SLOW MONTH ACROSS THE PORTFOLIO

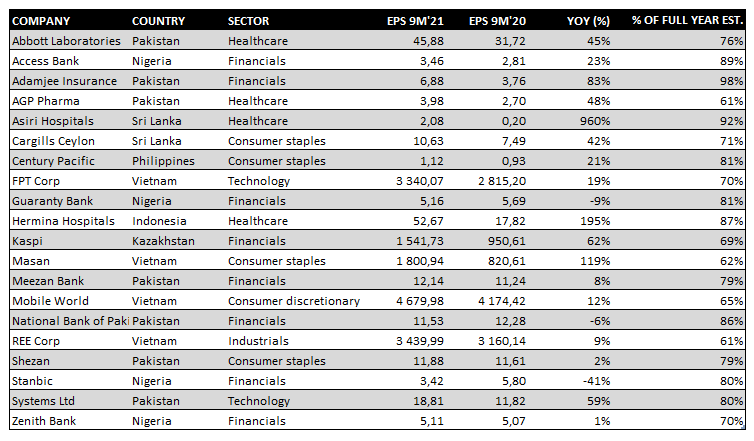

In USD the fund rose 1.7% during the month (EUR: +1.4%), compared to MSCI FMxGCC Net TR (USD) which rose 4.1% (EUR: +3.8%) and MSCI EM Net TR (USD) which rose 1.0% (EUR: +0.7%). Performance was dragged down by corrections in several of our larger, and best, positions so far this year. Measured in absolute return, it was primarily our holdings in Bangladesh and Pakistan that had a negative impact during the month. Our two largest holdings in Pakistan, Systems Ltd and Meezan Bank, fell 6% and 4% respectively during the month, resulting in negative portfolio-level contributions of 0.5% and 0.2%, respectively. Our largest position in Bangladesh, Square Pharmaceuticals, fell 10% during the month, making a negative contribution at the portfolio level of 0.8%. All three companies reported their results during the month which were in line with, or slightly above, market expectations (see summary of the quarterly reports below). In the case of Systems and Meezan, the declines should be seen against the background that both shares have been significantly stronger than their home market so far this year (Systems +69%, Meezan +41% vs MSCI Pakistan IMI Net TR (USD) -4.0%) and thus affected by profit-taking. In Square Pharmaceuticals’ case, we observed a major institutional seller during the month who gradually pushed the stock downwards. We increased our position in Square Pharma following the quarterly results, which was slightly better than our expectations.

A rather weak month was alleviated by our position in the Kazakh fintech company Kaspi, which rose 37% and thus made a positive contribution of just over 1% at portfolio level. Our increase in the position at the end of September thus proved successful in the short term. Another positive contribution during the month was Indonesian Media Nusantara, which rose 8% and made a positive contribution of 0.4% at portfolio level. During the month, we sold our marginal remaining position in Vietnamese Lien Viet Postal Bank (0.3%), where the majority of the holding was sold earlier this year.

Measured as share of the portfolio, 55% of our holdings have now reported third quarter earnings for (calendar year) 2021. The reports show that the earnings estimates for the portfolio as a whole are well substantiated, with a probable need for certain upwards adjustments. It should be pointed out that differences in fiscal years mean that the full-year estimates for some of the companies do not coincide with the calendar year 2021. Overall, however, the trend is strong.

Some of the companies, e.g. REE Corp (Renewable Energy in Vietnam) and AGP Pharma (Pharmaceuticals in Pakistan) have been hit by what we consider to be short-term, but explanatory, disruptions. In AGP’s case, it is about canceled exports to Afghanistan and a negative impact from the weaker rupee. In the case of REE Corp., it was affected by the shutdowns in Vietnam during the third quarter as well as certain short-term disruptions in power operations. In two of our five largest holdings, Systems and Meezan, we see probably upwards earnings adjustments ahead. In one case, Sri Lankan Asiri Hospitals, a rather significant upward adjustment is needed. In Asiri’s case, however, it should be added that the company’s results during the third quarter were positively impacted by COVID-related revenue.

For the consolidated portfolio, we see upward adjustments in estimated earnings for the current year but also some spillover to next year. On this backdrop, the portfolio’s P/ E-ratio (harmonic P/E-method) of 10.1x for the current year and 8.5x for next year remains conservative. As we usually point out, the stable growth that characterizes our holdings and the lack of traditional cyclical industries means that the probability of an external impact on results is generally low. Instead, it is about the companies succeeding in maintaining a continued high level of their delivery, which is more about the long-term strategy and its execution.

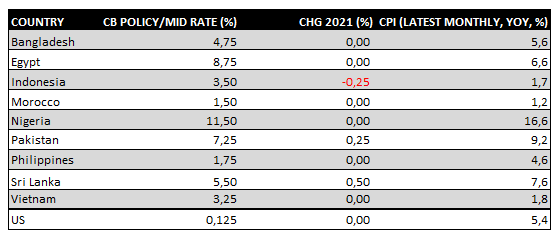

Regarding the general investment climate, it is worth noting that our markets are also affected by the global inflation discussion. We have seen clearly higher inflation over several of our markets in the wake of rising commodity prices and as a consequence of inadequate logistics. However, it is also worth noting that the upward jump has been more modest, and less of the shock we found in e.g. the US (see Figure 1). Less impact of rising shipping prices may be one reason. Another reason may be lower purchasing power and greater focus on simpler basic goods that are to a greater extent manufactured locally.

We also note that several of our countries’ central banks have already begun to act on the higher inflationary pressure. In fact, none of our investment countries at present (Nigeria, in reality, however the same) has a larger gap between inflation and the current policy rate than the United States (see Table 2).

If it turns out that the world is facing a period of more persistently higher inflation, then our thesis is that this outcome will have less impact on our markets, than e.g. the US. Combined with the currently low valuations, it is a good argument for investors who see a risk of longer-term higher inflation.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.