largest index market Kuwait (19%) which rose 26% during 2018. The Middle East escaped the concerns of most other frontier markets regarding trade wars and currency devaluations. However, we do not think that the region will belong to the winners circle when the stock market climate is slightly less pessimistic for the smaller emerging markets and frontier markets.

OUTLOOK FOR 2019:

After a weak 2018 we think 2019 looks very interesting:

There are, of course, plenty of concerns left, some of which are difficult to assess accurately. The ability to predict how President Trump acts from here on remains low and thus the risk of more significant damage to the world economy remains intact. Given what has been priced into our markets, we note that from our vantage point we anticipate that the risks to our markets come from significant unexpected movements in global stock markets. While the sentiment towards emerging and frontier markets is weak at present, there are possibilities too. The adjustment we have seen, not only this year but during the last five years, is extremely unusual. Even if we see further dips before the recovery gets a firm footing we already know that this is a good time to add long term exposure to emerging and frontier markets for investors who share our long term investment approach.

ESG ENGAGEMENT:

Sri Lanka’s John Keells Holdings was divested in December due to financial considerations. No new companies were added to the fund this month.

DISCLAIMER:

Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is ACOLIN Fund Service AG, Affolternstrasse 56, CH-8050 Zurich, whilst the Paying Agent is Bank Vontobel Ltd, Gotthardstrasse 43, CH-8002 Zurich. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.

Kundgrupp / Investortype:

* Ontario and Quebec