FOREIGN INVESTORS RETURN TO EMERGING AND FRONTIER MARKETS

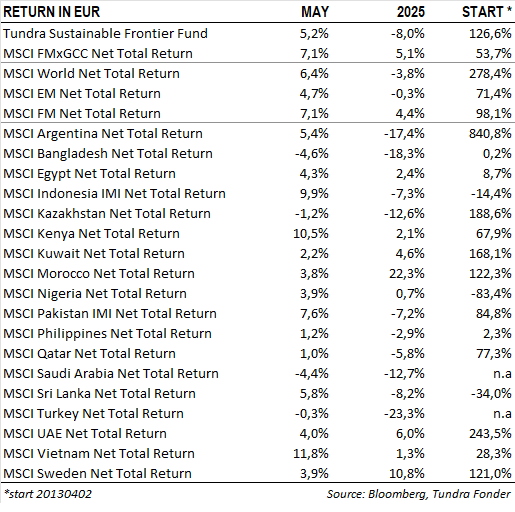

In USD the fund rose by 4.8% (EUR: +5.2%) during the month, compared to a 6.6% increase in the MSCI FMxGCC Net TR (USD) (EUR: +7.1%) and a 4.3% increase in the MSCI EM Net TR (USD) (EUR: +4.7%). In terms of absolute contribution (USD), Pakistan was the strongest contributor to the absolute return of the fund (+2.0% absolute contribution), followed by Vietnam (+1.2%) and Indonesia (+1.1%). On the negative side, Kazakhstan (-0.2%) and Egypt (-0.1%) detracted the most.

Relative to the benchmark, the primary positive contributors were our overweight positions in Pakistan (+1.8%), Indonesia (+1.1%), and Sri Lanka (+1.0%). The main detractors were stock selection in Vietnam (-1.6%) and our underweights in Romania (-0.8%), Morocco (-0.7%), Slovenia (-0.6%), and Iceland (-0.6%).

Among individual holdings, the best contribution came from Indonesian healthcare provider Hermina Hospitals (3% of the portfolio), which gained 40% following its Q1 earnings report. Pakistani Meezan Bank (7% of the portfolio) also contributed positively, rising 13% despite no specific news. The main detractor was Bangladeshi Square Pharmaceuticals (5% of the portfolio), which declined 6% in line with the broader Bangladeshi market. Egyptian dairy producer Juhayna (2% of the portfolio) was the second-largest negative contributor, falling 11% during the month as part of what we interpret as continued consolidation after peaking in February.

PORTFOLIO CHANGES IN MAY

During the month, we exited our position in Vietnamese consumer company Masan Group. Most of the proceeds were reinvested in port operator Gemadept, where we see a significantly greater upside following a recent decline related to tariff concerns. During April and May, we gradually added Gemadept, which now is among the top ten holdings of the fund.

We also added two new companies to the portfolio in May. First, we initiated a position in GRAB, the dominant ride-hailing and food delivery app in Southeast Asia, a region of 670 million people. We are attracted by the company’s exceptionally strong market position in two key segments where competition has markedly declined in recent years. We see clear potential for GRAB to evolve its super-app offering by expanding into additional services. We also value the leadership’s prudent, low-risk approach to growth. 2025 is expected to be the first year of positive post-tax earnings, and given the scalability of the business model, we believe profitability can increase significantly over the next three years.

We also added Commercial Bank of Egypt (COMI) to the portfolio. This is fundamentally a high-quality bank that we have historically avoided due to what we considered its premium valuation relative to its frontier peers, and the underlying risk. Previously COMI was one of the few frontier market banks trading at double-digit earnings multiples, but its valuation has now come down to approximately 4x earnings. We see a scenario in Egypt of gradual macroeconomic stabilisation after a challenging period, with interest rates likely to remain elevated while corporate fundamentals improve (reducing credit risk). We consider this an opportune time to add one of the strongest banks in our investment universe, now with an attractive long-term risk/reward profile.

KEY MARKET DEVELOPMENTS

Vietnam gained 11% during the month, supported by optimism around tariff negotiations with the United States. Positive signals from the Trump administration regarding a willingness to compromise were well received, and Vietnam’s own meetings in Washington (19–22 May) were described as successful. Notably, foreign investors turned net buyers for the first time in several months.

