THE FUND

The fund rose 0.7% in September, which was significantly less than the benchmark index MSCI Pakistan IMI Net TR (SEK), which rose 8.1%. Our underweights in the energy and fertilizer sector partly explained the underperformance. Another explanation was the fund’s exit from the Pension Swedish Pension Authority’s platform (PPM), where a significant part of the fund’s assets was divested in a rising market. A more thorough explanation of the overall changes in the Swedish PPM system can be found here: https://www.investmenteurope.net/news/4002399/funds-removed-sweden-ppm-platform). With the exit completed at the end of the month, we anticipate more favourable conditions to again start generating alpha in what we believe will be one of the most interesting emerging and frontier markets over the next 5 years.

MARKET

MSCI Pakistan IMI Net TR (SEK) rose 8.1% during the month, compared to MSCI FMxGCC Net TR (SEK) which rose 0.4% and MSCI EMF Net TR (SEK), which rose 2.0%. Falling bond yields (10-year interest rates fell by 70 basis points to 12.1%) and declining sales flows from the year’s biggest seller, local mutual funds, may be seen as the main explanations for this. We note an increased interest in the equity market, not due to optimism about rising profits in the short term, but rather the realization that we may have seen the worst in terms of falling demand and increased financial costs. The policy rate was left unchanged at 13.25%. After inflation for September reached (with the new inflation basket) 11.4%, it is likely that within the next 2-3 months we will see inflation gradually fall below 10%. This should open up expectations of a lower policy rate sometime in the first half of 2020.

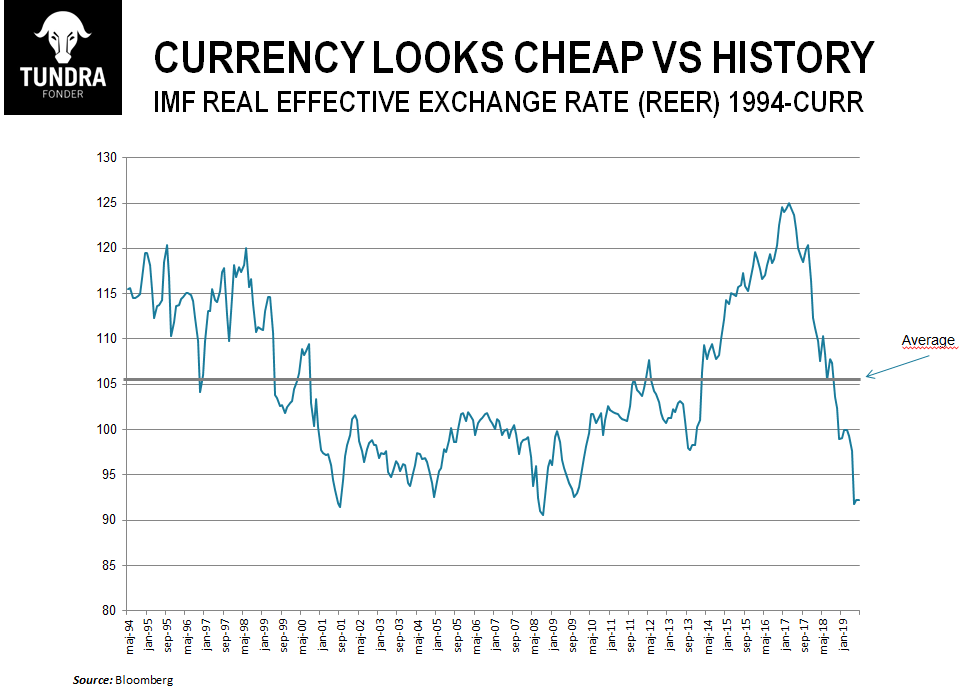

Further on, in September we saw foreign inflows of USD 242m to the local fixed income market. The amount may sound small but can be compared to USD 70m in August and USD 10m in July. Prior to that, the flows were close to zero for two years. This indicates increased confidence in the Pakistani rupee among foreign investors. It is reasonable to assume that the currency, based on IMF’s definition of real effective exchange rate (REER), is close to the cheapest levels we have seen in the last 25 years (see graph). The inflow into the fixed income market during September was about 40% of the current account deficit during the month of August. Pakistan’s current account deficit has already fallen substantially to levels around 2-3% of GDP on an annual basis. Signs that portfolio investments can help bridge the remaining gap would instil optimism about the Pakistani rupee. It is worth following the development of both portfolio investments and direct investments going forward. In the current climate, even smaller changes might matter.

Prime Minister Imran Khan made an emotional speech to the UN General Assembly (UNGA), calling on the UN to draw greater attention to the situation in Kashmir. Communication routes in the Indian part of Kashmir remain closed as it has been for the last 2 months after India shut down the internet and telephony in the region. As we said earlier, there is a significant risk of unrest in Kashmir when India decides to open up the communication routes. India may blame such unrest on Pakistan, which could lead to certain military confrontation. This risk might occasionally cause concerns in the stock markets in both Pakistan and India over the coming months. However, we continue to assess the likelihood of a full-scale war very limited given the negative implications this would have for both countries. In the meeting that will take place October 13-18 meeting, FATF will decide on further possible action against Pakistan regarding pointed deficiencies in money laundering and terrorist financing. It is most likely that Pakistan will remain under enhanced surveillance (so-called gray list) and be asked to continue its work to mitigate the risks in these areas. Pakistan claims that India has been lobbying a great deal to try to get Pakistan blacklisted (like Iran and North Korea). However, it is enough that 3 of the 39 member organizations block such a decision. Given that the member states China, Malaysia and Turkey have clearly made a stand on Pakistan’s side in the FATF, and that Saudi Arabia and the Gulf countries probably will oppose such action also, we see the probability of blacklisting as very low. It is almost equally unlikely that Pakistan will be removed from the “gray list” as this requires 15-16 votes. We note that the new government openly and actively has tried to show progress on identified issues, but we believe that there is significantly more work to be done and explained.

The stock market is still trading close to ten-year lows measured as P/BV, expectations in the most vulnerable sectors (such as cement, steel and vehicle assemblers) appear realistic, and we therefore expect that early August probably marked the lows in this bear cycle. In the short term, inflation and current account figures become the most important macro indicators. In terms of flows, the greatest interest will be attached to the actions of foreign investors and local mutual funds. Developments in Kashmir and the outcome of the FATF meeting will also be closely monitored.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.