GOOD STOCK SELECTION HELPED THE FUND IN AUGUST

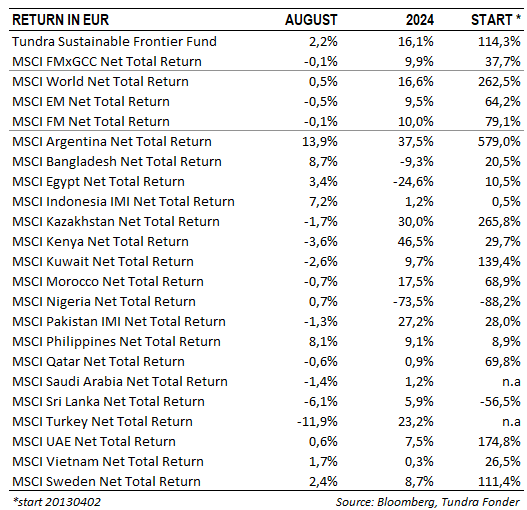

In USD, the fund rose 4.4% (EUR: +2.2%) during the month of August compared to MSCI FMxGCC Net TR (USD), which rose 2.0% (EUR: -0.1%), and MSCI EM Net TR (USD), which rose 1.6% (EUR: – 0.5%). In absolute return, it was primarily Bangladesh (+1.0% portfolio contribution) and Pakistan (+1.0% portfolio contribution) that contributed positively, while Sri Lanka (-0.1% portfolio contribution) and Turkey (-0.1% portfolio contribution) weighed slightly on returns. Relative to the index, our overweight and stock selection in Pakistan (+1.0% portfolio contribution relative to the index)and Bangladesh (+0.8% portfolio contribution relative to the index), and overweight in the Philippines (+0.7% portfolio contribution relative to the index) were the main contributors to the relative return during the month. Meanwhile, our stock selection in Vietnam (-0.2% portfolio contribution relative to the index) and underweight in Mauritius (-0.2% portfolio contribution relative to the index) contributed most negatively.

The largest single contribution came from the National Bank of Pakistan (4% of the portfolio), which rose 28%. The stock rose after the company reported an unexpected positive outcome in a court case that has been going on for several years concerning the company’s pension liability to employees. After the final liability has been determined, the company can resume its dividend. The second largest contribution was received from Bangladesh’s Brac Bank (2% of the fund). The stock rose 42% on optimism that Bangladesh will be considered a more attractive investment destination after the recent political changes (see more in previous monthly letter). The third-biggest contribution came from Vietnamese IT company FPT Corp (9% of the fund), which rose 6% with no company-specific news. The biggest negative contribution came from Vietnamese Airports Corporation of Vietnam (4% of the fund), which fell 4% during the month in continued profit-taking after the very strong run-up in the first half of the year, and Turkish ERP-company LOGO (2% of the fund), which fell 6% in a weak Turkish market.

IMPORTANT MARKET EVENTS

The Philippines suffered badly from COVID and the subsequent rise in commodity and food prices. The central bank has acted conservatively to protect the value of the currency, which has held down economic activity. During August, however, the country implemented a first rate cut since the hikes began in spring 2022. This was received positively by the stock market (+10% during August), which remains valued significantly below its historic averages measured in P/BV and P/E.

Sri Lanka was weighed down by political uncertainty ahead of the September 21st presidential election, where three candidates remain the frontrunners in the polls: incumbent President Wickremesinghe (21% in the latest opinion poll), leftist candidate Dissanayake (37%) and more liberal Premadasa (36%). In August, the latest poll was published that showed Dissanayake had overtaken Premadasa while Wickremesinghe had marginally increased his support. The election of the president in Sri Lanka is done so that every voter selects their favorite, but then also ranks the other candidates (second choice, third choice, etc.). If no candidate receives at least 50% of the votes in the first round, another count takes place where the second choice for the candidates who have been eliminated are also counted. Many of those who vote for Wickremesinghe will likely have Premadasa as their second choice as he is perceived as the closest to Wickremesinghe politically. However, some of those who vote for Premadasa might be doing so because they want to bring about change, and then it is less certain that their second choice is Wickremesinghe. Premadasa losing popularity is thus seen as worrying as it increases the probability that the politically more unproven candidate, Dissanayake, will win. Regardless of which candidate takes office, he will have to manage the relationship with the IMF. It is clear, however, that the stock market prefers either Wickremesinghe or Premadasa, whose political agendas are more predictable.

On September 23rd, Pakistan will officially leave FTSE Secondary Emerging Market status. Vanguard, which tracks the FTSE Benchmark, is estimated to have invested USD 150m in Pakistan. Rebalancing is supposed to happen on September 20th. The downgrade and its potential implications have been known since early July and are thus widely anticipated. Historically, flows related to index changes tend to impact the equity market well before actual implementation. It, however, remains to be seen if this pattern repeats this time.

After the resignation of ex-Prime Minister Ms. Sheikh Hasina, the government transferred to an interim setup, which is headed by a competent Nobel laureate Mr. Muhammad Yunus. Mr. Yunus quickly formed a cabinet of over a dozen advisors to run the different ministries within the government. The mandate assigned to the interim government is to reform different government ministries and institutions before announcing a fresh election. Consequently, we saw a sprawling change in the leadership of different institutions, such as the Central Bank, the Securities Exchange Commission, the Stock Exchange, etc. In August, the interim government quickly undertook key measures to address ongoing economic challenges (i.e., the high balance of payment deficit and inflation) to limit the fallout to the economy from the recent protest and subsequent change in the government. To bridge the shortfall in the balance of payment, the government decided to seek USD 8 billion in loans from development partners, including the IMF, to pay back foreign liabilities and build FX reserves. Consequently, the government has formed a proposal to top up the existing IMF program by an additional USD 3 billion. In tandem, the new government let the exchange rate weaken to reflect demand and supply. As a result, BDT/USD saw a depreciation of 2.1% during the month. The impact of supply chain disruption caused by the protest weighed on July’s inflation number, where the consumer price index rose by 194 bps to 11.66% from the previous month, a 12- year high. Subsequently, the central bank raised the policy rate by 50 bps to 9%, in line with the IMF prescription. Furthermore, the new governor of the central bank hinted that the central bank might raise policy rates to 10% or more to control inflation in view of the sticky inflation outlook in the near term. On the ground, there are high hopes and expectations from the interim government. However, it’s important to remember that change is a process, not an immediate event. People often focus on their current concerns and may struggle to see the larger, long-term picture. In developing nations, progress is usually seen as a gradual journey, where each step contributes to ongoing development and improvement.

___________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.