Indonesia rose 10% in May. As in several Asian markets, foreigners returned to the buy side after an extended period of outflows. We also detect a delayed reaction to the April announcement by state pension fund BPJS, which plans to double its allocation to local equities over the next three years (from less than 10% to 15-20%) due to attractive valuations. Increased participation by local institutions in our markets is a crucial—yet often underestimated—factor in addressing depressed valuations, particularly in the absence of clear catalysts for a turnaround. We note that the Indonesian equity market (Jakarta Composite Index) briefly touched two standard deviations below its 10-year average price-to-book ratio in March, but has since begun to recover.

Pakistan advanced 7% during the month following the announcement of a ceasefire with India. The outcome was in line with our expectations, although the level of military activity this time was unusually high. The tragic attack in Pahalgam, where 26 tourists were killed, was a stark reminder of the fragile security situation in Kashmir and quickly became a politically charged issue. The Indian government faced a choice: either evaluate its own security arrangements—implicitly accepting blame—or accuse its arch-rival and carry out retaliatory strikes. Politically, the latter was the more expedient option, which in turn compelled Pakistan to respond in kind to satisfy domestic sentiment. The confrontation concluded with the United States stepping in as mediator, resulting in an agreed ceasefire. This will not be the last time tensions flare between the two countries, but once again both demonstrated an ability to act rationally and responsibly under pressure. Also during the month, the State Bank of Pakistan cut its policy rate by another 100 basis points, somewhat unexpectedly, to 11%. This brings the rate just below the ten-year average of 11.5%. May inflation was reported at 3.5%, still influenced by base effects. Looking 12 months ahead, inflation is projected to rise to around 7%. We note that inflation expectations continue to be revised downwards—at the beginning of the year, forecasts pointed to 8–9% by year-end.

