STRONG HALF-YEARLY REPORTS DROVE THE FUND TO A NEW ALL-TIME HIGH

In USD the fund rose 1.9% (EUR: +2.5%) during the month, compared to MSCI FMxGCC Net TR (USD) which rose 2.3% (EUR: +2.8%), and MSCI EM Net TR (USD) which rose 2.6% (EUR: +3.2%). About half of the absolute return was generated in Pakistan, where our two largest holdings, the IT company Systems Ltd and Meezan Bank, rose 11% and 21% in USD respectively after strong half-year reports. No single market stood out negatively during the month. Negative contributions during the month were received from our positions in NBP and AGP in Pakistan, which fell 6% and 8% respectively. We also noted a decline in Bangladeshi Active Fine Chemicals which fell 11% during the month.

Good contributions were received from Vietnam, where one of our larger holdings, Vietnam’s largest listed company in environmental technology and renewable energy, REE Corporation rose 21% after a period of consolidation. A good positive contribution was also received from the Indonesian media conglomerate Media Nusantara (MNCN), which rose 13% after a strong half-year report. During the month, we increased our position in MNCN from approximately 2% to just over 4% as we believe that the company deserves a revaluation. With its base in the traditional TV industry and as a content provider, the business is gradually being transformed into digital media. Digital revenues amounted to almost 20% of total revenues during the second quarter after growth of about 170% on an annual basis. At the end of August, the company also announced that it will resume the dividend which was cancelled in 2020. Given the growing share of digital revenue where online gaming will be added during the autumn, we believe the market’s view of the company will change in the future. MNCN is today valued at just over 5x the annual profit, which in our eyes is a gross underestimation of future potential.

