STRONG STOCK SELECTION HELPED THE FUND IN NOVEMBER

In USD the fund fell 0.8% during the month (EUR: +1.4%), compared to MSCI FMxGCC Net TR (USD) which fell 4.4% (EUR: -2.3%). Despite a weak month in Pakistan (the market fell 4% preceding MSCI’s reclassification of Pakistan from Emerging Markets to the Frontier Markets category), we received our two best contributions from Pakistan.

Our largest holding, the IT company Systems Ltd (9% of the portfolio), recovered after the decline in October with an increase of 14%. The company benefits from a weaker Pakistani rupee given that more than 80% of revenues come from abroad. The increase was partly strengthened by the fact that the Bill & Melinda Gates Foundation invested in the company’s subsidiary in mobile payments. Our second largest holding in Pakistan, Meezan Bank (6% of the portfolio) rose 9%. In Meezan’s case, they benefit from rising interest rates, which have a positive effect on net interest income. Both companies are good examples of Tundra’s motto that stock selection over time is significantly more important than country selection. Our smaller position in Bangladeshi Brac Bank rose 17% after Japanese Softbank announced an investment in the company’s mobile payment business bKash. Among our negative contributions was the Kazakh fintech company Kaspi, which fell 10% after the strong performance in October. We also experienced a correction of 16% in our Indonesian hospital group Hermina Hospitals, after a strong performance so far in 2021.

During the month, we sold two of our smaller positions in Egypt, the cheese producer Obour Land and the pharmaceutical company Eipico. Both positions have for some time accounted for less than 1% each of the fund’s assets and were therefore under evaluation to either be increased or sold. We did not have a strong enough conviction relative to our other positions and thus chose to sell. No new positions were added during the month.

During the month, concerns about rising inflation continued in the wake of higher commodity prices. The State Bank of Pakistan acted by raising the key interest rate by 1.5%-points, to 8.75%. Pakistan’s difficulties during the year have gone unnoticed by our unitholders as our country portfolio has risen by more than 30% during the year thanks to good stock selection, while MSCI’s country index is down 10%. However, the country has been hit hard by rising commodity prices, which have had an impact both on a deteriorating current account, with a subsequent effect on the currency, and on inflation statistics. The market expects at least one further sharp rise in the policy rate. The auction of 1-year bonds on 1 December, the interest rate was set at 11.35%, which gives an indication of what the market currently expects from the central bank in the coming year. The market situation is interesting. Under Imran Khan’s PTI, Pakistan is undergoing a very comprehensive reform process with focus on transparency and increased international competitiveness, which we believe is very positive for the country’s long-term outlook. But in the short term, it has been hit hard by the sharp rise in commodity prices in recent months. Under previous central bank governors, the country tried to stabilize the currency during periods of weakened current account balances, which on all previous occasions has meant increasing uncertainty followed by a sharp devaluation. Unlike before, Pakistan today has a market-priced currency which, as expected, has weakened 16% vs the USD since its strongest level in May 2021.

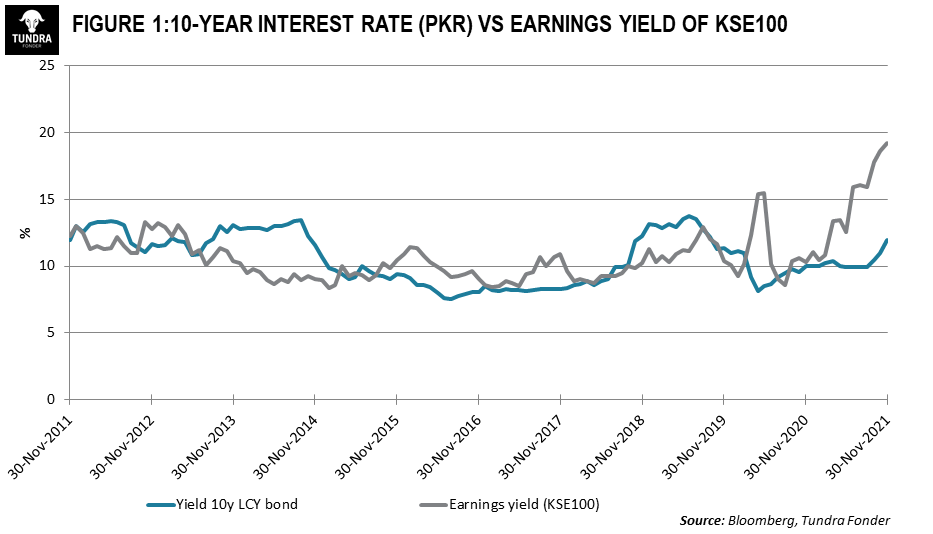

From a Real Effective Exchange Rate-perspective, the currency is now slightly undervalued. In addition, the effects of the weaker currency have gradually been absorbed by the companies. Profits among listed companies (KSE100) rose 28% YoY during the third quarter and were only marginally lower than the second quarter, which was the highest ever. We fully understand the short-term concerns about further interest rate hikes and the knee-jerk reaction from local investors to avoid equities in such a scenario. However, you must in all situations compare the current valuation with the potential impact of what you are afraid of. If we compare the return bond investors currently receive on the 10-year interest rate (normal basis for a required return) with the return investors receive on the stock market (1 / PE ratio), we find that shares have not been this attractive relative to the fixed income market in the last ten years.

