STEADY GAINS IN JUNE

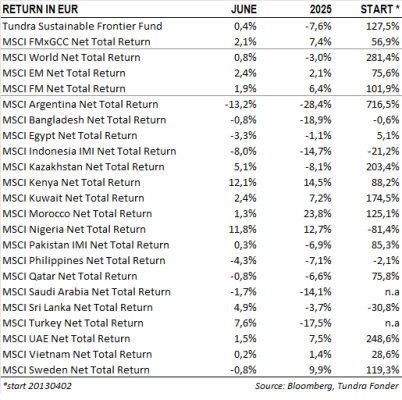

In In USD the fund rose by 3.9% (EUR: +0.4%) during the month, compared with a gain of 5.7% for the MSCI FMxGCC Net TR (USD) (EUR: +2.1%) and 6.0% for the MSCI EM Net TR (USD) (EUR: +2.4%). In terms of absolute contribution, Sri Lanka was the strongest performer (+0.8% absolute contribution), followed by Vietnam (+0.5%) and Bangladesh (+0.5%), while Indonesia (-0.3%) was the only country portfolio with a negative contribution. Relative to the benchmark, our overweight positions in Sri Lanka (+0.7% relative contribution), Nigeria (+0.5%), and Bangladesh (+0.5%) were the main positive contributors, whereas the absence of holdings in Romania (-1.1%) and Slovenia (-0.8%), along with an underweight in Morocco (-0.6%), weighed negatively on performance.

Among individual holdings, the largest contributions came from Pakistani banks—National Bank of Pakistan (5% of the portfolio), which rose 14%, and Meezan Bank (7% of the portfolio), which gained 9%. In our view, the key drivers behind these gains were growing optimism regarding earnings capacity and attractive dividend yields in a declining interest rate environment. The third-largest contributor was Vietnamese company REE Corp (7% of the portfolio), which rose 9% following a slightly better-than-expected Q1 earnings report. On the negative side, the main detractor was Indonesian Hermina Hospitals (3% of the portfolio), which declined 7%, following a strong rally in May.

We took advantage of the calmer market environment in several of our markets to make some portfolio adjustments. In Bangladesh, we increased our position in BRAC Bank while trimming our holding in pharmaceutical company Square Pharma. While we remain positive on both companies, we hold stronger conviction in BRAC Bank over the coming years and want to leave room for the position to grow. Amid the geopolitical tensions in the Middle East, we also took the opportunity to further increase our position in Egyptian bank CIB (to 3%).

KEY MARKET DEVELOPMENTS

Israel’s strike on Iran on 13 June caused only a brief stir in global equity markets and pushed oil prices up by nearly 20% (Brent, measured from the end of May). However, once it became clear that the risk of broader regional escalation was low, markets rebounded, and oil prices moderated. For the month, Brent rose 8%, though it remains 16% lower than a year ago. The involvement of the United States also had limited market impact. Following Assad’s fall in Syria, Iran lacks clear allies in the region. Natural partners such as the Houthi rebels and Hamas now have limited capacity to offer support. Aside from several formal condemnations, the international response was largely muted.

Nigeria rose 16% during the month, supported by rising oil prices. The naira appreciated 3% and has now recovered 10% against the US dollar since its low in November 2024.

Vietnam rose 4% during the month. Just after the end of the month, the US and Vietnam announced a trade agreement. Under the deal, US exports to Vietnam will be tariff-free. Vietnamese exports will be subject to a 20% tariff (down from the original proposal of 46%), while goods “transshipped” via Vietnam (exact definition still pending) will face tariffs of 40%. The higher tariff on transshipped goods is likely intended as a safeguard to block, for instance, Chinese exports routed through Vietnam before entering the US—but the specific rules remain to be clarified. As with all recent US trade deals, the practical implications will depend on implementation. Although it is positive that a major uncertainty has now been resolved, the equity market had already anticipated a reasonable outcome, especially as the US gradually softened its initially tough rhetoric from early April.

As the 9 July deadline for concluding trade agreements with the US approaches, very few countries have finalised deals. While consensus—including ourselves—expects some form of extension or exemptions to be the most likely outcome, one should not underestimate Trump’s unpredictability. This remains a key uncertainty going into the summer.

___________________________________

DISCLAIMER: DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.