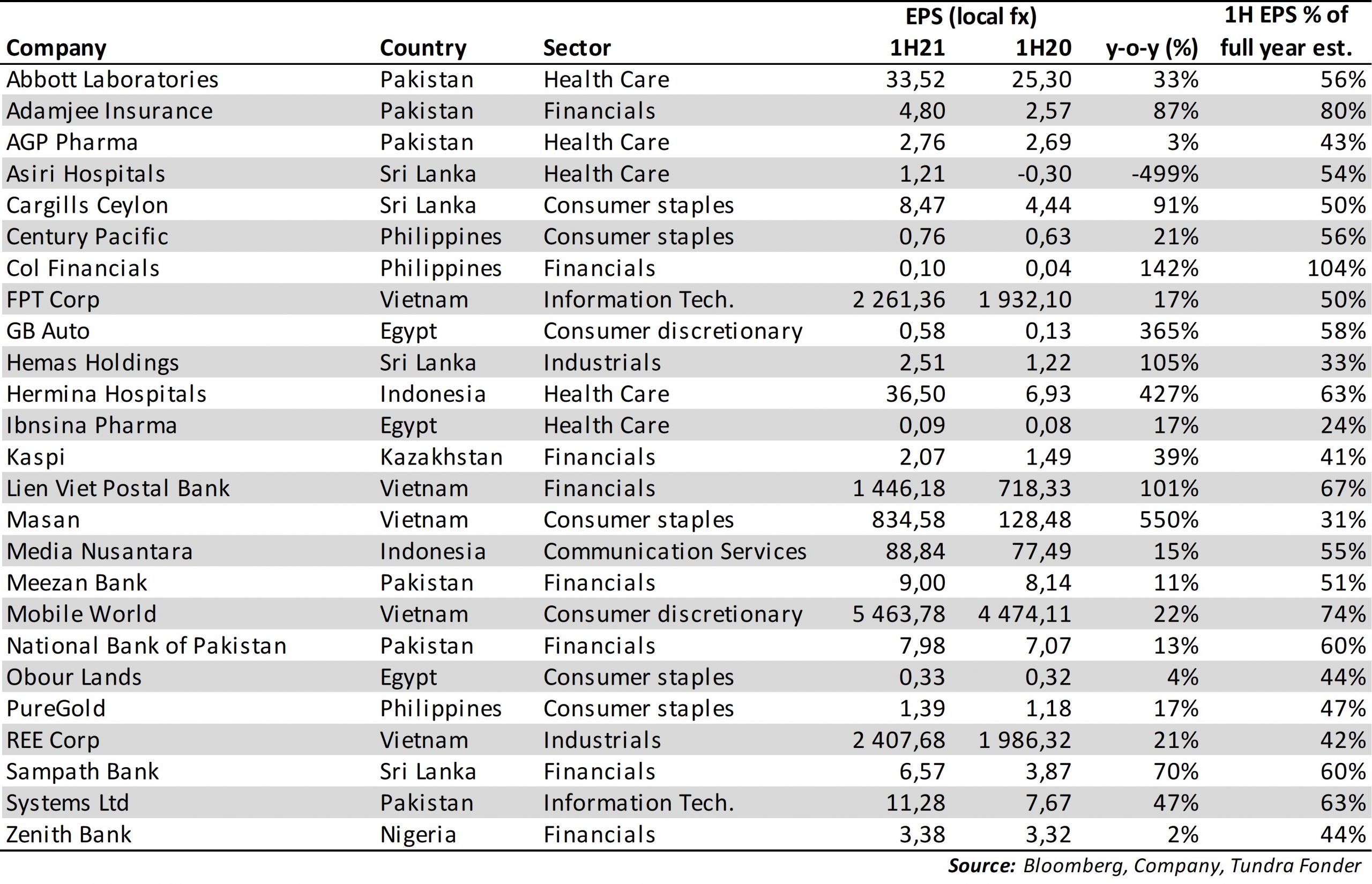

The majority of our portfolio companies (73% of the fund’s assets) have now reported their results for the second quarter (calendar year) (see Table 1 on previous page). We note that the reports, just as in the first quarter, indicate that our portfolio companies are slightly ahead of the profit forecasts for the full year (54% of the full-year estimate portfolio weighted). If nothing unexpected happens, we should thus see some upward adjustments in earnings estimates for the coming quarters, something that is normally positive for share prices. The average valuation in the fund (Harmonic P/E) is currently 10.4x for the current year.

