THE FUND

The fund rose 0.6% in September, better than the benchmark index MSCI EFM Africa ex South Africa Net Total Return Index, which rose 0.1%. So far this year, the fund has risen by 6.8%, worse than the benchmark index, which has risen 18.0%. At a country level, overweigths in Nigeria (33% of fund assets) and underweights in Morocco (0%) contributed most positively relative the benchmark. The fund’s overweigths in Egypt (51% of fund assets) and underweights in Kenya (0%) contributed most negatively. At the sector level, stock picks in Financials along with underweights in Materials contributed most positively, while the underweights and stock selection in Consumer Staples and overweigths in Health Care contributed most negatively relative the benchmark index. The Swedish krona was unchanged versus the USD. (all changes in SEK).

No major portfolio changes were done in September

MARKET

In September, the African markets (MSCI EFM Africa xSA Net TR +0.1%) performed worse than other Frontier markets (MSCI FMxGCC Net TR), which rose 0.4% during the month. Zimbabwe was the best African market rising with an impressive 40.1% (but still for the wrong reasons, which we have covered in a number of previous monthly updates, e.g. here), followed by Namibia, which rose 5.2%. BRVM (a joint exchange for e.g. Senegal, Ivory Coast and Benin) was the worst African market declining 7.5%, while Tunisia was the second-worst performer, falling 3%. (all changes in SEK).

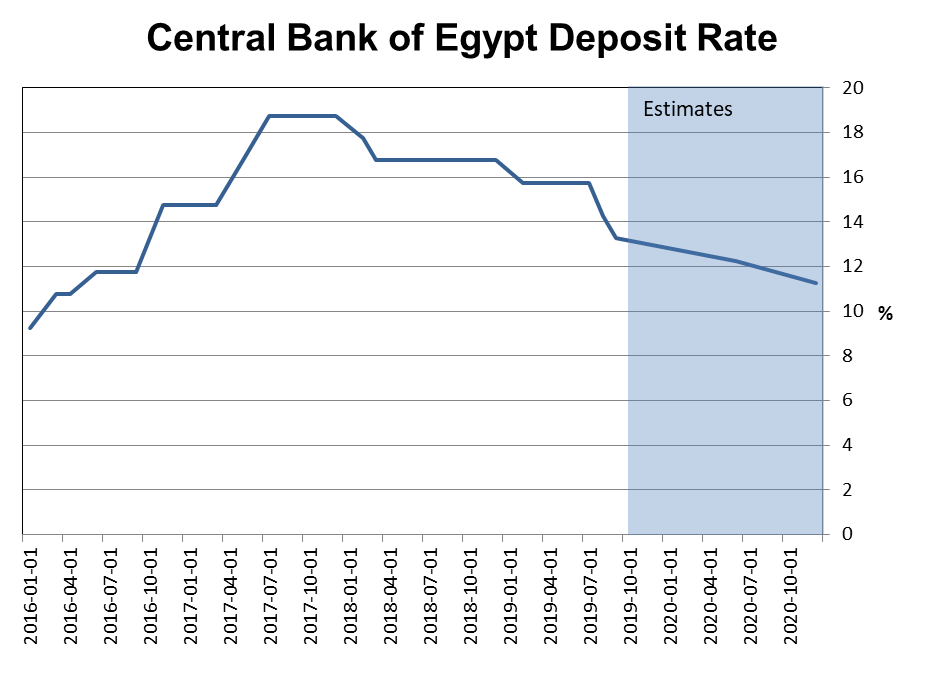

The Egyptian market (Hermes Index -2.5% in September) fell sharply after unexpected protests against al-Sisi were carried out in several cities in the country. Although the number of participants in the protests amounted to hundreds rather than thousands, the market reacted strongly and fell more than 10% over the following three trading days. Since the two revolutions (Arab Spring 2011 and the deposition of the Muslim Brotherhood 2013) there have been no major protests and the nervousness was evident with lots of alarming headlines and articles about the dissatisfaction with the reforms that eroded the purchasing power of the poorer part of the population. Prior to the following weekend, security was enhanced, and up to 2000 people were arrested to reduce the risk of more protests. In addition, a large pro-Sisi demonstration was organized, which attracted thousands of people. The relief in the market when the weekend passed without any reports of major gatherings was huge, and the stock market quickly recouped about half of the fall. It is too early to write off further protests fully, but the authorities are likely to be on full alert in the near future to make sure it is quiet on the streets. At the same time, the protests are a symptom of the fact that there are sections of society that do not feel that the clearly improved economic outlook for the country has benefited them, which must be dealt with in some way. In the long run, arresting people for expressing dissenting views for the policy pursued is not a viable option. Inflation fell to 7.5% in August (the lowest level since January 2013), and the central bank lowered the interest rate by another 1%-point at its September meeting. This means that the interest rate has now been cut 3.5% -points this year and we are starting to approach levels where the banks believe that lending to corporates for capacity expansion will accelerate again. A further 2% reduction is expected within the next 18 months, with most of it taking place next year.

The Nigerian stock market (Nigeria Stock Exchange Main Index + 1.2%) found it difficult to show any great enthusiasm after the rather poor GDP growth was released at the beginning of the month, (GDP 2Q2019 + 1.94%) but most blue chips recovered during the latter part. The inflation in August was reported to increase by 11%, approx. the same level since May 2018. The Central Bank Governor Godwin Emefiele has also expressed that there will be no interest rate cuts until inflation has come down to around 9%-level, which according to most analysts excludes more cuts this year after the surprising cut earlier in March.

In Kenya (Nairobi All Share Index + 2.8%), the debate continues on the interest rate cap that was introduced in September 2016 which limits the borrowing rate that banks can charge. Despite the Supreme Court’s ruling earlier this year that the interest rate cap contravenes the law, there are few signs that it will be removed in the near future. It’s more likely to remain in some form, which will continue to have a dampening effect on both banks’ profits and on the economic growth in Kenya. However, the latter seems to have adapted well despite the fact that the lending growth rate today is about half of what it was before the ceiling was introduced. GDP rose by 5.6% during the second quarter of this year 0.1%-point higher than expected.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.