This means that profits either need to collapse, or that interest rates must rise significantly above the crisis levels in 2018 (the 10-year interest rate was then just under 14% at peak, and the central bank’s policy rate peaked at 13.25%). If we look even further back in history to the Global Financial Crisis of 2008, the 10 year bond yield peaked at 16.7%. This can be compared to the current earnings yield (1/PE-ratio) of 20%. Given the composition of the index (40% banking & finance and energy), it is theoretically difficult to derive a profit decline of that magnitude. We don’t believe comparisons with 2008 are relevant and we believe even comparing with 2018 is a bit too conservative given the underlying trends we see in the country. One should always have great respect for how fear in the short term can affect stock markets. However, Pakistan is the one of our markets with the most favorable risk-reward going into 2022. Although we want to highlight that for Tundra, just like in 2021, it will always be about which stocks we own, we do expect better help from the market in the next twelve months.

One uncertainty factor that was added towards the end of the month was the news of a new variant of the corona virus, this time called Omicron. Although initial reports indicate that the symptoms are milder, the greatest risk with the corona virus remains the anxiety it can create in the form of shutdowns and other restrictions. Given that the world now has fairly recent experience of the consequences and that a more negative scenario is likely to have a certain dampening effect on inflation in particular, we find it difficult to see a more significant negative impact.

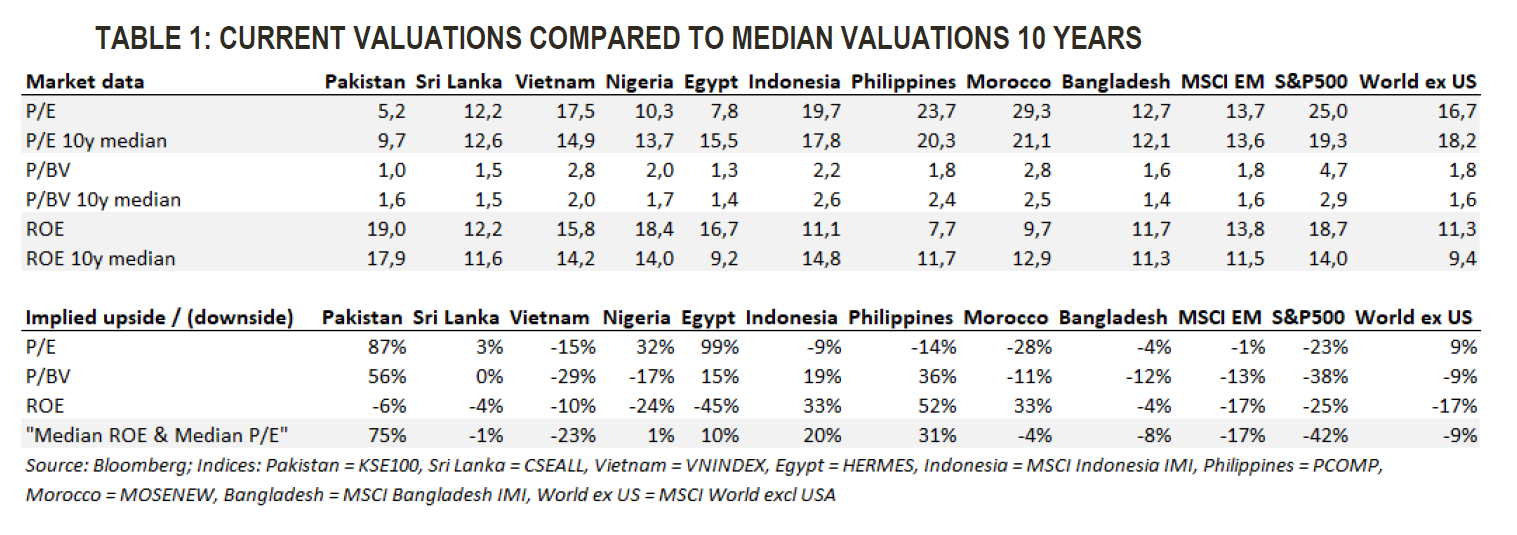

In the short term, we note some turbulence across global equity markets. To some extent, this is due to Omicron and concerns about new restrictions. But also a slightly more cautious tone from the US Federal Reserve regarding the inflation outlook and monetary policy ahead. Our markets have not enjoyed the frenzy we have seen in primarily the United States over the past 5-6 years and their valuations with few exceptions remain below or in line with their long-term median valuations (see Table 1). We are pleased with the portfolio companies’ financial performance and note that they are still early in a recovery that will hopefully last for a couple of years to come.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.