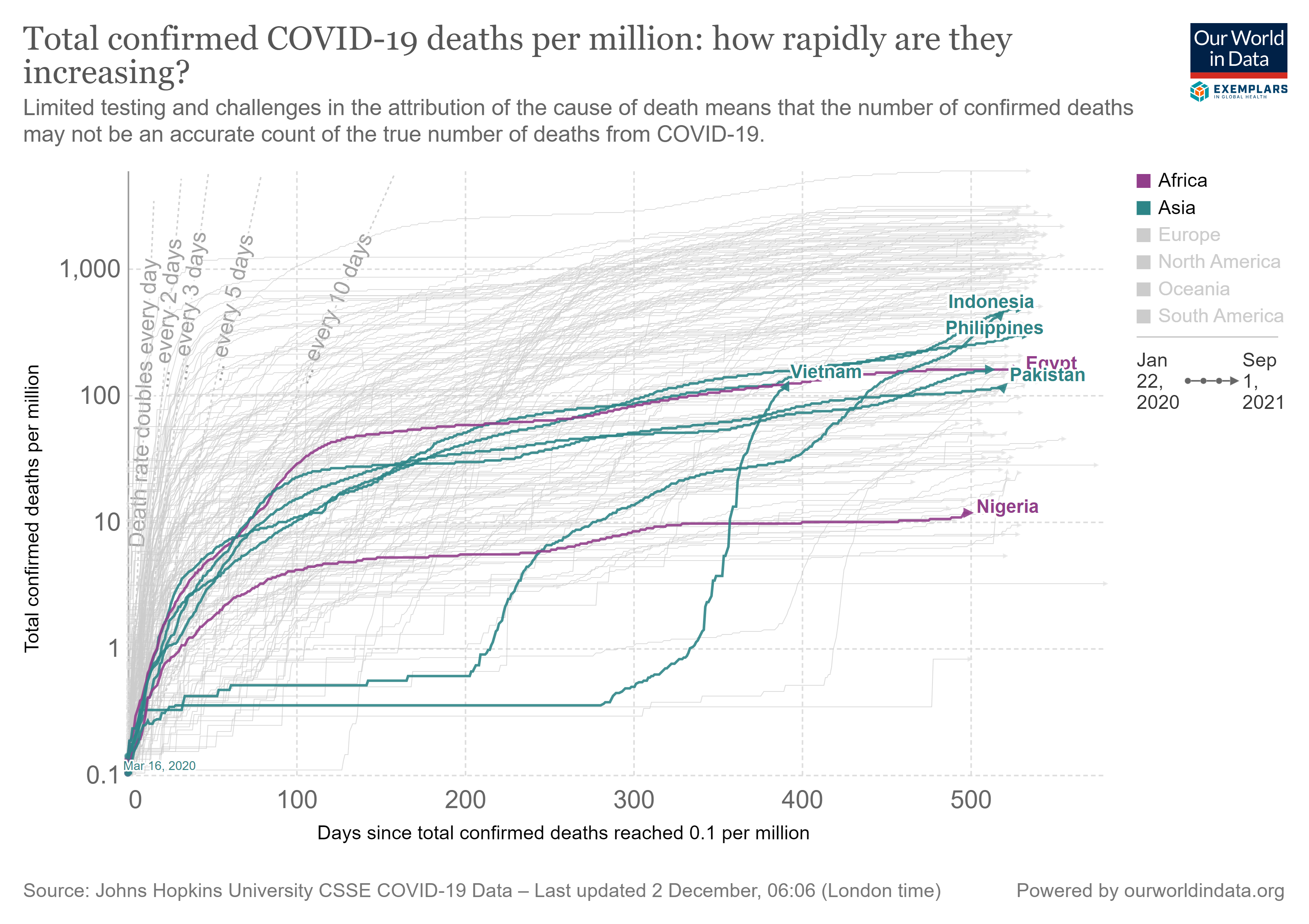

With the exception of Sri Lanka, the vaccination rate (defined as the proportion of the population who have received at least one dose of vaccine) is still low in our markets (see graph 1). This means that all our countries continue with selective counter-measures depending on the current rate of infection. Vietnam, which for long managed to keep the proportion of infected people down, has unfortunately been hit the hardest in recent times. Measured in the number of reported deaths (with emphasis on “reported”) as a proportion of the population, they have now caught up with several of our other markets (see graph 2). From 23 August, people in Ho Chi Minh City are prohibited from leaving their homes until September 6. Our colleague Chau, who is on-site, says that in her area, the system has worked well so far. She and her neighbours have continuously received the necessary deliveries of food and drink delivered to their homes. The very harsh measures however had very little impact on the equity market which rose 2% during the month.

After 20 years of war, the Taliban took power in Afghanistan in August. In the comments following the abrupt end, we note a large dose of criticism of the former Afghan regime, which, despite significantly greater military resources, both in number of soldiers and in the arsenal, made only limited resistance. A large dose of criticism, including self-criticism, was levelled at the United States for how the strategy was set up and the limited benefit it ultimately led to. We saw a risk that Pakistan would be blamed, given that the country has historically been accused for not doing enough to help the allies in Afghanistan and also from time to time have been accused of actively supporting the Taliban. We note that this criticism has largely been absent and has instead been replaced by a more nuanced picture that includes a greater understanding of the difficulties of controlling 1.5 million Afghan refugees on Pakistani soil, but also the strong link between 70 million Pashtuns in Afghanistan and Pakistan, with a relatively high share of illiteracy, and who often have stronger ties within their group than the nation whose borders they are currently within. Despite the Taliban’s stated commitments to a more equal society, there is every reason to be concerned about women’s and girls’ rights in Afghanistan in the future and thus for Afghanistan’s economy to recover. Furthermore, the question remains whether the Taliban, which consists of a large number of groups, can cooperate now that the external enemy is gone. Nor does the Taliban’s takeover mean that the risk of terrorist attacks disappears. Their arch-enemy ISIS showed this quite immediately in the terrible attack on Kabul airport. However, the best way to counter extremism is economic prosperity, not weapons. There is nothing more dangerous than people who have nothing to lose and who lack the opportunity (literacy) to take alternative worldviews. Provided there is now peace in Afghanistan it could mean a major boost for all of Central Asia, including Pakistan, which has lost 70,000 people and estimates the cost of its economy at nearly USD 150 billion (50% of current GDP) since the war began in October 2001.

On September 7, MSCI will announce whether Pakistan will be moved back to the MSCI frontier index. The probability of this happening this time is high and in that case, the change will take place in November. The initial flows are seldom market-influencing and should not be this time either. However, we consider a possible change of category to be positive for the market as Pakistan’s low weight in the Emerging Markets index has meant that it has been largely ignored. The initial weight in the MSCI Frontier Index should be just over 2%, but given the market’s liquidity and the attractive valuations, we believe active funds will have a higher weight than that. For the MSCI Frontier Index, it would be very positive to bring in the world’s fifth-largest country, which also provides a dynamic and liquid stock market.

Frontier markets and smaller emerging markets have received a well-deserved boost over the past twelve months, reminding investors that over time it is worth investing also outside the largest emerging markets. Not least, the positive aspects of diversifying your emerging market portfolio into frontier/smaller emerging markets have appeared in 2021, when the frontier category so far has outperformed the Emerging Markets category. Low valuations and good profit growth indicate that we are still early in a possible revaluation process.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.