THE FUND

The Fund fell 9.1% in May, compared to MSCI Pakistan IMI Net TR (SEK), which fell 5.3%. Most of the underperformance (3%) came from our overweight in cyclical sectors, primarily cement and steel. You can read more about these positions in the previous monthly letter. Over a period of just over a month, the team has done a thorough review of the companies, which rendered selective adjustments to the positions. Given that Pakistan has now reached an agreement in principle with the IMF (May 12), which, after the presentation of the budget on June 11, should result in a signed agreement, we believe that the uncertainty will gradually decline in the coming months. This is likely to benefit the hardest hit sectors, such as cement, which are now trading at distressed valuations. During the month, we increased our exposure to the banking sector. The Fund added Bank Alfalah, MCB Bank, Meezan Bank, and National Bank of Pakistan to the portfolio. The banking sector is one of the few sectors that directly benefit from the higher interest rate situation and we expect significant EPS growth in the coming 12 months.

MARKET

The government’s communication with the market has been under all criticism since assuming power. The worst thing a leader can do towards financial markets is to formulate timelines that are then gradually moved. This is what happened in the autumn when a tentative timetable for an IMF agreement was gradually moved from early autumn to an agreement in principle on May 12. The business community and its investors are able to absorb short term shocks, but uncertainty creates paralysis, spreading of rumors, and ultimately panic. When the principle agreement on the IMF agreement was finally announced on May 12, the market was still left guessing in terms of what it meant. Expressions such as “market-priced exchange rate” and “heavy budget cuts” without further specification, created a last wave of panic on the market in the days after the announcement, and the currency was devalued an additional 7%. However, criticism aside, it is now time to look forward. In the budget that will be published on June 11, all details regarding agreed cuts in spending and tax increases should be stated and any remaining uncertainties should be highlighted.

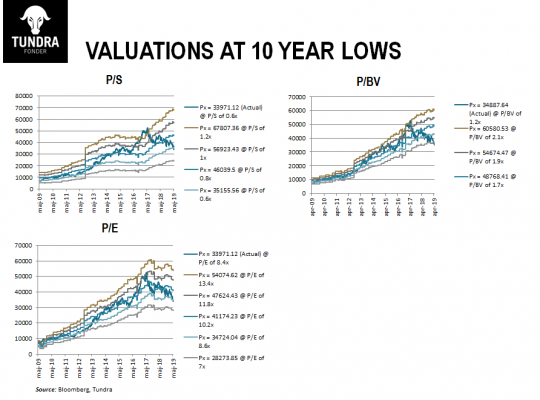

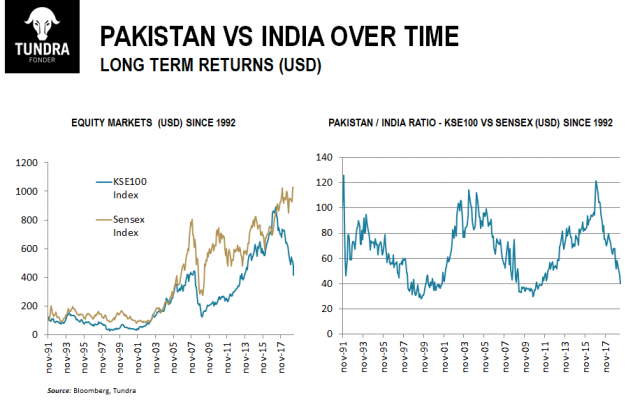

At the end of May, a number of support measures were announced towards the stock market. A state-funded support fund for the equity market is about to be established. The fund will be able to invest in the equity market with an initial capital of USD 150m. Furthermore, the Securities Exchange Commission is reviewing the possibility of simplifying for companies to buy back their own shares. At present, this is a relatively complicated process. Given that most companies are debt-free and that the stock market is trading about 10-year-lowest vs book values, several companies would benefit from the opportunity if beneficial enough. The short-term uncertainty and the pessimistic dynamics this creates must be broken through clear measures that have an impact in the short term, but above all through clear communication. However, we should remember that we remain optimistic about the new government’s reform program, focusing on raising a larger proportion of the population from poverty and increasing Pakistan’s industrial export base. Of course, these measures will take several years to bear fruit, but as soon as we get out of the current period of uncertainty and painful savings programs, we should expect the equity market to look beyond the current pain. As mentioned earlier, the Pakistani equities are trading close to ten-year lows versus book value, and the P/E ratio of just under 7 times compared with a historical average of about 9 times. Until mid-2017, Pakistan’s stock market and India’s stock market had yielded a similar US dollar return over the 27-year data available through Bloomberg. As appears from the graph showing the Ratio KSE100/Sensex (USD), Pakistan’s historical underperformance is now close to historical bottoms. It has been two troublesome years for investors in Pakistan and there might be another few months of uncertain development, but nevertheless, the next couple of years are looking considerably better.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.