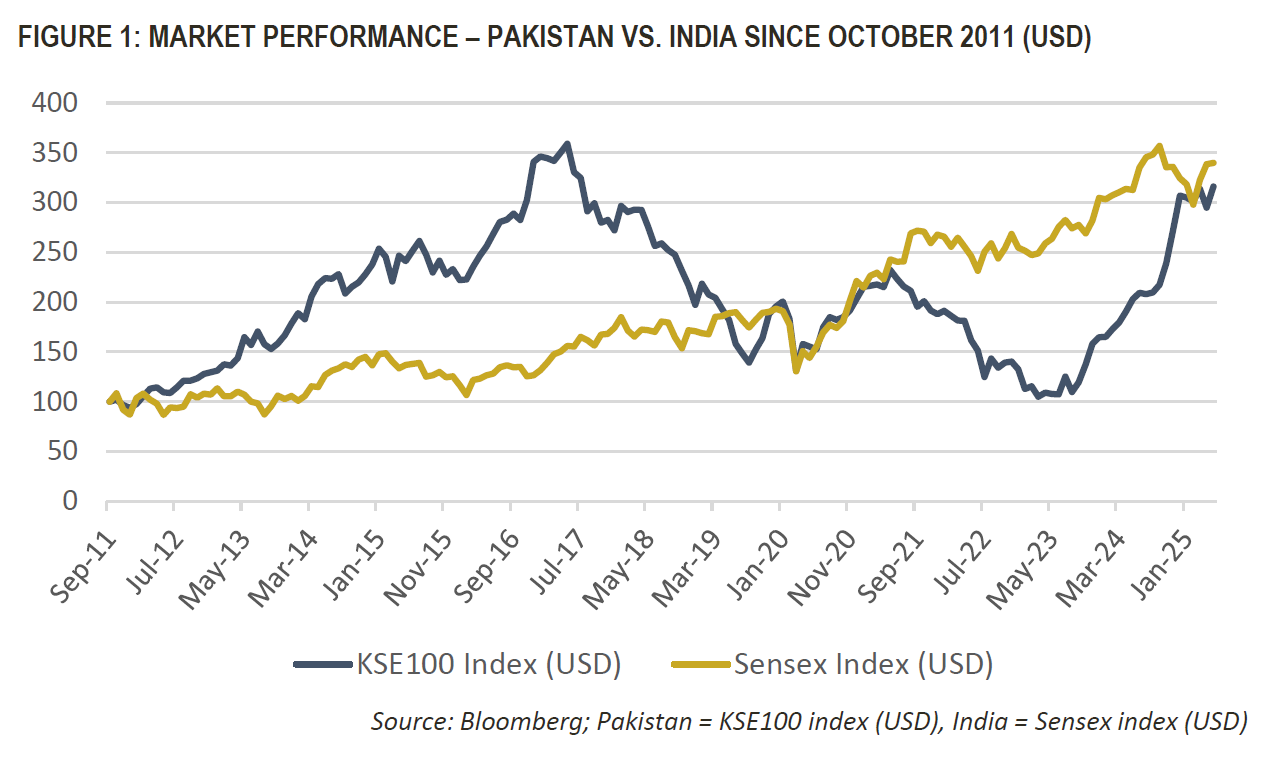

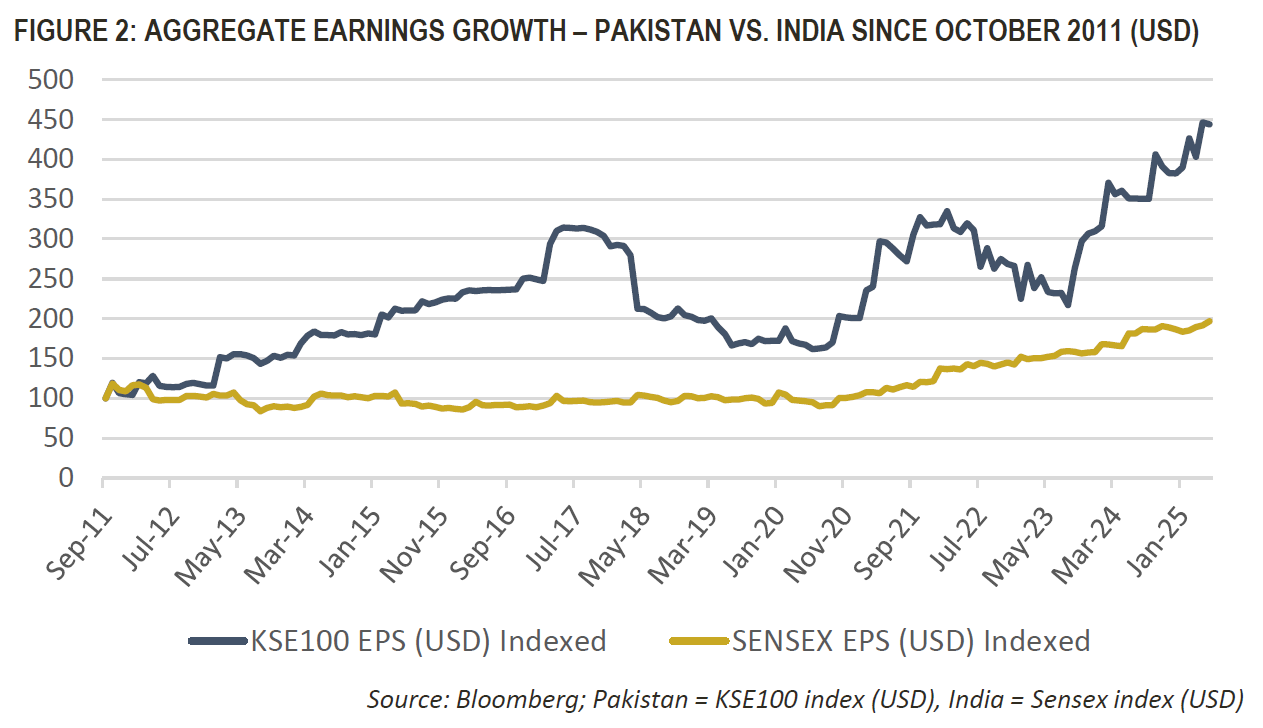

When Tundra launched its operations in October 2011, our first fund was a dedicated Pakistan fund. At the time, the decision was seen as controversial, with many investors considering the market uninvestable. What followed was a true rollercoaster: a number of strong years (2012–mid-2017), followed by six difficult ones (mid-2017–2022). Looking back, we now note that the Pakistani equity market (KSE100 Index) has, in fact, delivered approximately the same return as one of the world’s most celebrated emerging markets, India (SENSEX Index), over the full period—measured in USD. Those who have followed us through the years know that our investment case for Pakistan has always been based on the quality of the companies we’ve found there, rather than the broader macro backdrop. We’ve consistently highlighted earnings growth and management teams capable of navigating even the most adverse conditions. Over the past 13.5 years, average annual earnings growth for companies in the KSE100 Index has been 11.7% in USD terms, compared to 5.1% for Indian companies. Today, the Pakistani equity market trades at just over 6x earnings, while India trades at 22x. We are under no illusion that the risk premium assigned to Pakistani equities will decline dramatically in the near term, but we continue to see the valuation as conservative relative to demonstrated historical earnings growth. The underlying earnings trajectory supports a positive long-term outlook, even in the absence of multiple expansion.

___________________________________

DISCLAIMER: DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.